When we channel James Carville to declare “It’s the economy, stupid,” what we’re really saying in 2026 is “It’s the wealth effect and the AI spending, stupid.”

That’s it. The US economy lives and dies these days by two things: AI investment and consumer spending powered by financial asset inflation.

On the former, we just found out that Alphabet, Amazon, Meta and Microsoft are likely to spend nearly $720 billion this year on capex (read: AI compute), almost double last year’s outlays and far more than analysts expected just four months ago.

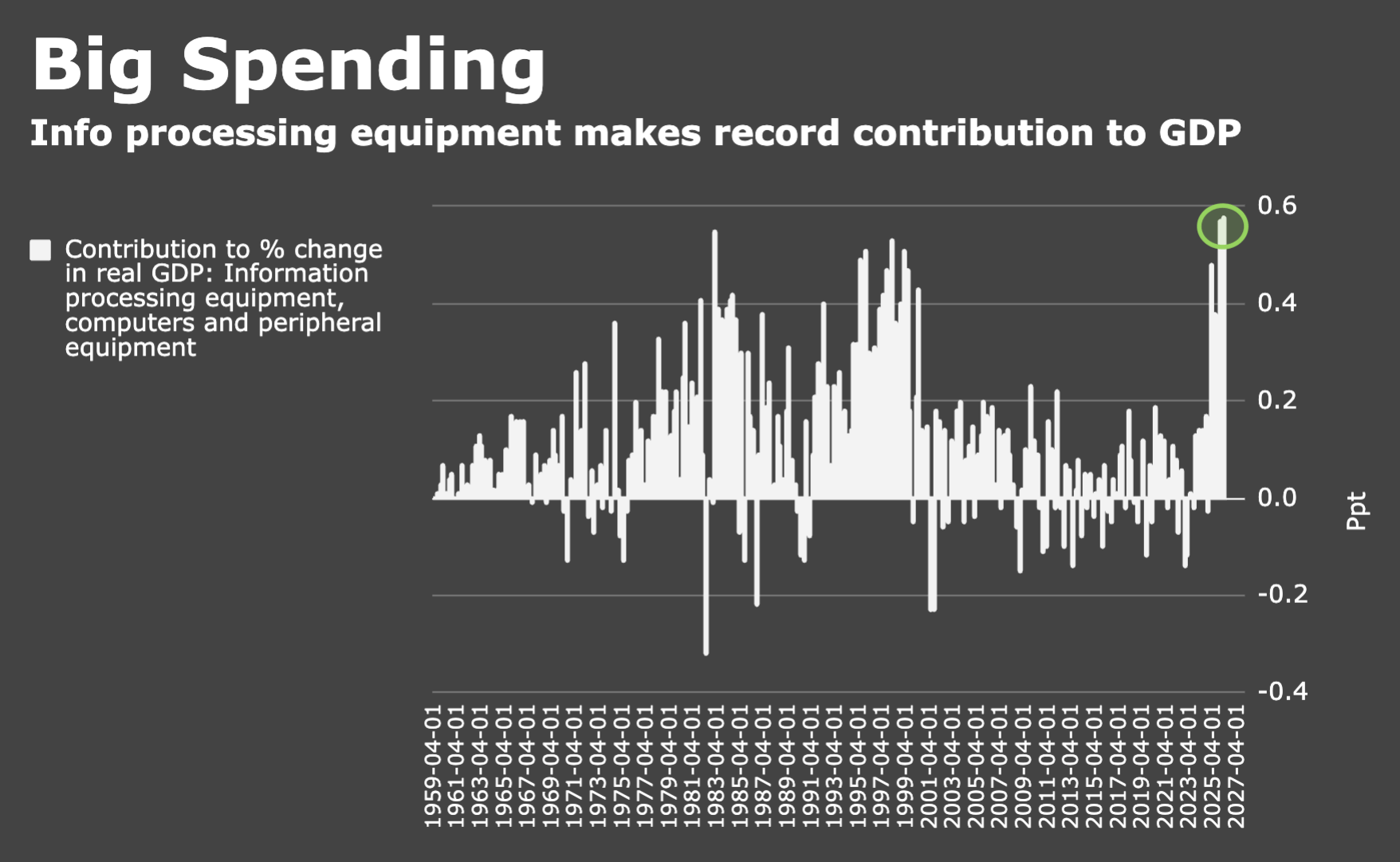

That spending, and other AI-related outlays across corporate America, is having a big impact on the growth aggregates. According to the St. Louis Fed, AI was responsible for nearly a full percentage point of GDP growth during the first nine months of 2025, a larger share than IT components during the dot-com boom.

The figure below shows you the GDP line item which tallies the contribution to real growth from information processing equipment, and specifically computers and “peripheral equipment.”

At 0.58ppt, it was the highest on record in the advance read on Q1 growth released this week by the BEA.

Note that the “old” record was 0.57ppt notched in Q4. So, in each of the last two quarters, that particular line item eclipsed levels seen during the height of the dot-com boom.

Now to the wealth effect. The figure below shows you the quarterly change in household equity wealth plotted with the quarterly change on the S&P 500.

The Fed series on household net worth comes on a (long) delay, but you can figure on something like a ~$2 trillion hit for Q1, when stocks slipped on Iran war jitters.

April’s 10.5% gain for the S&P recovered all of that and then some. It’d be absurd to extrapolate one month to the entire quarter, but if you were inclined, the chart gives you a sense of what such a gain, if it held through July, might translate to in terms of household equity wealth.

Of course, if you don’t own (m)any stocks, that’s irrelevant. But most of us long ago gave up on the idea that the US economy works for everyday people, so let’s not be obtuse — we can litigate that another time.

Relatedly, the stock rally from the March lows helped snuff out a nascent tightening impulse on the Chicago Fed’s gauge of national financial conditions.

As a quick reminder, that index is — and I’m quoting from the official explainer page — “constructed to have an average value of zero and a standard deviation of one over a sample period extending back to 1971.” If the index is positive, financial conditions are probably tighter-than-average. If it’s negative, they’re probably looser-than-average.

The annotations are a reminder or, for the youngest readers, a wakeup call: With the requisite sympathy for the deceased, and while acknowledging, to the extent it’s possible to ponder the unfathomable, the incomprehensible scope of the suffering associated with the pandemic, in terms of market stress, COVID was a walk in the park compared to the GFC.

“The strength of the equity market has once again provided a constructive backstop for consumption expectations in light of the supportive impact for the wealth effect,” BMO’s Ian Lyngen remarked, commenting on all of the above. “In March, the risk that substantially higher oil prices led to tighter financial conditions was a consideration that supported the doves’ case for rate cuts [but] that argument has since lost its relevance with the S&P 500 above 7200.”

{kind=link}

Sure seems like the US economy is going ‘all in’ on AI. If it doesn’t meet the hype there is going to be a lot of tears shed. There was an article today in The Verge about Gen Z starting to push back on AI. Cracks anyone?

What if one of the most profitable uses for AI is to combine with hedge funds/capital, quantum computing and a short/long player disguised as an equity analyst?

The US equity market would be a great place to “play”.

Momentum is momentum! 🙂

IMHO using AI everyday. It’s a fantastic assistant but its unreliable. You can’t give it full control unless the results don’t matter. So you will get significant improvements in productivity but it’s use remains limited. It could be a significant amount of time before they completely fix the reliability.