“The last shall be first and the first last.”

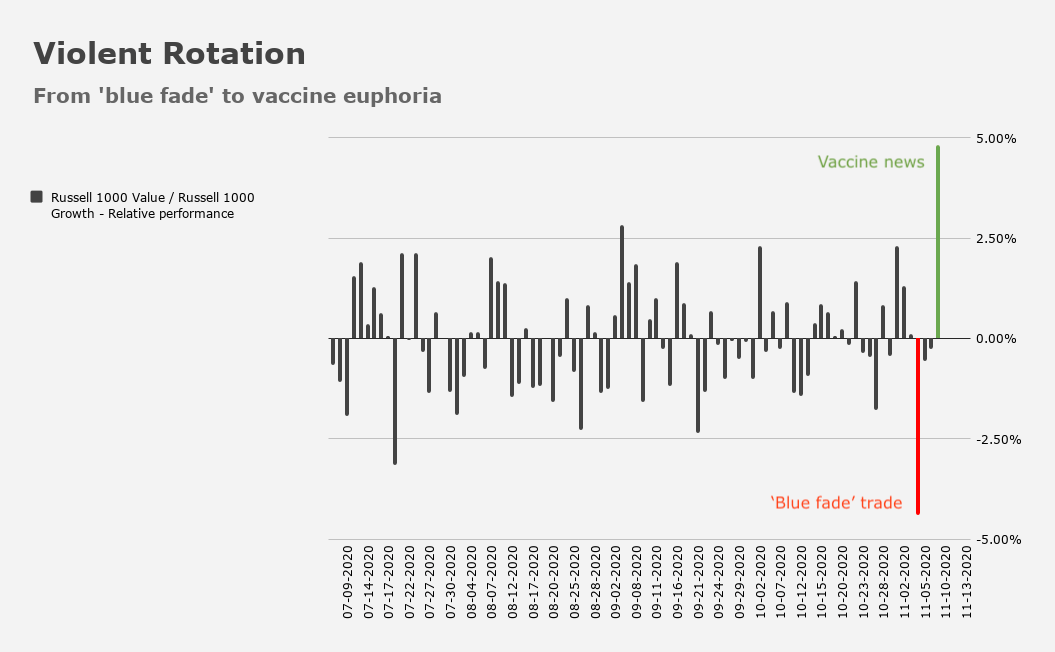

That was the story for markets through Tuesday, as value posted record outperformance versus growth thanks to Monday’s vaccine news from Pfizer.

The visuals are astounding, and they are myriad (see here, here, and here, for example). During these types of shocks that lead to dramatic dispersion, you can spend all day (literally) conjuring fun charts and statistics. I’ll indulge one more. On Monday, the equal-weighted S&P outperformed its cap-weighted counterpart by the most ever.

Writing on Tuesday, Nomura’s Charlie McElligott remarked that “‘Momentum’ shocks rarely happen in isolation, especially in the case of a market which is attempting to anticipate ‘regime change’ by pulling forward future growth- and inflation- expectations.”

If you’re wondering about the magnitude of Monday’s moves at a more granular (for lack of a better adjective) level, McElligott noted that “yesterday was the largest one-day US Equities ‘Momentum’ factor crash in the history” of Nomura’s data. The decline was -24.5% — it was a 0.0%ile move. That’s zero point zero.

“‘Mo Longs’ were destroyed,” Charlie wrote, noting that many growth factors witnessed underperformance that counted as -7 to -15 standard deviation moves. On the flip side, Momentum shorts “exploded higher,” which McElligott reminds you “caus[ed] pain, with ‘Value’ factors experiencing +8 to +12 standard deviation moves.”

Going forward, one obvious question is how the Fed would react to a sustained rise in long-end yields and a concurrent bear steepener. Given the amount of duration risk embedded across the market, not to mention the more straightforward impact higher yields would have in terms of tightening financial conditions, those outcomes are non-starters.

Last week, Jerome Powell essentially confirmed that the Fed can and will extend the maturity profile of asset purchases if “necessary.” That has implications for the durability of any pro-cyclical rotation.

“What could kibosh this ‘economic’ +++ impulse pull-forward,’ Value factor renaissance from here?,” McElligott asked on Tuesday, before answering his own question.

“Outside of the COVID trajectory and seeing states re-restrict activity in the absence of a deployed vaccine, the Fed plays a major role on the macro rates side,” he said. “If the bond selloff were to get sloppier from here, we already know that the Fed plans to extend the duration /WAM of the portfolio or size of the overall QE purchases, because they cannot allow tighter financial conditions [during an] extremely fragile economic recovery.”

The irony, then, is that protecting that “extremely fragile recovery” may mean taking actions that, via their likely bull-flattening effect on curves, could undercut equities trades that benefit from expectations for a stronger recovery.

{kind=link}

{kind=link}

{kind=link}

Just idol speculation of the Fed on my part…we’ll wake up one morning to an announcement that they are buying the long bonds. TLT goes from whatever SD below 200 DMA to some goofy move about resistance.

Lower resistance is like 137. No way it’s going to test this before we’re post COVID. Maybe not even while we are still in the existing monetary regime.

The Treasury has already telegraphed that they are going to move from short term to longer term bonds to fund measures.

There is no ambiguity in Fed policy.

A reasonably high probability outcome for the next six months is COVID, businesses close, employment suffers, income suffers, lackluster stimulus, Fed jawbone or purchases creates YCC, Treasury sells long bonds, government funded using 20 and 30 years, checks go out.

What remains is what’s the level of rates where the Fed and Treasury have had enough. When the Treasury wants to fund with the longer bond, and they can fund at 0.6% instead of 1.0%, rates are going to move and they’re going to fund at the lower rate. And, it’s kind of in our nation’s collective interest any longer to want them fund at 0.6% rather than 1.0%.

we are going to need another vaccine