While explaining France’s new coronavirus lockdowns, Emmanuel Macron was unequivocal in dispelling the notion that there are easy fixes for the worst public health crisis the world has seen in a generation. “There’s no magical solution,” he said.

That’s bad news for Christine Lagarde and the ECB. In the post-financial crisis world, monetary policy garnered a (dubious) reputation for offering silver bullets, elixirs, and sundry cure-alls, to a world that desperately needed real economic solutions.

Alas, politicians across advanced economies proved largely inept, opting instead for austerity, supply-side gimmickry, and other half-measures, leading directly to lackluster growth and inflation outcomes following the GFC and the European debt crisis. In simple terms, the developed world limped into the pandemic economically, with monetary policy largely exhausted.

“Largely exhausted” doesn’t mean “totally bereft,” though, and the policy response to the pandemic has been dramatic indeed. Central banks have deployed trillions in asset purchases to help stabilize the global economy and to accommodate the kind of massive fiscal impulse necessary to save jobs, not to mention lives (figure below).

The ECB came into its October meeting confronting a rapidly deteriorating situation across the eurozone’s largest economies. France and Germany instituted new lockdowns this week in a bid to contain a second virus wave that’s markedly worse than the first on some metrics.

Services sector PMIs were already deteriorating, hinting at a loss of economic momentum for Europe prior to the new containment protocols. Some analysts now see a double-dip recession as inevitable. Small- and medium-sized firms face an existential crisis.

Core inflation sits at a record low, and the headline gauge is in negative territory. While some of this is down to one-offs and various pandemic distortions, the bottom line is that the ECB’s ever elusive target became even more distant thanks to the virus.

Euro strength exacerbated things. While Christine Lagarde downplayed the currency effect at the September meeting, she later reversed course, admitting the obvious, which is just that the FX channel matters. A stronger currency into a deflationary backdrop can beget still more disinflation.

It’s with all of this in mind that the ECB is widely expected to expand its emergency pandemic asset purchase program (PEPP) later this year.

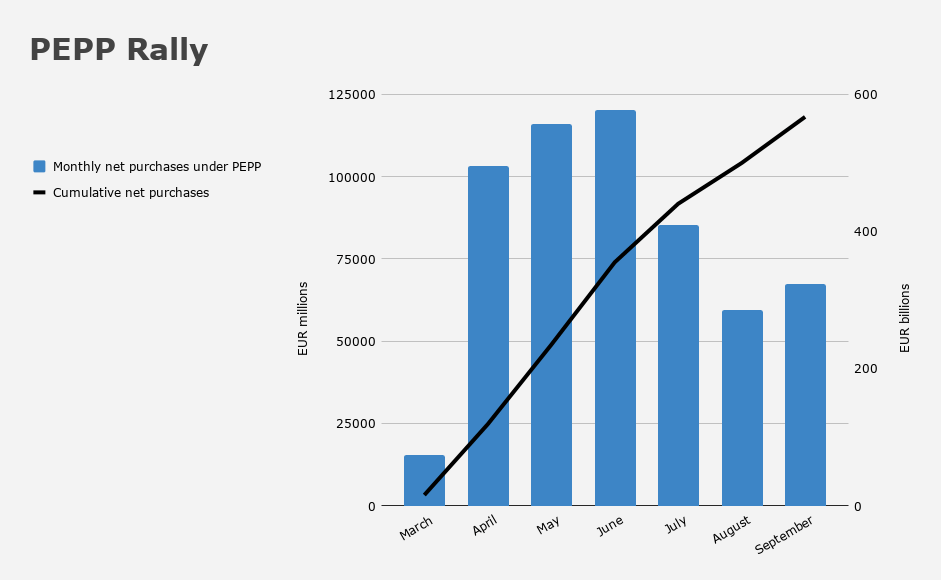

As a reminder, PEPP came with initial firepower of €750 billion and was later expanded to €1.35 trillion. It’s not even halfway exhausted yet (figure below).

Given the existing dry powder, the market expected the ECB to wait until December to authorize an additional €500 billion in purchases.

That was, in fact, the correct read. The ECB’s October statement keeps the PEPP envelope unchanged at €1.35 trillion — for now.

You’re reminded that this program is running alongside “regular” QE.

“In the current environment of risks clearly tilted to the downside, the Governing Council will carefully assess the incoming information, including the dynamics of the pandemic, prospects for a rollout of vaccines and developments in the exchange rate,” the October statement reads. “The new round of Eurosystem staff macroeconomic projections in December will allow a thorough reassessment of the economic outlook and the balance of risks.”

There is a rather explicit nod to imminent additional easing in December:

On the basis of this updated assessment, the Governing Council will recalibrate its instruments, as appropriate, to respond to the unfolding situation and to ensure that financing conditions remain favourable to support the economic recovery and counteract the negative impact of the pandemic on the projected inflation path. This will foster the convergence of inflation towards its aim in a sustained manner, in line with its commitment to symmetry.

Clearly, Lagarde can make the case, with the usual caveat that monetary policy acting in isolation (i.e., without a concurrent fiscal impulse) is not as effective.

She offered a cautious take on the economic outlook Thursday, setting the stage for more easing in December. “There’s little doubt” that the ECB will act later this year, she said.

Of course, by then, the eurozone economy will likely have suffered a fresh blow from new lockdowns. Hopefully, that will be offset by a marked reduction in virus cases and fatalities.

The bottom line is that just a year in, Lagarde has endured a trial by fire. This time last year, the world hadn’t even heard of COVID-19, and a guy named Mario was bidding the ECB adieu.

ECB October statement

In the current environment of risks clearly tilted to the downside, the Governing Council will carefully assess the incoming information, including the dynamics of the pandemic, prospects for a rollout of vaccines and developments in the exchange rate. The new round of Eurosystem staff macroeconomic projections in December will allow a thorough reassessment of the economic outlook and the balance of risks. On the basis of this updated assessment, the Governing Council will recalibrate its instruments, as appropriate, to respond to the unfolding situation and to ensure that financing conditions remain favourable to support the economic recovery and counteract the negative impact of the pandemic on the projected inflation path. This will foster the convergence of inflation towards its aim in a sustained manner, in line with its commitment to symmetry.

In the meantime, the Governing Council of the ECB took the following monetary policy decisions:

(1) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

(2) The Governing Council will continue its purchases under the pandemic emergency purchase programme (PEPP) with a total envelope of €1,350 billion. These purchases contribute to easing the overall monetary policy stance, thereby helping to offset the downward impact of the pandemic on the projected path of inflation. The purchases will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions. This allows the Governing Council to effectively stave off risks to the smooth transmission of monetary policy. The Governing Council will conduct net asset purchases under the PEPP until at least the end of June 2021 and, in any case, until it judges that the coronavirus crisis phase is over. The Governing Council will reinvest the principal payments from maturing securities purchased under the PEPP until at least the end of 2022. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

(3) Net purchases under the asset purchase programme (APP) will continue at a monthly pace of €20 billion, together with the purchases under the additional €120 billion temporary envelope until the end of the year. The Governing Council continues to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates. The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

(4) The Governing Council will also continue to provide ample liquidity through its refinancing operations. In particular, the third series of targeted longer-term refinancing operations (TLTRO III) remains an attractive source of funding for banks, supporting bank lending to firms and households.