We now know that SoftBank was the “Nasdaq whale”.

For at least a week prior to Thursday’s big selloff (and its less spectacular sequel on Friday morning), the rumor mill was alive with talk of a massive buyer in single-name call options on red-hot tech shares and the handful of momentum stocks which became synonymous with the summer rally.

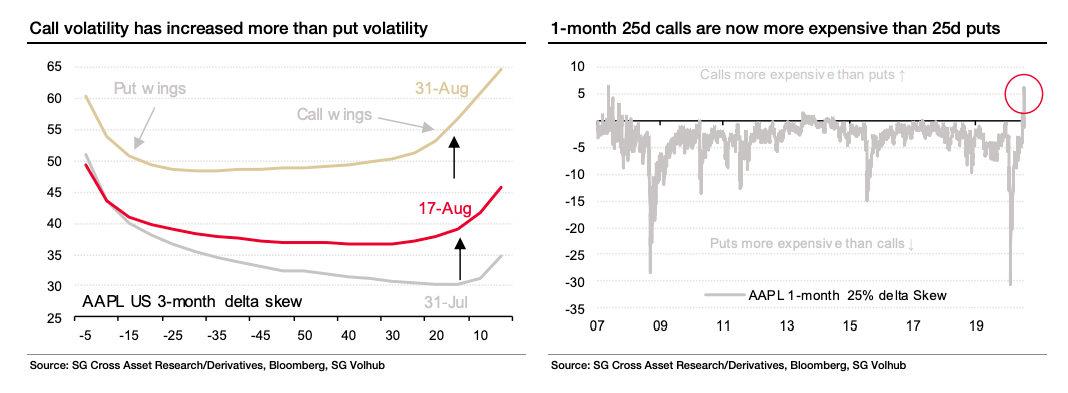

As August melted into September, it was abundantly clear to anyone with any sense that there was more to the Nasdaq 100’s run-up than just earnings and the fundamental case for indispensable technology in a post-pandemic world. Anomalous moves in Salesforce, Netflix, and Zoom, along with Apple’s almost comical ascent, lent credence to the notion that the Street was short gamma in the wake of large, persistent upside premium buying.

I’ve spilled gallons of digital ink documenting this over the past two weeks (here, here, and here, among a half-dozen at least), and I endeavored to ramp up the volume starting Monday, as it became increasingly apparent that, as Nomura’s Charlie McElligott put it, “this flow is simply larger than an illiquid August single-name market can take”.

“Although we’re just hearing about it, rest assured, it’s been an open secret on institutional desks for the past week”, Kevin Muir said Tuesday. “You simply can’t buy that sort of size without rumors spreading”.

And you didn’t need the rumors to see it. It was readily apparent in, for example, skews, the “stocks up, vol up” character of the rally and the concurrent positive correlation between the VIX and the S&P, among other “tells”.

On Friday, just in time for nobody to be around ahead of the long US weekend, the Financial Times made all of this “official”, unmasking the “Nasdaq whale” in the process.

That it’s SoftBank somehow seems wholly unsurprising to me, even as the trades were described as “a new chapter” for Masayoshi Son. FT cites the ubiquitous “people familiar with the matter” in confirming that SoftBank spent the past couple of months “snapping up options in tech stocks… in huge amounts, fueling the largest ever trading volumes in contracts linked to individual companies”.

Descriptions of the trades ranged from “huge” to “dangerous”, in keeping with the language heard across desks (and parroted in these pages) in the week leading up to Thursday’s rout.

“These are some of the biggest trades I’ve seen in 20 years of doing this”, one buy-sider told FT, whose coverage correctly, if belatedly, notes that “the sheer size of the trades appears to have exacerbated a ‘melt-up’ in many big technology stocks over the summer”.

Yes, it does “appear” that way, doesn’t it?

It also “appears” to have catalyzed absurd, parabolic wealth gains for the founders and CEOs of the tech names swept up in the surge, which was by no means confined to FAAMG. As mentioned above, Salesforce, Zoom, and Tesla, among others, also benefited either in first- or second-order fashion, as did the Nasdaq itself and, to a lesser extent, the S&P.

When the self-feeding loop was spinning at its fastest, the top-10 richest people on the planet added $30 billion in net worth over the course of just 72 hours late last week.

Shortly after FT‘s piece was published, WSJ printed something similar, calling SoftBank’s call-buying program “a giant but shadowy bet”, in an amusing attempt to create suspense.

The bottom line, as Charlie put it Tuesday, is that SoftBank’s flow was “frankly” more than the single-name market “can ever take regardless of month”.

Kevin echoed those sentiments. “The buying is huge. This is a monster bet by a Godzilla of an account”, he said Tuesday. (As it turns out, “Godzilla” was an exceptionally apt description, given SoftBank’s country of origin.)

As explicitly stated here during the selloff, Thursday’s rout was comeuppance — it’s just not clear for whom. While legions of Robinhood traders and other unwitting home gamers caught up in the euphoria witnessed what Bloomberg called “downright existential” losses, SoftBank can easily absorb the hit.

One banker who spoke to FT said that while the downdraft “would have been painful for SoftBank, he expected the buying to resume”.

Read more: Whale Tales And Riverboat Gamblers – The Story Of 2020’s Summer Tech Bonanza

What is it with Softbank and bubbles? Seemingly everything they touch. The poster child of Minsky’s “ponzi finance”.

Right? Does Masayoshi Son have a massive gambling problem on a scale unseen by humanity? Is there a shadowy cabal behind the shadowy cabal? Stay tuned next week to find out!

Yeah, as noted in the piece, this was wholly unsurprising to me. I mean, I see why it’s a “big” story, and kudos to FT for figuring out who it was, but certainly don’t count me incredulous. Plus, it just feels like the mainstream media should have done more on this over the past two weeks. It was painfully obvious that this was in the driver’s seat, and I saw very little coverage of the dynamics themselves outside of blogs.

I expect we will see more of these strategies deployed by big players, resulting in future “crash up” “crash down” dynamics, if nothing else, Softbank proved the strategy works in a somewhat illiquid market, volume today included 90k+ AAPL calls at the 125 strike expiring next Friday, most of the flow came in when AAPL was trading around 115 this morning, the whale is still hungry.

With three days of time decay to absorb,. Someone must be mighty confident that the vol/risk parity monsters will ride to their rescue next week.

Looking forward to more reporting on why SFTBY did this. If, say, KKR or Apollo or another major private equity player suddenly became a giant options trader, Questions Would Be Asked. SFTBY is also publicly traded, deserving more scrutiny.

If SFTBY was buying the same near dated OTM calls that the Robinhooders lost big on, then SFTBY should have suffered losses – at least on the recent buys. Those losses could be material, relative to the June quarter’s $12BN profit.

Call me fusty, but if I invested in a private equity/venture capital company based on my belief in their skill at identifying early stage companies, I would be puzzled/concerned to see it launch an options trading strategy.

Let see if the Saudis whack him. Masayoshi Son might want to avoid KSA embassies in the near future… unless the market rallies on Tuesday…

My understanding of options finance is rudimentary, but I have been told that many of the options pricing models tend to misprice short dated out of the money options. Perhaps softbank saw this and realized the opportunity in an illiquid market. Sounds like they spent the summer squeezing Wall Street options desks and brought along amateur traders along for the ride.

“Fat tail” models are supposed to cover that, but none of them price in a whale.

If so what is the trade? How does SoftBank profit from this parabolic? or was the google story just enough to let the air out of their bubble and saw them trapped like the Hunt Brothers with silver before they could get out?

My memory is aging but as I recall the Hunts were forced out by the CFTC. They might have succeeded in a Trump-style environment,

Have they cashed in their chips?

Got my bowl of popcorn/glass of vino…..watching the “show”.

Nice whale tale!

Forget the tale…this whale has FAANGs.

I guess after the WeWork and Uber toe-stubs, if you are Mr. Son you need to go big to save face.

H-Man. SoftBank dies on the vine.

Some reading shows I haven’t been paying much attention to SFTBY.

Apparently on the June quarter call it announced a strategy shift to include public stock investing, changed accounting from operating company to investment company, created a $550MM stock trading fund, sold a bunch of assets, said it would park the proceeds (many tens of billions) in “liquid stocks” before using the funds for the promised purpose of paying down debt and buying back shares, and on the last earnings call Son talked about its position in FAANG stocks. So everything was known, except for the options part, which trading desks and the bigger hedge funds would have sussed out many weeks ago. In plenty of time to join in the party and/or take the other side and/or place side bets.

According to an article I just read (Reuters, following WSJ) SFTBY bought $4BN of stock, and $4BN of options corresponding to $50BN notional. So over the past few weeks it could have made $1BN on the stock position (say 25%?) and I don’t know what it might have made on the options, this is before whatever it lost this week.

https://www.channelnewsasia.com/news/business/softbank-option-purchases-raise-eyebrows-as-wall-street-backtracks-13083794

Maybe the sell off on Thursday was caused by Soft Bank liquidating positions, thereby escaping some/most of the losses?

FT reporting SFTBY has $4BN (some unrealized) trading profit from whaling. https://amp.ft.com/content/53aa19bb-fc9a-46fd-aafd-4bc3669ab161

So the option-gobbling may continue.