The Fed on Wednesday delivered a third consecutive 75bps rate hike, escalating a historic and, outside the housing market anyway, so-far quixotic, war on the hottest inflation in a generation.

Data showing the monthly pace of core price growth was double economists’ forecasts in August compelled markets to price in some chance of a full-point hike at the September FOMC gathering. Although such a move would’ve dominated the financial pages from New York to London to Tokyo, it wouldn’t have made the Fed an outlier in 2022. On Tuesday, the Riksbank became the second developed market central bank to deliver a full-point rate increase, following the Bank of Canada’s July broadside.

Wednesday’s move brought this year’s cumulative total to 300bps (figure below). Markets generally expected an additional 125bps by year-end, consistent with the new dots.

Already, 2022 stands as the most hawkish year in recent history. I dare say “modern” history, at the risk of making many readers (not to mention myself), feel like antiques.

The new dots suggest rates will reach 4.4% by year-end, and 4.6% in 2023. Terminal rate pricing ratcheted higher in the wake of August’s CPI report. Traders saw 4.5% as the likely peak headed into Wednesday’s decision. The Fed has been at pains to convince markets that rate cuts aren’t likely in 2023. The dots not only suggest rates will end 2023 higher than year-end 2022, but also show support on the Committee for keeping policy restrictive through 2024, suggestions markets will continue to view with extreme skepticism. The out year dots looked a bit less aggressive than expectations, though, even as the 2024 dot was higher than market pricing. Rates will still be near 3% in 2025, the guesstimates suggested.

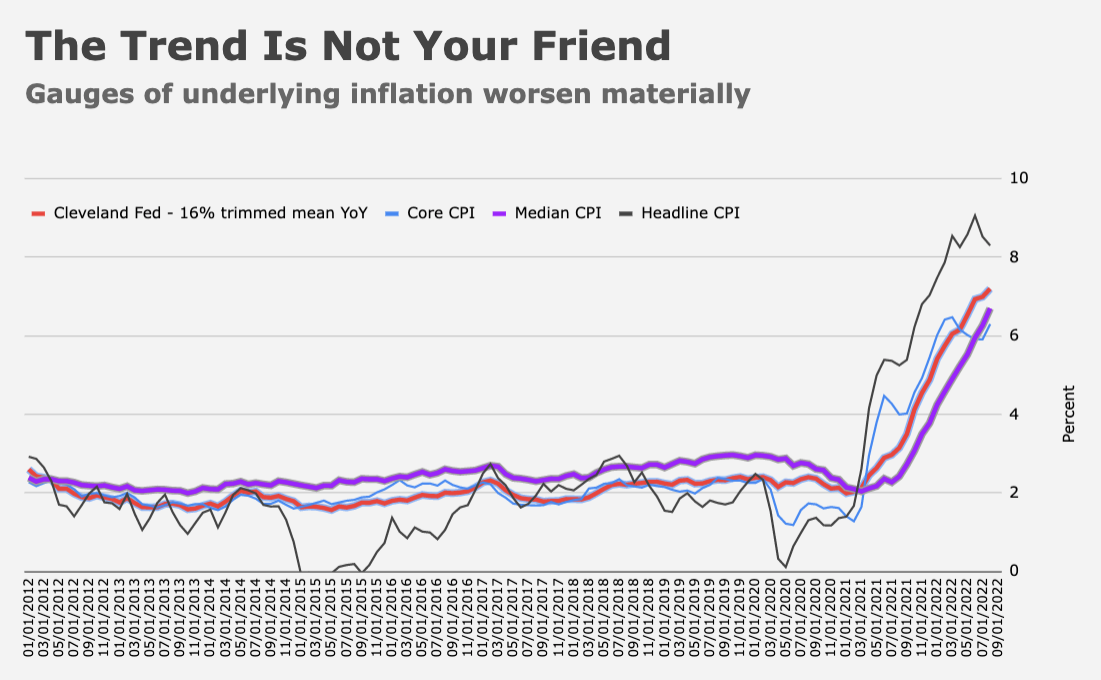

So far, the Fed has little to show for its efforts on the inflation front. Although the housing market has cooled dramatically, and 2022’s bear market on Wall Street wiped away nearly $11 trillion from the value of household equity holdings during the first half of the year, inflation remains elevated and price pressures have broadened out. Measures of the underlying trend suggest it may be difficult to dislodge. On the bright side, consumer inflation expectations have receded with gas prices, and headline price growth should moderate further assuming commodities are a semblance of well-behaved, not necessarily a safe assumption given geopolitical realities.

“Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices and broader price pressures,” the Fed said, in the September statement, which was terse. “The war and related events are creating additional upward pressure on inflation and are weighing on global economic activity. The Committee is highly attentive to inflation risks.”

The new projections found officials marking this year’s inflation forecast to market, as it were. PCE will be 2.8% next year, and 2.3% the year after that, officials imagine (figure below).

Inflation will return to target in 2025. Core PCE is expected to be stubborn at 3.1% in 2023.

Economists were closely eying the new unemployment projections, mostly so they (economists) could suggest the Fed remains wildly optimistic about the prospects for a soft landing. Although Jerome Powell warned of “some pain” for the economy late last month, there’s still widespread doubt about his willingness to countenance pervasive economic malaise in the name of vanquishing inflation.

The unemployment forecasts were indeed marked higher, to 3.8%, 4.4% and 4.4% for this year, 2023 and 2024, respectively. The new 2025 projection was 4.3%. Although the estimate for next year was materially higher compared to June’s SEP, it likely won’t be enough to placate critics, many of whom suggest the jobless rate “needs” to rise to at least 5%, if not much higher, for the Fed to have any hope of returning inflation to target expeditiously. It was notable that the 2025 estimate suggested officials don’t see unemployment returning to record low levels anytime soon, if ever. The longer run estimate was unchanged, at 4%.

The growth outlook was downgraded sharply. Officials see a much more tepid expansion in 2023, and subpar growth in 2024. Powell has repeatedly emphasized the likely necessity of engineering below-trend growth in the inflation fight. This year’s projection was slashed to just 0.2% on Q4/Q4 basis.

Frankly, I doubt it’s worth taking the GDP forecasts seriously outside of the signaling effect. As Powell himself will readily attest, albeit in more diplomatic terms, forecasting growth outcomes years in advance when macro volatility is high and geopolitical tensions even higher, is an exercise in futility. Suffice to say that, like the unemployment forecasts, the new growth estimates don’t reflect the sort of hard landing many insist will ultimately play out, even as the cuts were indeed meaningful as far as optimistic Fed forecasts go.

“Recent indicators point to modest growth in spending and production,” the statement said, of the economy. “Job gains have been robust in recent months, and the unemployment rate has remained low.”

The Fed likely intended to deliver a “hawkish 75.” I’d say the jury is out and will remain so until the event risk from the Bank of Japan and the Bank of England clear. Given intense speculation around the prospects for a full-point move, threading the needle required a more aggressive median 2023 dot, much higher unemployment projections and, perhaps, some indication that officials believe long run neutral has undergone a epochal shift. The Fed checked the first two boxes, but perhaps not emphatically enough to clear the bar. One thing we know is that 75bps is a lock for November, and 50 for December.

In his post-meeting press conference, Powell was direct, if regretful. “It’d be nice if there were a way to just wish [inflation] away,” he said. “But there isn’t.”

{kind=link}

My 28 year old granddaughter just called the house and my wife answered the phone. She hands the phone to me, saying our granddaughter had a dream about me dying last night. So I tell her no, I’m not dead, and then I asked her why did she think I was dead, and she said she was drinking last night and passed out, woke up feeling terrible, and that’s probably the reason she had the dream. I told her she can’t drink all night and not expect a hangover. Similar to what years of unnecessarily loose fiscal policy will do to an economy.

As to inflation I have seen published industry estimates of heating and energy costs doubling this winter from nat gas prices. On the other hand, my gas bill is flat, the same for my electric bill.

H-Man, this economy is like braking a runaway train, from the time you apply the brakes until you stop, you can travel several miles.