While previewing the release of key activity data for the Chinese economy, I not-so-gently suggested that if “things keep going the way they’re going” Xi might decide to “gradually pare the number of top-tier economic updates made available to market participants.”

Fast forward a day and sure enough, China omitted the youth unemployment rate while disclosing a hodgepodge of critical figures, including retail sales, industrial output and fixed asset investment.

The jobless rate for China’s youth raised eyebrows in recent months after surging to a record high. Markets noticed the omission. Without knowing the number it’s hard to say, but unless it was markedly worse compared to June’s rate, you could easily argue that leaving it out did more damage to sentiment than just reporting another increase.

By the time you read these lines, the figure may be published or otherwise known. I have no idea. But the fact that it was left out initially spoke volumes. The Party’s silence on that number was indeed deafening.

To reiterate: If the situation continues to deteriorate, no one should be surprised if the Party chokes off the flow of information to investors. No matter what kind of spin the financial media tries to put on Xi’s government, at the end of the day it’s an authoritarian regime and a black box.

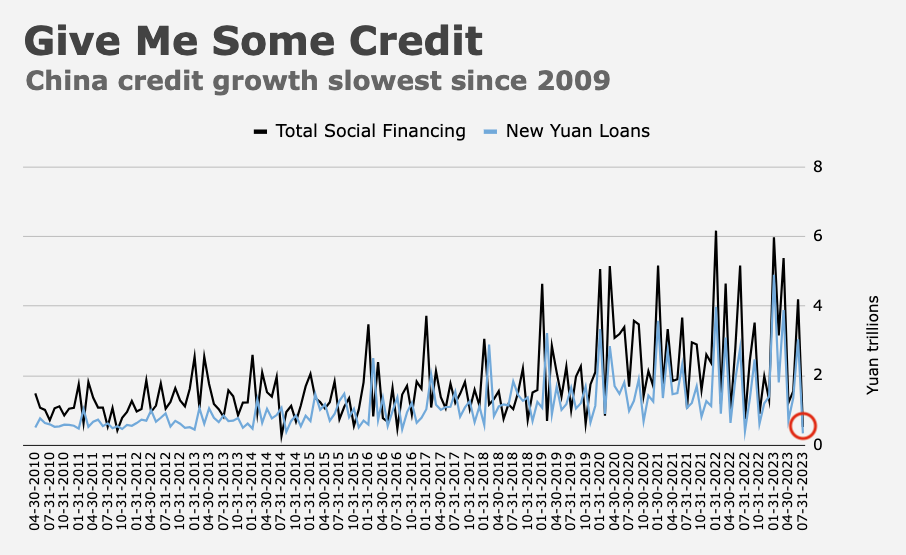

The activity data was predictably bad. Retail sales rose just 2.5% YoY, underscoring the message from July’s steep deceleration in credit creation and deflationary CPI print. That message: China has a demand problem.

Industrial production rose 3.7%, well short of estimates, and cumulative fixed asset investment missed too.

You might suggest these are only “misses” versus sell-side estimates, and that if buy-side expectations were factored in, the figures wouldn’t be all that surprising. But the market (somewhat unfortunately) benchmarks to Bloomberg consensus. So the data counted as poor.

Beijing is plainly concerned. The PBoC delivered a surprise rate cut on Tuesday, the second in three months.

The 15bps MLF reduction was the largest since 2020. China also cut the seven-day repo rate by 10bps.

Those moves will pressure the already weak yuan, likely compelling the central bank to lean harder into the fix to put a floor under the currency at a time when US monetary policy is the tightest in recent memory.

This all bodes very (very) poorly, and it came on a day when markets were warily eyeing renewed stress in the property sector and tremors in China’s labyrinthine shadow banking complex.

Maybe the White House was onto something with the whole “ticking time bomb” characterization of Xi’s economy.

{kind=link}

You’re going to get yourself on a list.

He’s already on several!

Remember when China was about to overtake the US as the world’s most powerful economy? I believe it was right after Russia was about to overtake us. Spin is a funny thing.

Looking forward to the puck’s future location, as it were, what will the CCP ultimately do about this?

Continue the current course (lower borrowing costs, ease business restrictions, mandate stimulus by local govts, restrict reported economic data, etc.?

Large-scale fiscal stimulus, perhaps even demand-side household-focused, at the cost of fiscal rectitude?

Fundamental economic reforms to increase household income and reduce government/SOE economic share?

Other?

Which Xi chooses has large investment implications, e.g. for commodities.

Sorry, I meant to finish with a question: What is your best guess?

Or a nice war to rally the populace.

Anyone hear that Kyle Bass interview at the Hudson Institute?

The Taiwanese elections in January will be “interesting”, to say the least. A large slide in the share of votes for the pro-independence party would complicate things for those who call for military action to defend TSMC.