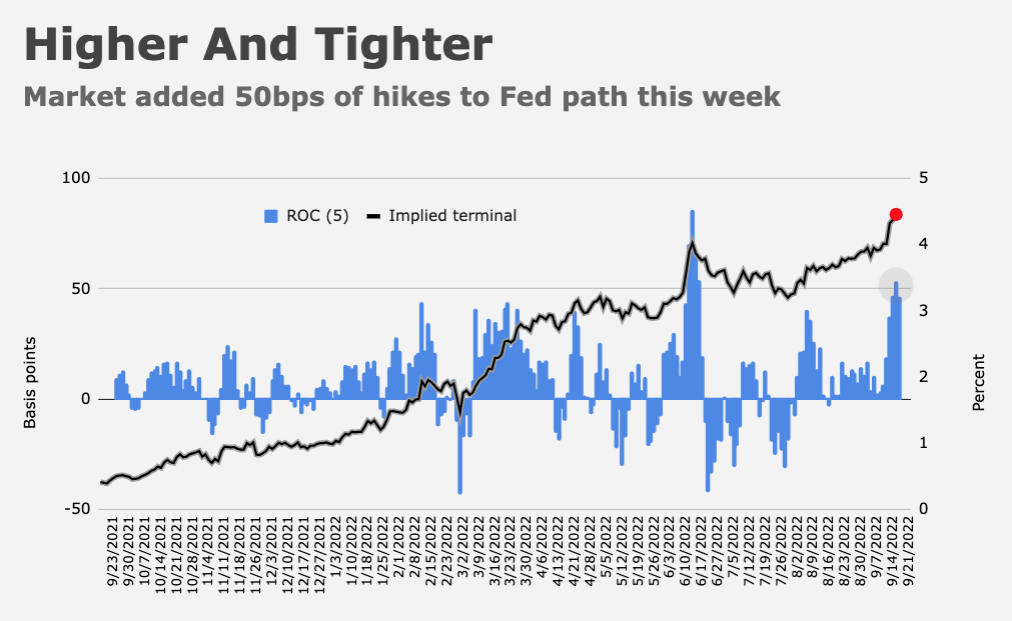

The run up in terminal rate pricing and accompanying increase in US real yields are a drag on risk assets, but a trio of mitigating factors may limit downside for equities despite the twin albatrosses.

That’s according to JPMorgan, whose cross-asset team came across as generally constructive in a Monday note, certainly compared to Wall Street’s bearish contingent.

Earnings risk is front and center, and FedEx’s bleak macro warning didn’t go over well with nervous investors last week. With the caveat that corporates are everywhere and always predisposed to blaming macro conditions for poor execution, FedEx was unequivocal in suggesting that the odds of a global recession are elevated. “We are a reflection of everybody else’s business,” CEO Raj Subramaniam reminded the market, during an interview with CNBC. Bears feasted on FedEx’s pre-announcement. The company also pulled its full-year outlook.

After initially embracing the bull case in the weeks following the original pandemic lockdowns, some top-down strategists, including Morgan Stanley’s Mike Wilson, turned cautious this year on the notion that stocks are the best inflation hedge.

For JPMorgan, many of the basic tenets still hold. “High inflation and robust nominal GDP growth are cushioning nominal earnings growth in an environment of low real growth,” analysts including Marko Kolanovic said Monday. “Better than expected earnings growth is reminding investors that equities represent a real asset class that offers protection against inflation and is thus more attractive than nominal assets like the vast majority of fixed income.”

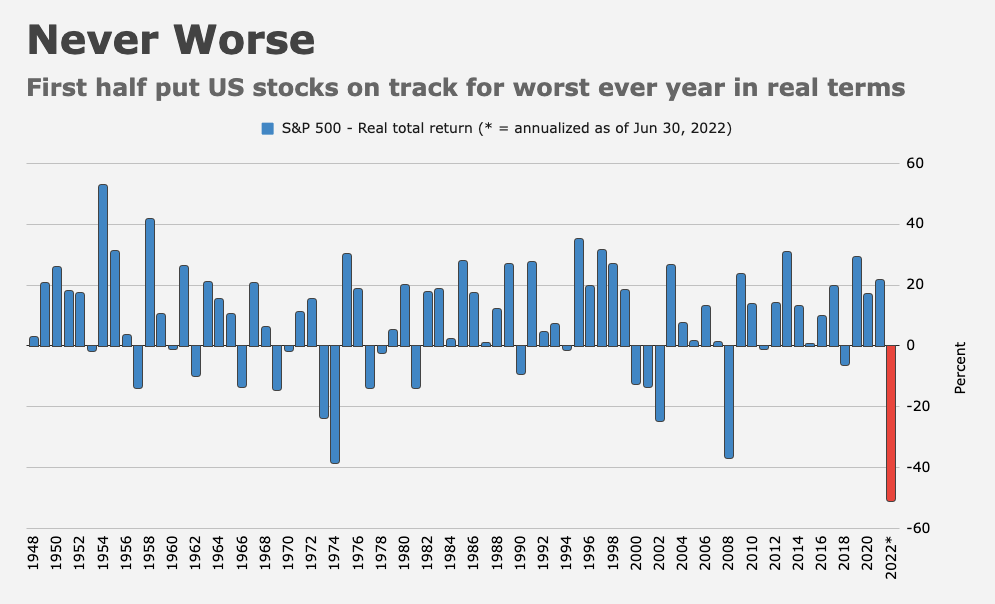

I’d be remiss not to note that between 2022’s bear market and near double-digit annual CPI inflation, real returns for equities were among the worst in history during the first half of the year. To be fair, the bar for solid real returns is very high, especially considering that periods of elevated macro volatility are likely to be accompanied by depressed sentiment, which can exacerbate losses for risk assets. On the other hand, it’s important to avoid begging the question — either stocks are an inflation hedge or they aren’t. Citing elevated price growth while explaining away poor real returns for an asset class that’s supposed to be an inflation hedge is a bit tedious.

In any case, JPMorgan said that even excluding energy, “the decline in earnings has been rather small so far.” The bank conceded that ex-energy declines “could become more significant” in the event the Fed does end up tightening the economy into a deep recession or, relatedly, if the unemployment rate “starts moving up materially.” But there’s a counterbalance. “Even in this adverse scenario we believe that the Fed would be cutting rates by more than is currently priced in for 2023, thus backstopping equity markets and inducing higher P/E multiples,” the bank wrote.

As a reminder: The more hawkish the Fed gets, the more inclined markets are to price in rate cuts on the perception that “hard landing” odds are rising with each hawkish escalation. That presents a bit of a paradox for policymakers: The harder they push the “restrictive for longer” narrative, the more convinced the market is of a bad outcome, and thereby the higher the odds of a dovish pivot.

As for earnings revisions (the key to many bearish outlooks), JPMorgan said they’ve “been tracking the pattern seen in previous recessions [but] there are signs of bottoming out, which suggests that large earnings declines would likely be avoided.” The figure (below) is an illustration.

As regular readers are aware, I harbor reservations about the outlook for corporate profits. Dour warnings weren’t borne out during Q2 results, but there’s a lot to contend with on the macro front, from the prospect of episodic input cost volatility tied to geopolitical frictions, to elevated labor costs. This is a very challenging operating environment. I don’t think that’s debatable, and consensus still expects S&P 500 margins to hit a record next year. Skeptical as I am, I’ll also be the first to admit that betting against corporate America’s determination to protect the bottom line is usually a fool’s errand. Usually.

In any event, for JPMorgan, earnings are actually a mitigating factor, not an impediment for risk assets. The second mitigating factor is positioning, which is unequivocally subdued for “professional” investors. When it comes to “mom and pop,” I’m a proponent of the “retail hasn’t capitulated yet” narrative. I recapped it on Monday morning, in fact. But if we’re all being totally honest, it’s very difficult to say, definitively, how retail investors are feeling or how they’re positioned. “Retail investors” can mean pretty much anything, and there are any number of metrics you can cite to tell any story you want to tell. What’s more clear is that institutional investors are out. Everyone agrees on that. “This is not only indicated by equity futures positions proxies… but also by persistently low demand for hedging,” JPMorgan said Monday. “In our opinion, the low demand for hedging is another manifestation of how low equity positioning is.”

As we saw over the summer, when positioning is low and the tide turns in favor of the bulls, the snapback can be dramatic, especially when systematic flows play along. At the same time, the allure of 3% on USD cash and cash-like instruments could continue to bleed equity demand, both on the institutional and retail side.

The third, and final, mitigating factor for JPMorgan is the decline in both market-based and consumer inflation expectations. The preliminary read on expectations for September in the University of Michigan’s survey was relatively benign, and breakevens have come way down (which, by the way, is mechanically driving reals up, to the detriment of stocks). The figures (below) illustrate the point.

“The stabilization in longer-term inflation expectations reduces fears of de-anchoring, thus making a dovish Fed pivot easier in the future in a scenario where labor market indicators weaken enough to confirm a US recession,” JPMorgan went on to write.

When you think about JPMorgan’s relatively bullish view, I’d encourage you to consider that bearish takes almost always sound “smart.” I’ve discussed this dozens of times over the years. When you spread fear in markets, it’s often taken by investors as a sign of deep knowledge, while anyone who’s calm is described as a Pollyanna. The problem with that is very straightforward: Stocks tend to go up over time, and while I’m the first to argue that the sample size is too small relative to the long arc of human history, we have to consult the data we have, and it plainly suggests that if your holding period is sufficiently long, the odds of stocks being higher down the road are good.

With that in mind, JPMorgan “remain[s] cautiously optimistic.” “We combine a sizable equity overweight in our model portfolio with a credit underweight as a hedge,” the bank said. They’re bearish bonds with a bias towards flatteners, remain “long the dollar as a hedge to a hawkish Fed” and still see “significant upside” for raw materials.

{kind=link}

{kind=link}