There was a lot of talk last week about a purported regime shift for the dollar.

Cooler-than-expected US inflation and a sharp decline in real yields catalyzed the worst week for the greenback since November, prompting some to speculate on “the end of an era,” as Bloomberg put it. The dollar, some reckon, is poised to enter a “multi-year downtrend.”

Suffice to say this debate, like every other market and macro debate in the 2020s, isn’t easy to settle. If the question is “Where to now?” the answer is a Magic 8 Ball-esque, “Reply hazy, try again later.”

In a new note, Morgan Stanley strategists including David Adams attempted to make sense of the cross-currents while turning neutral, “but not broadly bearish,” on the greenback.

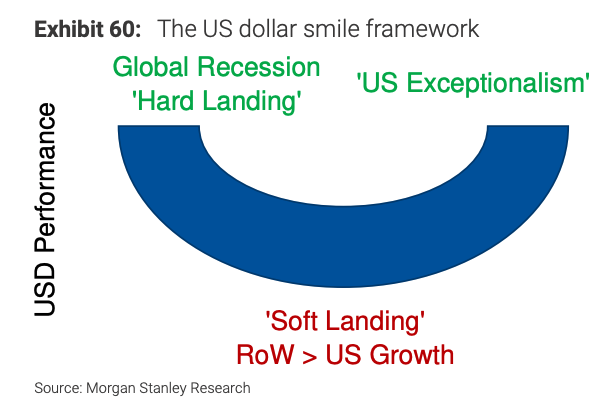

Previously, the bank assumed the demonstrable growth divergence in favor of the US would be conducive to dollar strength consistent with the “smile.” Alas, it hasn’t exactly worked out that way in 2023.

Now the downside US CPI surprise risks tipping the scales in favor of the above-mentioned downtrend or “‘regime 1’ trading,” as Morgan Stanley describes a conjuncture defined by falling US reals and buoyant risk appetite.

Plainly, that’d be agreeable to investors, particularly when juxtaposed with 2022’s “everything rout” perpetuated by the so-called “dollar wrecking ball” dynamic. Last week was a reminder that when the dollar is on the back foot, it’s generally good news for assets of all sorts — US equities, global equities, EM FX, gold, bonds and commodities all rallied simultaneously. Everyone was a winner+.

As Morgan Stanley put it, “such a change would be meaningful for currency (and macro) markets [as] regime 1 tends to see broad-based USD weakness, gains in commodities and equities, and lower cross-asset vol.” The last time we saw such a regime (if you don’t include last week) was Q2 through Q4 of 2020.

But, again, Morgan isn’t outright bearish on the dollar. Why not? “In short, the rest of the world matters too, and short USD is a clear consensus trade,” the bank said.

“USD positioning [is] now back at levels rarely exceeded and infrequently held for long,” Adams and his colleagues wrote, of the figure on the right above. “Such positioning make[s] it less compelling for investors to ‘chase’ a narrative, particularly one as consensus as short USD.”

Beyond positioning, there’s significant ambiguity about the path of inflation, and thereby policy outcomes and rates, in the rest of the world. Without clarity on that, it’s difficult to draw any firm conclusions on the likely path for the dollar.

For example, if inflation doesn’t moderate substantially and sustainably outside the US, central banks may be inclined to raise rates further or, at the least, to keep rates restrictive. That’d create a policy divergence with the Fed, but crucially, it’d also weigh on global growth. Those two dynamics could offset.

“Falling inflation is a necessary condition for reduced policy tightening, which both weighs on real rates and bolsters growth expectations,” Morgan Stanley remarked, adding that they’d be more confident in an unequivocal bearish stance on the dollar if rates were telling the same story across locales, as they generally were in 2020 (as shown in the right-hand figure above). Real rates falling in unison would bolster global growth and risk appetite to the detriment of the dollar, which would feed back into the growth impulse and back into investor sentiment, in a self-feeding loop.

Currently, we’re not there, though. And until we get there… well, ask the Magic 8 Ball. “In order to see the dollar weaken materially, a necessary condition may be to see real rates falling not just in the US but in the RoW too,” Morgan Stanley went on. “If that’s not the case, it’s harder to [argue] for a large USD-negative move.”

{kind=link}

China is slowing significantly, the Eurozone has been lagging U.S. economic performance for the better part of a decade, and everyone would like to have our military, our tech sector, and our relatively unconstrained economic system (as imperfect as it may be). When it comes to a weakening dollar or, more improbably, its replacement as the world’s reserve currency, count me in the noise-and-fury-signifying-nothing camp.

Not hearing the narrative yet, but expecting to soon: “this is as good as it gets.” We can call it the Jack Nicholson Economy.

It feels like we’re going to look back on June/July in 3-6 months time and feel this narrative was correct. Everything has gone “right” for the economy. Markets and economies are not linear, this makes me think we have 2 paths from here:

1- back to stagflation

2- Retracement

We just had a fantastic mini economic boom. There are numerous dynamics about to pivot meaningfully. Plus, economic booms don’t tend to live long when total households are contracting.

https://fred.stlouisfed.org/series/TTLHHM156N#

You might be right. On your last point, I would argue that, over the next 20-30 years, demographic trends in the U.S. are the most favorable of any developed country + China. (Keep an eye on India, where demo trends suggest it could pretty quickly become one of the five, if not three, largest economies in the world.)

Interesting point RE demographic trends, however, the data I’ve seen show Millennial HH formation peaking in 2027; though the analysis was a top down macro generational view and did not take into consideration HH contraction due to overall economic trends. Essential I believe the read to draw both theories 2027 Millennial HH peak and current HH contraction is esoteric dynamics (Pandemic housing demand) have pushed HH formation above macro secular trend and the recent contraction is a reversion to trend.

Are there other demographic trends you are thinking support your perspective? I’ve been re-thinking a lot of thoughts RE retiring Boomers based on new theories regarding spending wealth transfer, etc.