Telling the same yen story over and over again is admittedly a bit tedious, but it really is paramount.

The Bank of Japan meets later this week, and, as I put it a few days ago, Haruhiko Kuroda is playing with fire at this point. Yield-curve control in Japan has (arguably) reached its sell-by date, although not for any of the reasons critics suggested it might over the years.

The relentless rise in US yields is a migraine headache for Kuroda’s YCC regime. The cap on 10-year JGB yields means that whenever yields reach the upper limit of the tolerance band, and US yields are rising, the rate differential moves against the yen (i.e., in favor of dollar strength). Crucially, the very act of defending the yield cap is also bearish for the yen. Bond-buying is easing after all.

This wouldn’t be particularly vexing under “normal” circumstances. Normally, US yields wouldn’t be predisposed to rising inexorably, the Fed would be keen to avert ever higher real rates instead of encouraging them and the cost of energy and food wouldn’t be such that the combination of a weaker yen and spiraling prices threatens to turn Japan into a current account deficit country. But these aren’t normal circumstances. Or maybe they are if we jettison the view that recent history is the only history, but that’s a separate discussion.

On Tuesday, data for August showed Japan’s key CPI measure (so, prices excluding fresh food) rose 2.8% YoY last month. That seems tame in a world where advanced economy inflation prints resemble emerging market outcomes, but outside of the tax-hike impact eight years ago, it was the hottest print in more than three decades (figure below).

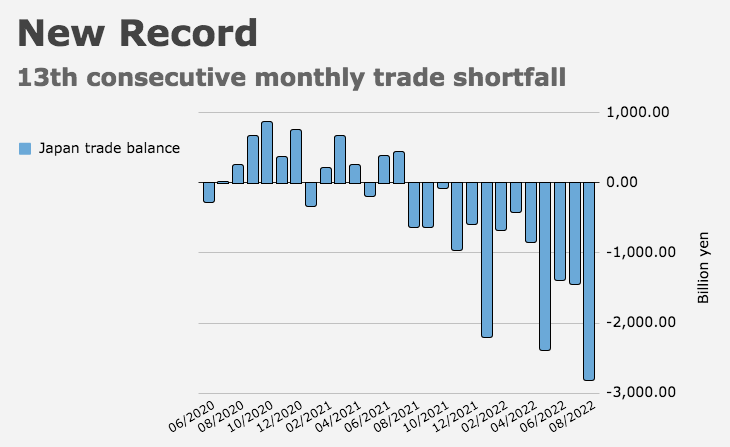

Inflation is now almost a full percentage point above target. This is, in no small part, the product of imported inflation from the yen, which is loitering near a quarter-century low on pace for its worst year on record.

I’m compelled to suggest that this is a case of one man’s legacy taking precedence over the interests of an entire country. Many Japan watchers (and Kuroda himself) would dispute that vociferously. Their argument would revolve around the idea that this inflation isn’t “real” inflation, or if it is, it’s not the virtuous sort that Kuroda is religiously committed to fostering.

But, the story goes, this “bad” inflation could eventually turn into “good” inflation in true “when life gives you lemons” fashion if it’s allowed to simmer. The Wikipedia page for that (hopelessly tired) proverb describes it as an exhortation to “optimism and a positive can-do attitude in the face of adversity or misfortune.” In 2015, Kuroda famously channeled Peter Pan to describe his approach to battling disinflation, using almost the exact same language. “‘The moment you doubt whether you can fly, you cease forever to be able to do it,” he said, before insisting that what central banks need is “a positive attitude and conviction.”

With time running out on his term, Kuroda apparently sees Japan’s burgeoning currency crisis as an opportunity to achieve what’s eluded him for a decade: Inflation. He seems fully prepared to sacrifice Japan’s macro fundamentals at the altar of what’s proven to be a wholly quixotic endeavor, and appears largely unconcerned with what, by now, looks like the most laughably egregious manifestation of moral hazard in the history of central banking.

Great men in positions of power have a tendency to become singularly and dangerously obsessed with their own legacies as the sun sets. That, I’d argue, is what’s happening in the land of the rising sun.

As one economist put it Tuesday, “the current cost-push inflation is bad for consumers, but… the central bank’s policy won’t change until Kuroda’s term ends as this is the last, big opportunity for Kuroda.”

The tragic irony, of course, is that if Kuroda’s last stand goes wrong (and that could mean any number of things at this juncture), history won’t remember him fondly.

{kind=link}

Something else is at work here as well. In Japan there has a long-held aversion to allowing foreign speculators dictate economic policy. Some of your readers may recall how many hedge funds lost their shirts relentlessly shorting JGBs in the 1990s and 00s.

The BOJ enviously eyes Singapore’s ability to ruthlessly see off foreign specs. (Speaking from experience on that one!) Many Japanese policymakers would love to return to a more managed and stable FX regime like that. I don’t blame them.

Yeah, but at this point (and if you watch Kuroda speak) the whole thing has a distinctive “going down with the ship” sort of vibe to it, which I think is unnerving.