How seriously should we take alternative measures of the world’s most important macro readout?

That wasn’t an especially pressing question prior to this year, notwithstanding persistent concerns about BLS response rates.

Until 2025, America’s preeminent macro statistics agency was still nominally independent and, more importantly, at least open and staffed enough to produce a monthly jobs report.

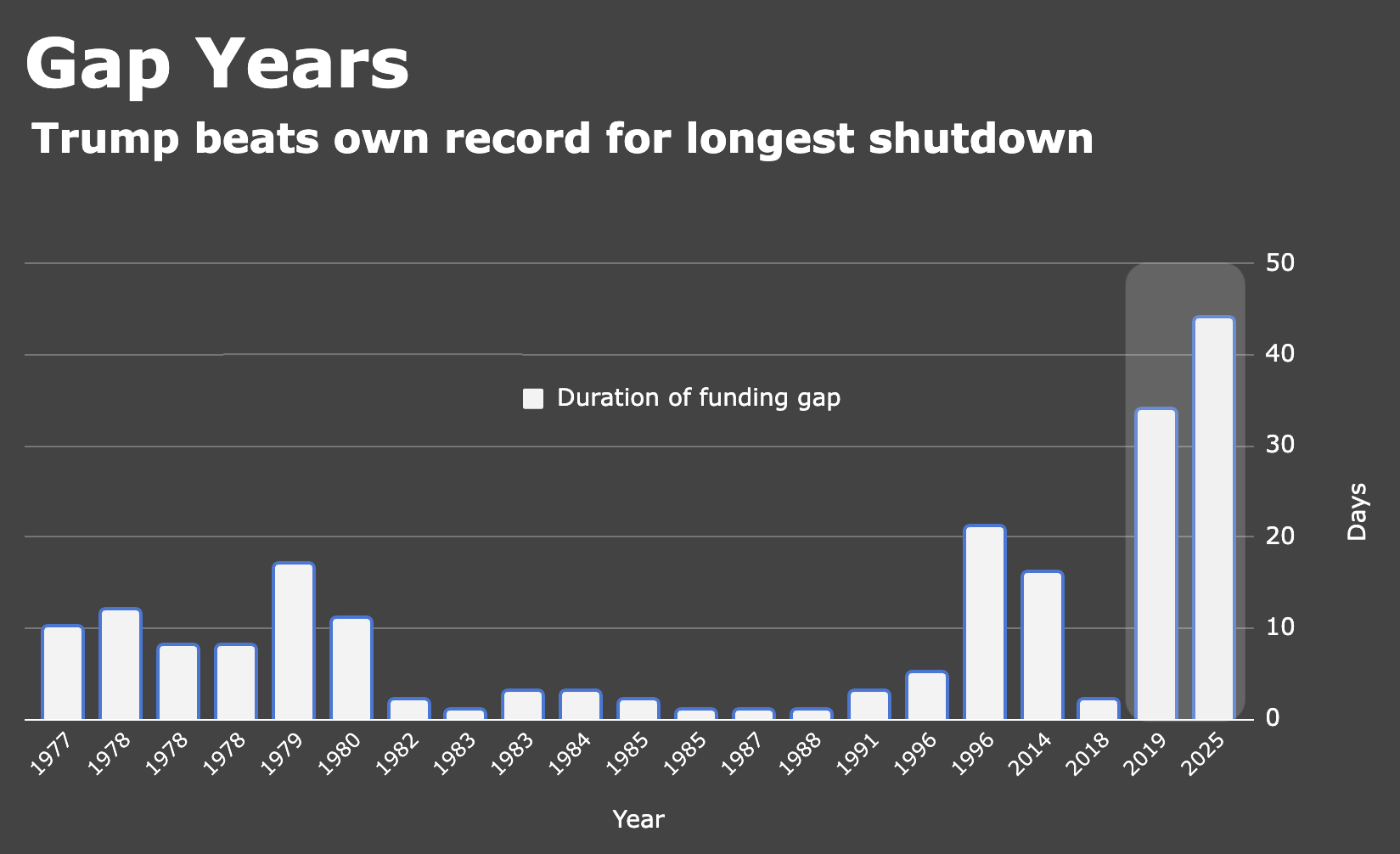

Then Donald Trump shook things up, first by championing a slapdash effort to cut federal payrolls (thereby inhibiting some aspects of the data collection process). Then he fired the head of the BLS for publishing revisions he didn’t like. Then he shut down the government and partially canceled the October jobs report (and that month’s CPI report).

Like everything else to do with Trump, that’s all so crazy as to induce a begrudging chuckle, unfortunate as it is. Once the giggles subside, it’s all sighs and laments. Because Trump’s actions — to say nothing of his words — have amplified preexisting concerns about data quality at the BLS, particularly around the monthly labor market numbers.

So here we are, pondering a world where private sector efforts to measure the hiring (or, more recently, firing) impulse might be more reliable (and more timely) than the government figures. ADP’s stepped up with a weekly update on private sector hiring in addition to their monthly tally which showed employers shed the most jobs since 2023 in November led by small businesses.

Another, lesser-known effort to guesstimate hiring in America is the Revelio Labs monthly jobs report. As a quick reminder, Revelio essentially tries to replicate the BLS’s release using individual-level data from more than 100 million online professional profiles.

For whatever it’s worth to you, that metric showed a second consecutive decline in data published Thursday. According to Revelio, the US shed 8,892 jobs in November after losing a revised 15,457 the prior month.

As the figure shows, this alternative metric suggests the US has lost jobs on net in five of the last seven months. Losses were led by leisure and hospitality, manufacturing and retail in November.

There’s not a “consensus” estimate for this print (or not that I’m aware of), but directionally at least, it’s consistent with pretty much every other indicator of the US labor market, which is to say it suggests the hiring impulse isn’t just waning, it’s gone.

Thursday’s figures came on the heels of the ADP data mentioned above and another disconcerting read on job cuts and hiring plans from Challenger.

Meanwhile, the final update for November on the Chicago Fed’s suite of labor market indicators — yet another new edition to the toolkit discussed here — suggested the unemployment rate in November was 4.44%.

As is clear from the copious amount of digital ink I spilled this week editorializing around alternative labor market indicators, it won’t be possible for the Trump administration to obscure a downshift in hiring if in fact that’s part of the plan.

I’m not necessarily saying The White House intends to manipulate the BLS series, but let’s be honest: When you fire the nation’s chief statistician at the first sign of labor market weakness, you’re inviting conspiracy theories.

Public suspicion would only grow in the event ADP, Revelio, Fed metrics and all the rest start to deviate materially from the “official,” government-sanctioned numbers which, if tallied honestly, probably don’t suggest America’s experiencing anything like the “golden age” Trump promised in his second inaugural.

{kind=link}

New title, “Fool’s Gold.”

The BLS jobs report is less and less reliable, even absent intentional manipulation. The survey response rate is plunging, illustrated by – but not remedied through – large revisions. The birth-death adjustment is always wrong at economic turning points. Many BLS personnel have left. Investors will increasingly rely on private labor data. Algos may be later to switch. The private labor data, and much other govt and private data, show the non-AI economy rolling over into recession in real-time. The prospect of a zombie Fed and a 40% AI weight has so far insulated the S&P500 index. Bonds don’t have AI “insulation”. The 70bp drop in 10Y yield is not a good sign. Neither is the -160bp drop in short yields.

The more apparent goal in Washington is to grind everything to a halt, perhaps in the hope that it can never be restarted again.