“For Saudi Arabia, the shock transmits mainly through the loss in government revenue and exports caused by the drop in oil demand and prices”, Moody’s said Friday, in the course of cutting the kingdom’s outlook to negative from stable. “The government’s balance sheet has weakened since the previous oil price shock in 2015-16… leaving the sovereign’s credit profile exposed to the further prolonged period of depressed oil prices that the pandemic may usher in”.

Moody’s assessment reflects (and likely understates) the rather daunting financial reality the Saudis face in a world where demand for crude collapsed by as much as 30 million barrels per day at the height of the coronavirus shutdowns, which put economic activity on ice across developed and emerging economies for the better part of six weeks.

The IEA called last month “Black April“, while describing 2020 as the “worst year in the history of global oil markets”.

For Riyadh, this is something of a self-inflicted wound. While it’s true that Russia walked out of the original Vienna meeting when OPEC+ still had a chance to stay ahead of the pandemic by slashing production, it was the Saudis who fired the first shot in the price war the following day (on March 7).

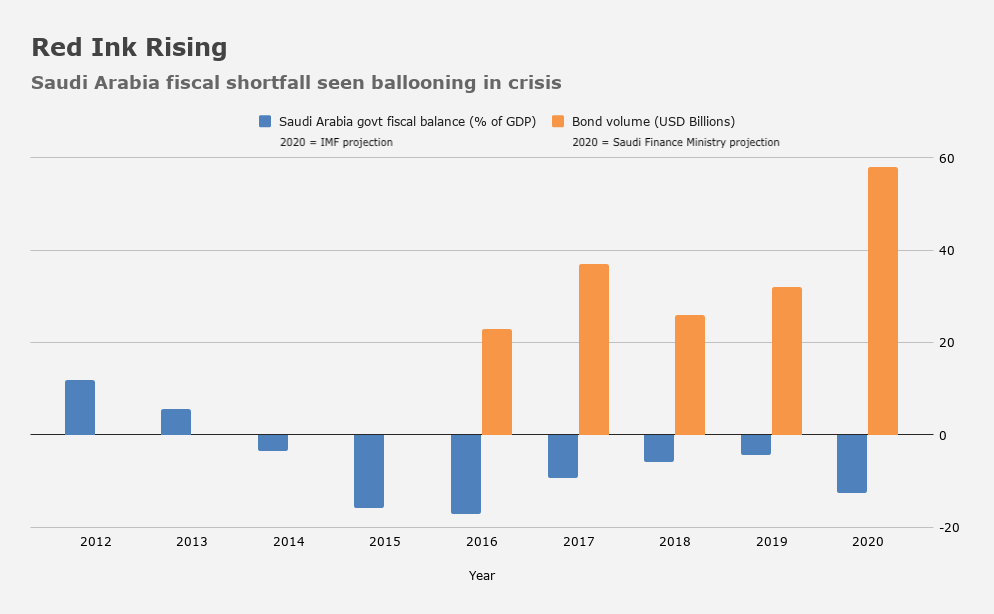

Late last month, Saudi Finance Minister Mohammed Al-Jadaan said the government may issue another 100 billion riyals in debt this year in an effort to help stop the expected budget bleed from collapsing crude prices. When you add that to the 120 billion riyals in issuance already announced, it means the kingdom could tap the market for around $60 billion in 2020, the most since its debut four years previous.

To be sure, there’s no shortage of demand if the kingdom does, in fact, raise its debt ceiling as planned. Orders for a $7 billion sale last month totaled some $54 billion, for example.

But the situation is getting pretty dicey, something Moody’s underscored Friday.

“Based on [new] oil price assumptions and Saudi Arabia’s commitment to cut oil production, Moody’s now expects that government revenues will drop by about 33% in 2020 and about 25% in 2021 relative to 2019, even after accounting for potentially higher dividends from state-owned entities”, the ratings agency said, adding that “a sharp slowdown in GDP growth will also depress revenue from the non-oil sector”. Here’s some additional color from Moody’s:

[We] project that the fiscal deficit will widen to more than 12% of GDP in 2020 and more than 8% in GDP in 2021 from 4.5% of GDP in 2019. This will cause government debt to increase to around 38% of GDP by the end of 2021 from less than 23% of GDP in 2019. These projections assume significant drawdowns from the government’s liquid assets, worth around 7% of GDP in 2020-21, in order to contain the sovereign’s borrowing requirements. The bulk of the government’s liquid fiscal buffers are on deposit with Saudi Arabian Monetary Authority (SAMA), managed as part of SAMA’s foreign currency reserves.

Note the reference at the end to the kingdom’s reserves. They plummeted by around 5% in March. And that is a problem.

Part of the rationale for tapping the debt market for an additional 100 billion riyals is to limit reserve burn, which the finance ministry says could be kept to 120 billion riyals this year. But some quick math is all you need to know that the ~$27 billion reserve decline in March essentially means the kingdom drew down the amount planned for the entire year in the space of just 30 days. Or at least that’s what it sounds like to me.

This can be ameliorated if crude prices stabilize, but that seems like a pipe dream (no pun intended) at this point.

The kingdom’s debt-to-GDP ratio is very low comparatively speaking, but it’s worth remembering that the Saudis, for all their swagger, have a very high breakeven rate when it comes to what price level is necessary to balance the budget. That level for Riyadh is about $80, a figure that stands in stark contrast to the similar figure for Russia.

That’s not to say things are going swimmingly for Moscow either, and according to some industry observers, Russia’s compliance with the cuts isn’t necessarily a sign that everything is “hunky dory”.

Consider the following, from Stephen Brennock, an analyst at PVM Oil Associates:

Russia’s retrenchment will not have been triggered by a sense of loyalty to its OPEC+ peer. Instead, the non-OPEC heavyweight is reacting to its own predicaments. For instance, Russia is expected to have made a loss on exporting Urals crude this month for the first time in two decades. All the while, the country has only eight days of available storage compared to 30 days for the US, according to IHS Markit. The glut in Cushing is grabbing all the headlines but in reality the storage situation is far more desperate in Russia. In short, Moscow is still prioritizing its own interests despite rekindling its partnership with Riyadh.

When it comes to the Saudis, nothing says this has to dead end in some kind of dramatic fiscal fiasco, especially given voracious demand for the kingdom’s debt. But it does suggest that Mohammed Bin Salman either didn’t think things through before flooding the oil market last month or else grossly underestimated the scope of the demand destruction that ended up accompanying the global effort to contain the coronavirus.

As one regional analyst quipped Friday while chatting with me about the outlook for the kingdom in 2020, “It couldn’t have happened to a nicer bunch of people”.

He was referring to the royals, of course. Not Saudi citizens.

While you can’t fault MBS for coronavirus, I think his prior provocations in the family will come back to haunt him.

hopefully so

Peter Zeihan in his recently published book has a chapter on Saudi Arabia, a particularly entertaining chapter by the way. At the end of each chapter, Mr Zeihan provides a report card for that country. And also provides a one-word summation. In the case of Saudi Arabia, that one word is: arsonist. Quite fitting indeed.

Wells shuttered and moth-balled, machinery idle, roughnecks laid off by the tens of thousands, capital investments near zero, and Greta et al magnifying a growing distaste for hydrocarbons, thus accelerating the exiting of sovereign funds and pension plans towards something more ESG.

And yet all the while, outside of this anomaly that is 2020, year after year oil consumption rates continue to rise. Simply put, the 4 billion that reside in China, Africa, India, and SE Asia are getting wealthier and thus their energy needs are growing at a faster rate than the global adoption of green energy. We are at least a decade away before oil consumption rates even plateau.

The cure to low prices, is low prices. And with a little patience the laws of supply and demand will prevail.

It’s all turning out to be a contrarian’s wet dream… and I for one am loading up on the oil blue chips.

Me too brother, me too. I lost some money in oil when price broke down (direct futures play, no USO ETF fiasco here), but I know that those prices cannot stay that low for long as here no one makes money.. Sure the glut is still huge, but EU is already opening back up, US will quickly follow. We will not see flights and tourism back to previous level any time soon if ever, but like you said emerginc economies will need more and more oil which will balance things out. I just hope we do not get wiped out before the recovery 🙂

How are you playing this? Oil related stocks and ETFs (XLe, XOP, IXC..) ETFs on oil (DBO, USL) or directly via futures or futures options? I stay away from equities as they rebounded 50 % from the lows already and due to bad earnings and dividend cuts I am not so bulish on this. I think oil price should now be next to recover while stocks will lag, but I could be dead wrong.. 🙂

Blg Oil ETFs such as FILL and a call option on XOP, and some ERX. Then individual oil companies such as Exxon, ConocoPhillips, Suncor, and Enbridge.

Honestly I don’t have the time or the skill set to adequately determine which in the industry will make it through this rough patch and which will go bankrupt. Buying an ETF like FILL that holds the world’s biggest players is the safest way to go for a guy like me.

Don’t think of a cure for low crude prices. Think of a cure for US jobs being lost in the oil patch. Think of a cure for hard earned US energy independence being lost. Even think of a cure for the environmental impact of the growing wealth in the countries you cite. Tariffs on imported oil is the cure. More expensive oil is good for green energy development.

The Saudi royals are cheating, lying murderers. We spend huge sums militarily to protect them to assure our access to their oil which we no longer need. Import tariffs should be a bi-partisan issue. The powers that be have personal reasons for continuing to kiss the Saudis’ asses.

First, more efficient assets can be restructured to shift refiners to the left-hand side of the cost curve. Second, refiners with marginal assets should be looking out for the best approach and timing for exit.

https://www.mckinsey.com/industries/oil-and-gas/our-insights/global-refining-profiting-in-a-downstream-downturn

I should have added this comment to last post, sorry.

That analysis above is a fine metaphor for where economic stuff is headed, meaning, weak entities, industries and individuals, who are over leveraged, will need to acknowledge this come to Jesus pandemic. That also will include weak political parties reliant on total bullshit.

We all know global GDP was in decline before the virus and we know the vast majority of all Wall Street corporations had weak earnings and bubble accounting, so, as with time tested Darwinism, survivors will adapt by being smart versus relying on absolute piracy.

I assume online shopping was already a growth industry that will quickly adapt, and robotics will take full advantage of Human frailty. The end ….

It would be a failure of vision to separate the current crisis from the one on the horizon. A series of makeshift interventions may assist vulnerable oil-producing countries in rapid recovery, but what they need is a concerted strategy to wean themselves off their dependence on fossil fuel exports. Otherwise, the oil counter-shock of 2020 will be no more than the first step on a path toward terminal crisis.

https://foreignpolicy.com/2020/04/23/the-coronavirus-oil-shock-is-just-getting-started/

How do you think we feel here in Alaska?