The range of possible policy outcomes is expanding in the US.

I assume this is obvious to my non-US readers, but just in case: That matters to everyone, everywhere.

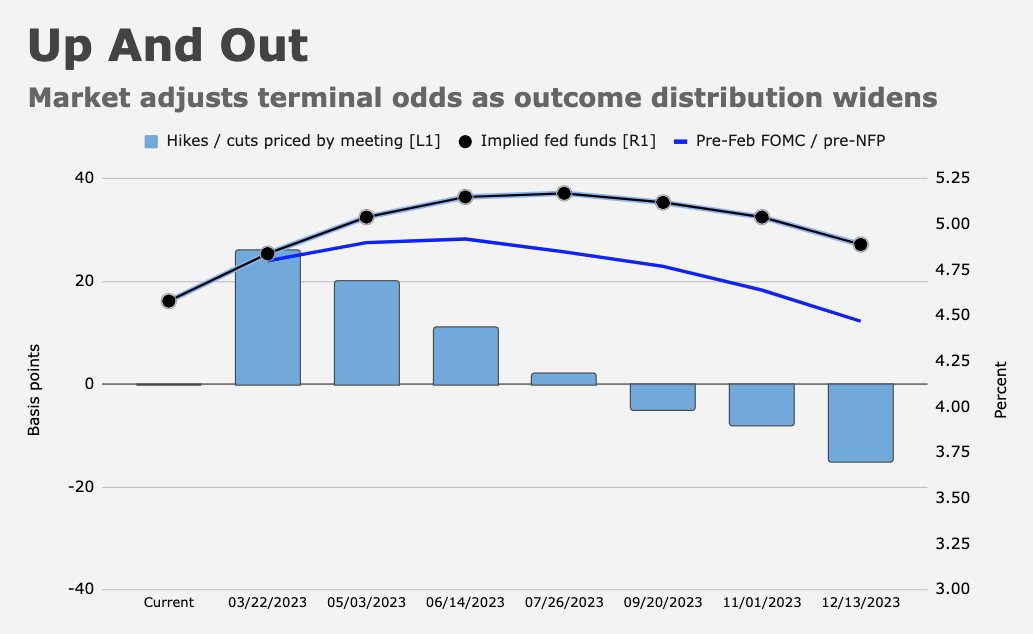

The perception of a wider distribution for the Fed comes courtesy of a resilient US labor market, and the implications of that for personal spending, housing and the services sector in general.

As discussed at length in “Hawks And Doves On The Carousel Of Madness,” terminal rate pricing has moved markedly higher, and next week’s US CPI report is set up to be a binary blockbuster.

When it comes to the outcome distribution discussion, it’s not just a nebulous macro talking point. “For the first time in forever, we have some tangible pockets of dealer ‘short convexity’ developing,” Nomura’s Charlie McElligott said, in a Friday note, referencing large VIX upside trades and sizable premium spent on puts in apparent recession plays.

For what it’s worth, vol-of-vol is up pretty handily since last week. VVIX is the highest since October.

That’s not a coincidence. Regular readers will doubtlessly recall that everything shifted midway through that month, when terminal rate pricing settled (nervously) around 5%. Rates vol (or at least the MOVE) receded, equities turned around and before too long, the dollar was decidedly on the back foot. It’s possible that the “up and out” shift in peak-rate pricing presages a reversal of the friendly environment that’s generally prevailed since October.

“VVIX always knows,” McElligott said. “Volatility of volatility is signaling an inflection in the probability path, as tails are again bid and with the chance of a new price range coming back into play, synching-up with next week’s crucial data,” he went on.

Charlie struck a somewhat ominous tone. Funds and market participants in general have rushed to add exposure into what, until this week, was a runaway rally. That, in turn, meant hedging the newly-added risk, and all ahead of OpEx and a loaded data docket which, in addition to CPI and PPI, includes retail sales.

“[The] likely binary market interpretation of next week’s economic data — which for now is loading with ‘hot’ / ‘hawkish’ expectations, risking a ‘de facto dovish’ response for anything less — is the perfect scenario for a wider distribution of market outcomes going forward,” especially considering the “frighteningly very-hedged OpEx” around the numbers, McElligott explained.

Suffice to say the risk of large directional moves exacerbated by hedging dynamics and systematic flows is elevated. The table below shows CTA trigger levels for the S&P and small-caps on Nomura’s model.

“A ‘hawkish’ data dump across CPI and retail sales risks opening up a move back below the acceleration point of Spooz 3,975, where not only would we lose some large gamma support, but as we currently see it, would also be the level where as of today, our CTA Trend model would project the S&P to flip from its current ‘+40% Long’ back through both the ‘-30% Short’ signal all the way to ‘-100% Short’ again,” McElligott observed.

But remember: It’s binary. If the data comes in cool, or simply fails to live up to the hawkish “whispers,” equities could rally and vol could compress into OpEx, alongside a repricing back lower in terminal rate expectations. That could make for an explosive move higher.

{kind=link}

Are there any notable reversals back up in CPI inputs big enough to make the headline numbers miss? It seems like they are trending down but is there a spoiler lurking?

I know top pros (CTAs) do this for a living but I’ll bet my new hat profs don’t teach any of this to undergrad investment students and I know none of my teaching colleagues had a clue.