For the longest time, the case for a “soft landing” in the US revolved around the notion that household balance sheets were generally strong and that “excess” savings (a legacy of the pandemic) would serve as a buffer against a severe contraction in consumer spending.

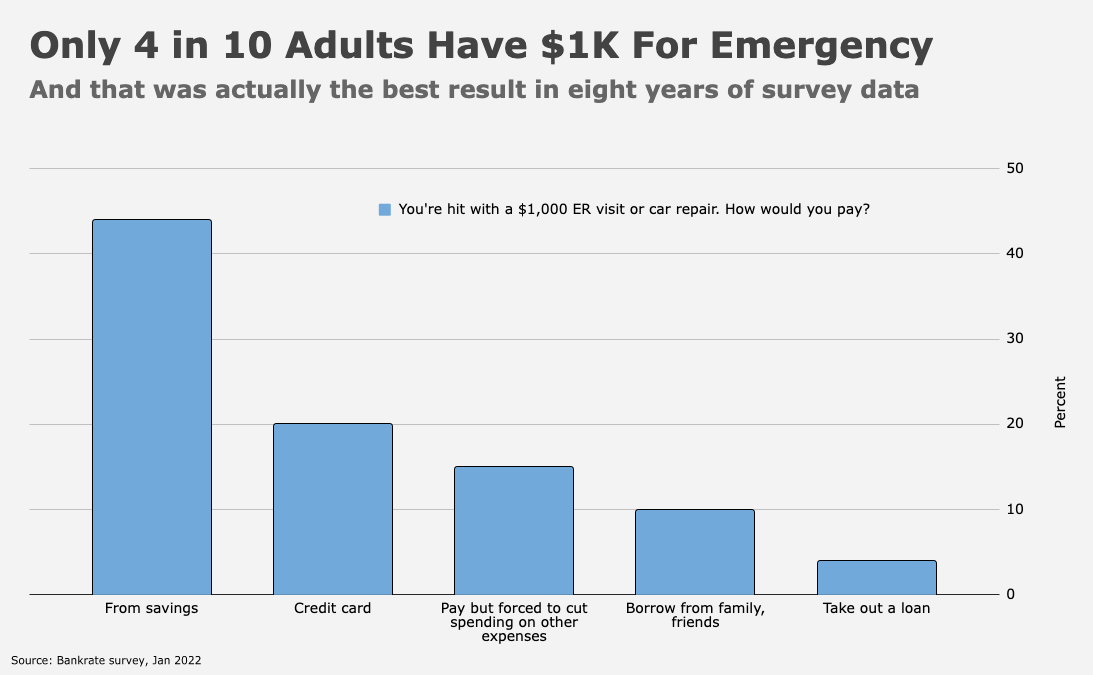

I’ve explored virtually every side of that debate in these “hallowed” pages at one time or another. Part of me harbors serious doubts about the notion that the same Americans who, famously, can’t cover an expensive emergency without borrowing, are also flush with “extra” cash. Another part of me has a difficult time arguing with aggregates, some of which plainly suggest cash balances are indeed swollen, from money market funds to bank deposits.

My efforts to reconcile conflicting data typically entail suggesting that most of the “excess” cash is concentrated in the accounts of the wealthy (figure below). But even there, I often come across figures which appear to show lower-income households are actually better off on some metrics than they were prior to the pandemic.

It’s not particularly helpful if most of the extra cash is piling up in the accounts of the rich. The richer the household, the lower the marginal propensity to consume, and therefore the less “useful” the cash buffers are for sustaining the recovery. Everyone can recite that narrative by now.

Ultimately, I doubt there are any “right” or “wrong” answers to the questions posed and implied above. What I’m quite sure of, though, is that the rich are still rich and the poor still poor.

Setting aside the inequality debate and accepting as true the idea that somebody, somewhere, has extra cash, those buffers are starting to look like an albatross for the Fed and, ultimately, for the US economy. There’s a paradox around every corner in 2022, and quite a few of them relate back to the concept of demand construction, the flip side of the demand destruction orthodox economics tells us is the cure for generationally high inflation.

I’m reluctant (really I am) to keep referring back to Zoltan Pozsar’s missives penned over the first eight months of the year, but quite a bit of what he said across a dozen or so “dispatches” was borne out, although no one will remember in the event “Bretton Woods 3.0” crashes and burns, as I think it probably will.

In May, Pozsar warned that “strong balance sheets are a ‘cyclical bad,’ not a ‘cyclical good.'” That was diametrically opposed to the boilerplate narrative that prevailed at the time, but it made sense. “It means more discipline from the Fed. More hikes and more volatility injected by the Fed — by design — until financial conditions tighten more and demand slows enough,” he went on to write, in the same note. “Consider the idea that strong private balance sheets raise the risk of a recession, for they may force the Fed’s hand to shock risk assets more to make sure we get a recession, or at least a very hard landing, so that the Fed can slow down inflation enough.” Again: “Strong private balance sheets raise the risk of a recession.”

Although the core aggregates in August’s retail sales report were weak, it’s likely that savings buffers are still bolstering consumption, thereby forestalling demand destruction and quite possibly propping up core inflation. When taken in conjunction with the dramatic drop in gas prices from this year’s highs, it seems entirely reasonable to suggest that two things we typically think about as unequivocally positive for the economy (healthy household finances and lower gas prices), are in fact bad to the extent they make the Fed’s job harder.

A popular version of the soft landing narrative suggests that a resilient consumer and a strong labor market will allow the Fed to “do its work” without tipping the economy into recession. But what exactly does that mean? If it means consumers will keep consuming thanks to legacy savings and robust wage gains, then the Fed’s “work” could be for naught.

These concerns are creeping into top-tier research. “The threat of surging headline inflation is fading, but the threat from still-too-high underlying inflation has intensified,” JPMorgan said Monday. Although the bank’s base case is that rate hikes and improvements in supply chains will ultimately work to cool the labor market and help with core inflation, thereby allowing central banks to pause during the first half of next year, they see scant flexibility for overt policy easing “absent a slide into recession.”

“The greater risk now is that a recession will eventually be needed to bring inflation back in line with objectives,” the bank said, noting that “the sharp decline in gasoline prices and rising dollar are boosting household purchasing power [and when] combined with robust labor income growth and strong balance sheets, support for household spending [is] considerable.”

To be sure, JPMorgan didn’t say that strong balance sheets, wage growth and lower gas prices raise the risk of recession. But connecting the dots to get to Pozsar doesn’t require a leap of logic. You could easily suggest that the very same conditions which we’re all inclined to cite as conducive to a soft landing (i.e., a strong labor market, healthy household balance sheets, excess savings, lower gas prices and a strong dollar) in fact make a hard landing more likely by compelling the Fed to telegraph an ever higher terminal rate and commit to holding terminal for twice, three times or even four times as long as they have during historical tightening campaigns. The longer they hold terminal when policy is restrictive, the higher the odds of recession.

{kind=link}

This has all been making me dizzy. Marco or Harnett, soft or hard, and toss in the gamma rallies and 200 point 5 minute red candles, I can say my confidence is damaged.

Taxes would be an obvious solution… and, contrary to rate hikes, they can be targeted. But, alas, everyone hates taxes so much, woe to the politician who try to raise them…

Don’t forget the surge in consumer credit. So far in 2022, we have seen four of the five largest monthly increases. Furthermore, that doesn’t include BNPL. This factoid may just be anecdotal, but i don’t think I have purchased anything online this year without being offered a payment plan. And now even my credit cards (Amex and Chase) are both offering “plan it” options. I remain of the view that even the aggregate data will soon show the consumer hitting a brick wall. I also think unemployment will jump but that is less clear.

CL – Great point.

Yes, in fact, I believe PayPal gives you the option to pay in installments for a Heisenberg Report custom t-shirt in the shop. So, no need to buy it all at once! We’ll ship you the collar first, then the sleeves, and so on, until you have the entire shirt by next summer.

Hopefully, this type of payment structure/delivery of goods doesn’t start applying to mortgages. Otherwise, me and the family will have to make some tough decisions as to which parts of our house we’ll want to cram into until the bank ships the rest of it over the next 30 years.