Were you curious as to what America’s largest bank expects for US equities in 2026?

No? Me neither. But I gotta pretend. Because some readers are here for that sort of thing, God bless ’em. And Lord knows I aim to please.

With that in mind, Jamie Dimon’s research department — which I doubt he’s ever visited — is bullish on the S&P in the new year, where that means Dubravko Lakos-Bujas’s year-end 2026 target is 7,500.

Part of the rationale centers around FOBO, and no that isn’t a new line of streetwear from Daymond John. Rather, it’s another acronym to add to a market lexicon full of them.

“Both corporates and governments across the world are racing to invest in AI out of fear of becoming obsolete,” Lakos-Bujas wrote, in his outlook. So that’s FOBO, and it’s set to perpetuate “an AI-driven supercycle fueling record capex and rapid earnings expansion,” according to JPMorgan.

It’s not just AI. There’s a macro-policy narrative too. The bank expects double-digit gains for equities more generally — i.e., not just in the US, and not just in the developed world, but globally and across emerging markets — on “robust earnings growth, lower rates and declining policy headwinds.”

How’s that for a generic bull case? (I’m just kidding, Dubravko. Seven times out of 10, the generic bull case turns out to be right.)

He did toss in some eye-watering statistics which, while not unfamiliar by now, are nevertheless worth a mention. What JPMorgan calls the “AI 30” account for almost half of S&P market cap. The Mag7 and Broadcom alone make up almost 40%, which Lakos-Bujas noted is up from 23% when OpenAI introduced ChatGPT to the world three years ago.

Although he conceded that concentration’s now more extreme than the Nifty Fifty-era peak, Lakos-Bujas defended narrow market breadth along the usual lines. “Today’s concentration is primarily in Quality Growth names with strong profit margins, resilient cash flow growth, disciplined capital returns and still low credit risk profiles,” he said.

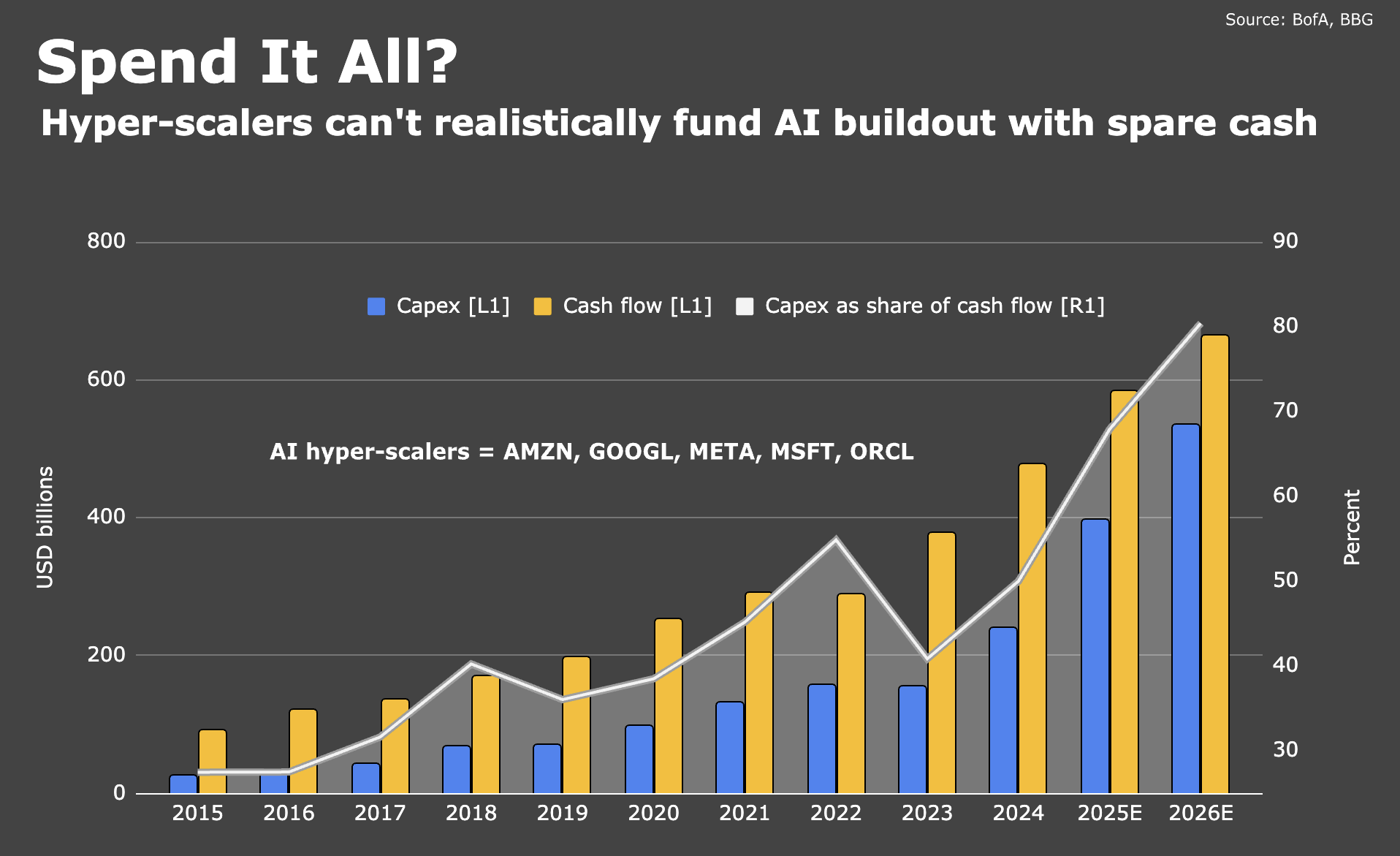

As such, the mega-cap leadership’s “uniquely positioned to deploy capital in size when new opportunities, such as AI, emerge.” (To make the obvious joke: They’re deploying capital, alright. So much of it, in fact, that if they funded capex solely out of cash flow, there’d only be $2 out of $10 left over for other things like, say, buybacks.)

The table summarizes JPMorgan’s house calls for global equity benchmarks.

If you’re wondering whether the bank has a “bull case,” which is to say a scenario that’s even more optimistic than their already-bullish base case, the answer’s “yes.”

The 7500 SPX target assumes just two more Fed cuts “followed by an extended pause.” If the Fed were to deliver additional cuts on top of those two, JPMorgan “see[s] greater upside with the S&P 500 likely surpassing 8,000 in 2026.”

Don’t laugh: Morgan Stanley’s Mike Wilson, erstwhile incorrigible bear, sees upside to SPX 9000 in a best case.

{kind=link}

Personally, I like TINA.

Based on JPM’s targets, we should aggressively re-allocate from the S&P 500 to ex-US markets, which have equal or better upside, are lower valued, way less exposed to an AI slump, and offer possible FX gains as the Fed cuts and cuts.

“Crack-up-boom” or just “Boom.” The bear case I keep wrestling with is a lost long end, Fed loses credibility (which is already happening), and equities rocket up on panic buying to escape inflation. Both scenarios say stay out of credit duration and junk.

“Low credit risk profiles”, yes for the AI leaders but is their AI onslaught low risk. How many winners can there be and computer tech is famous for the curveballs that magically appear. I’m no tech geek, but quantum computing seems like it could be a threat to the current strategy. If quantum computing overcomes its error problem, will that make Nvidia chips obsolete. If anyone has insight on how these technologies might work together or not, I’d love to hear it.

These all seem like a top –

a.) The boat is getting crowded on the bullish side.

b.) New terms like FOBO are being coined to justify continued bullishness, despite 3 back-to-back well above average years.

Maybe they can keep it going for a while (until Drumpf has to face up to mid-terms), but unless you are nimble, you could be left holding the bag, AI-bust or no AI-bust.

I meant seem to be indications of being toppy*