Mega-cap tech blew the proverbial doors off last week when the companies which, together, make the difference between the S&P 500 being positive for the year or negative, reported quarterly results that were even more impressive on many metrics than bulls imagined.

That was good news for a market that lives and dies by just a handful of names. You’re Linus and mega-cap tech is your security (or “securities”) blanket.

And yet, as Nomura’s Charlie McElligott writes on Tuesday, US equities are increasingly “likely to ‘agitate'” and otherwise “trade sideways over the next month”, tech “safety blanket” or no.

The figure (above) shows Nomura’s SPX Sentiment Index which measures a variety of inputs, including breadth, RSI, vol, put/call, momentum and credit spreads. It’s sitting in the 94.5th %ile since 2004. McElligott notes that “backtests when at or above this level show we struggle and in aggregate go nowhere out 1 month in the S&P 500, before picking up and rallying again out 3m-6m-12m”.

The good news (as noted here on Monday) is that we’re “deep” in long gamma territory, insulating equities from the kind of selling-begets-selling dynamic that’s exacerbated so many of the big directional moves witnessed over the past several years.

Looking out across systematic positioning, Nomura’s CTA model shows that overall (i.e., cross-asset) leverage is sitting in the 95th %ile. “This is a function of realized vol. compression growing the book to extremes”, McElligott writes, calling it a “standard ‘stability breeding instability’ setup”.

Again, that’s cross-asset exposure. Bond exposure is in the 99th %ile. Clearly, that’s a crowded trade which potentially sets the stage for a reversal in September, when a heavy IG calendar could help pressure yields higher/UST curves steeper, leading to an unwind in a variety of duration-sensitive equities expressions. That’s generally McElligott’s medium term view (for more, see “Nomura’s Charlie McElligott Outlines ‘The Largest Pain Trade In The World’”).

As a quick aside, Bloomberg’s Stephen Spratt on Tuesday notes that while the MOVE at record lows “implies a quiet period ahead… summer is a dangerous time to be short vol.”. He cites the election, geopolitical jostling, and seasonal trends both in liquidity and in rates vol. itself. “Summer may be the time to chill out, but not so much in the rates vol. space”, he cautions.

Getting back to McElligott, CTA exposure in equities on Nomura’s model is in just the 42 %ile.

That said, signals for US small-caps, Japanese equities, and German stocks have flipped from neutral to varying degrees of “long”, and McElligott estimates some $110 billion of mechanical buying across global futures on Monday alone.

For risk parity, the longer look-back window means the worst days of the panic are “still embedded” (as Charlie puts it), which means gross exposure can’t rise — remember, “volatility is the exposure toggle”.

Vol.-control, on the other hand, has been mechanically adding exposure for quite a while, given the shorter “memory” (if you will) of the model.

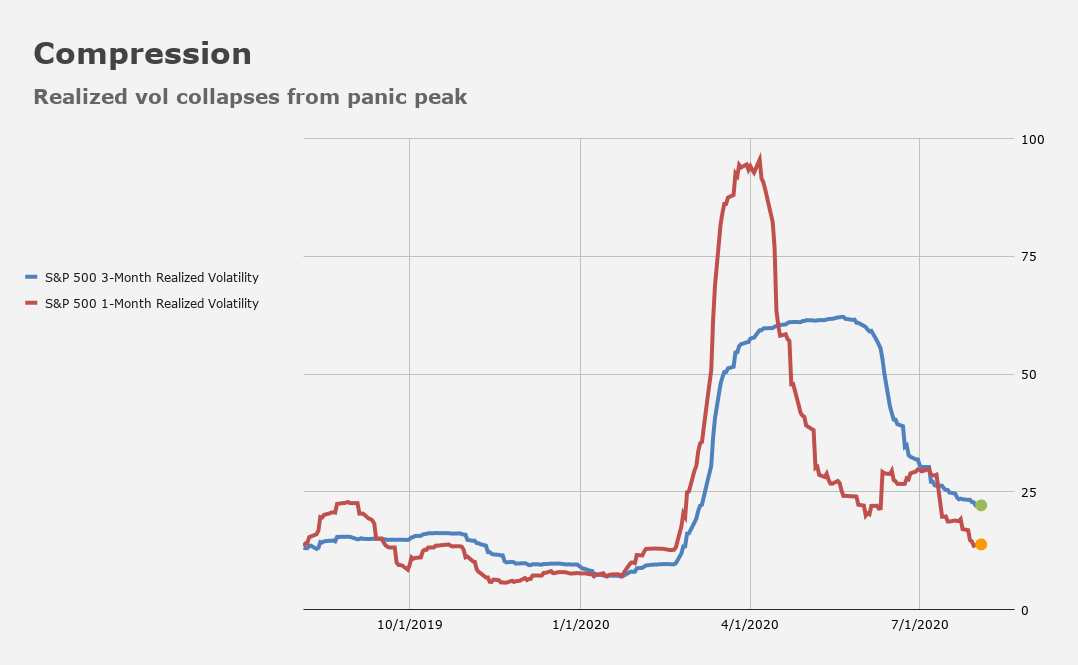

“Our model looks at the max of either the 3m realized or 1m realized in SPX, so with the enormous compression under its own prior ‘weight’ and actually seeing 1m (now 12.7 vols) crash downward below 3m (22.7), the 3m trailing realized vol window is what is driving the allocation for vol.-control”, McElligott says.

And so, vol.-control has been a buyer since late June, when the truly horrific days of March started to drop out of the look-back. McElligott estimates some $31 billion in buying over the last month, but cautions that this bid from the vol.-control universe has faded, and could see incremental selling over the near-term depending on the conditions.

Ultimately, the above paints a mixed picture as stocks confront a somewhat daunting August seasonal.

You can draw your own conclusions, and, I suppose, take comfort in the greatest security blanket of them all — not tech, but rather the technocrats in the Eccles Building, who are now acting as America’s caretaker government.

{kind=link}