The Bank of Japan is now effectively at war with the Japanese finance ministry, an absurd outcome months in the making.

Masato Kanda, Japan’s top currency official, confirmed the first intervention since 1998 on Thursday, the same day Haruhiko Kuroda stuck assiduously to the script while reiterating the central bank’s intention to remain steadfast in monetary accommodation for the foreseeable future.

“We won’t raise rates for some time,” Kuroda said, adding that the bank debated the proper course of policy “thoroughly,” and “concluded that we will continue with monetary easing.”

I suppose this is obvious, but BoJ policy won’t likely be changing under Kuroda, for whom easing in the service of engineering sustainable 2% inflation is tantamount to a religious imperative. On Thursday, he said the bank’s forward guidance could be in place until 2025. “You can expect no change to our forward guidance for about two to three years,” he said, at today’s press conference.

It’s possible, I’ve suggested, that Kuroda is now prioritizing his own legacy over the national interest. Inflation in Japan is nearly a full percentage point above target, and Kuroda’s defense of the cap on 10-year Japanese government bond yields is the driving force behind the yen’s worst year on record (figure below).

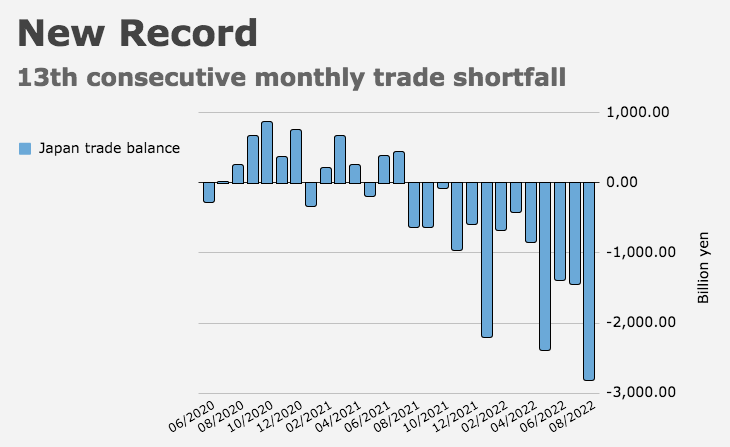

The currency’s inexorable slide is contributing to a terms of trade shock as commodity prices remain elevated. Japan notched its largest trade deficit on record in August, the 13th consecutive monthly shortfall.

Kuroda’s obstinance came hours after the Fed delivered a third consecutive 75bps rate hike, hours before the Bank of England was poised to hike rates for a seventh consecutive meeting and around the same time the Swiss National Bank exited negative rates, leaving the BoJ alone in monetary Neverland.

There’s “no need for Japan to remove negative rates because others have done so,” Kuroda insisted. He cited “clear differences in the price situation.” His remarks pushed the yen towards 146.

Kanda’s intervention drove a sharp rally (figure below), but the MoF is fighting a losing battle. Both the fundamentals and monetary policy argue for more yen weakness, particularly with the Fed now telegraphing a more aggressive near-term rate path.

“We took decisive action just now,” Kanda declared, less than an hour after Kuroda finished speaking. “The government is concerned about excessive moves in the FX markets,” he said, blaming “speculative” behavior for “sudden and one-sided” price action.

Again, the problem isn’t “speculators.” If speculators feel emboldened, it’s because Kuroda is encouraging them, but at this point, at least some “speculators” are betting the government will eventually call time on the BoJ. JGB shorts and wagers on a yen rally may seem a fool’s errand now, but the moment the BoJ relents (if they ever relent), the snap higher in yields and the knee-jerk rally in the currency will be something to behold.

For now, though, the MoF may well find that its “decisive” interventions come to nothing. Kuroda is unmoved and unbowed.

“With the Fed turning ever more hawkish and the BoJ still printing money, it looks like the Japanese government wanted to stop a quick run to 150,” ING’s Chris Turner wrote. “Japanese authorities could well be doing battle with the FX market for the next 6-9 months as the dollar stays strong.”

{kind=link}

Kuroda fought for years to arrest stagnant or even falling prices in Japan. Prior leaders at the BOJ failed at this. While we may disparage his policy, it is well to understand what has gone down in Japan since the property bust / banking problem dating back to the late 80s. He may want to stay the course to finally get Japan out of the lowflation regime there. Japan has other problems too- and Kuroda probably would rather have his successors deal with higher inflation down the road, than endure another 30 years of stagnation. I doubt his policy has to do with his personal legacy of maintaining a yield peg.

It’s not a peg. It’s a cap. And that’s part and parcel of the whole discussion. That’s the crux of the issue. Defending that cap is a key pillar of the easing regime, and that defense entails printing endless (literally) amounts of money. You do realize he can be compelled to do this every, single weekday, right? The market can force him to print yen simply by challenging that cap. The more he prints, the more pressure on the currency, and that’s on top of the fact that the cap itself serves to pressure the currency because it means that on any day when 10-year JGB yields are bumping up against 0.25% and US yields are rising, rate diffs are moving against the yen. He’s risking a crisis. In my opinion, he should be removed from his post now, before this gets worse. This wasn’t a problem until this year. He refuses to recognize that the situation has changed. It isn’t tenable. At the least, he has to widen the YCC band. Has to. Has to. Has to. But here’s the rub: As soon as he does, the market will challenge the new upper limit. So he’ll then have to print more to defend that cap. There’s no way out of this unless US yields (and particularly US reals) retreat and the dollar weakens. This isn’t the old “central banks are trapped” cliché that everyone with a soapbox has rolled out over the past dozen years. He’s literally trapped. The failure to appreciate this sort of thing is the stuff crises are made of.

That’s very clear but what’s your take on what happens the moment they let go of the yield cap?

I’d have thought widening it might be a decent half way house but certainly past experiences in the Euro (ecu as it was called back then) system do not impart lots of confidence…

Oh, it’d be even worse! But if that’s the argument for keeping it, then they need to make that crystal clear. So, they need to say something like this: “Look, this was arguably sustainable until this year, but the combination of rising rates across DMs, the plunging currency and the impact of the latter on the trade balance and other fundamental pillars of economic and financial stability, have conspired to make it untenable. However, having acknowledged that, we’ve come to conclusion after a serious internal debate, that scrapping our policy settings in the current environment is even more dangerous than keeping them, and here’s why. [XYZ.] Therefore, these settings will remain in place until conditions are more favorable for adjustments. We want to make it clear that in the interim, attempts to force us away from these settings will be terminated with extreme prejudice. That said, we reiterate that we understand the market’s concerns and that we do intend to address them as soon as it’s feasible. Thank you, no questions today.”

The problem with that, though, if you’re the BoJ, is what do you say about this ridiculous juxtaposition where you have the finance ministry selling dollars while you (the BoJ) are printing yen? The upward pressure on the yield cap is what’s causing this. And, as you suggest in your comment, letting all of that pressure out at once could be very perilous. The yen, for example, could rally so hard, so fast, that it’d be destabilizing. And there’s no liquidity in the JGB market. None. There were no trades in benchmark 10-year JGBs for two straight days this week.

So, I don’t know. That’s really all I’m trying to say with these BoJ articles. I don’t know what the solution is, but I do know that unless US yields and the dollar fall on their own, this’ll remain a pressure cooker.

Understood. As you said, kinda like the Fed, they waited too long to react to the US inflation and its foreseeable impact on US rates. But unlike the Fed, they’re really cornered.