I left the car running. I always do.

It’s still scorching hot around here, and I don’t like to sweat. Besides, in-person conversations with me never last very long, especially when the person with whom I’m chatting is a Merrill rep at a local BofA branch. I almost called it a “nearby” BofA branch, but that wouldn’t be accurate. Like Walmart and other places I’m begrudgingly compelled to visit from time to time, the bank trip is a mini-journey. It’s not all the way on the mainland, but it is several islands over from “mine,” which means traversing two bridges.

Admittedly, I relish the bank visits. I schedule them almost solely for my own amusement. They’re so few and far between that I invariably meet a new rep each time, and infallibly, they have trouble coming to terms with the concept that is “me.” I dress like Paulie Walnuts when he’s not at dinner — so, tracksuits. I talk very fast, and only about myself. My recitations of prevailing market realities are encyclopedic and, I’m told, condescending.

I scheduled this particular appointment for a reason, though. Cash is a viable asset class again, and I was interested to see if BofA (or Merrill or whatever) could sell me on any high-yielding cash products. It was a Seth “Daily News” sort of thing. In the normal course of business, I use BofA only for my “regular” banking. I have enough parked in federal money market funds and I admittedly turn my nose up at those high-yield “online savings accounts,” despite having no rational reason to snub them other than the “retail investor” vibe they throw off, which makes my delusions of grandeur uncomfortable.

The truth is, there’s a part of me that likes to have a sizable portion of my cash holdings right down the street, where “right down the street” can be taken entirely literally. Because I’ve rotated into cash this year (for obvious reasons) the portion held in accounts accessible through local bank branches is now too small relative to my total cash allocation. I was hoping BofA could help me remedy that.

“I do understand that given current realities, you’d sooner turn away deposits than court them,” I told the rep, leaning back in the chair, one FILA almost propped up on the desk. “I’ve never talked to anyone who understands that,” she marveled. Given her age, she’d probably never seen a pair of FILAs either. Jokes aside, I sympathized with her incredulity — fast-talking Paulie with his tracksuit is the only local who understands anything about the banking system in 2022, despite everyone in the area code being a semblance of rich.

The results of that “sit down” (there’s a subtle joke there) were inconclusive. I bring it up… well, first and foremost because it’s been a while since I employed one of my signature vignettes, and that one has the added benefit of being funny. But it also serves to underscore the pervasiveness of a dynamic that’s already bleeding institutional demand for equities and may soon impact retail investor demand for stocks too.

“In addition to the larger macro theme of equities currently being punished under the global central bank regime of ‘tight FCIs until demand-side inflation is killed,’ a topic that’s part of almost every conversation we’re currently having with clients is ‘Who wants to hold volatile risk assets when you can hold cash?'” Nomura’s Charlie McElligott wrote Monday.

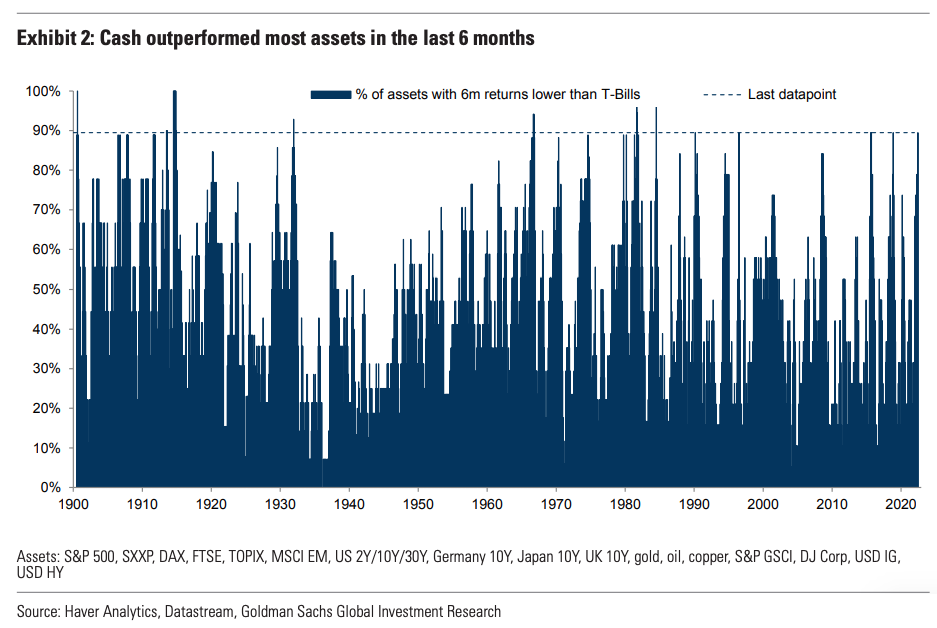

“Global central banks are telling you that we have months of ‘financial conditions tightening shocks’ left until we see terminal rates at a level where the demand side of inflation is broken,” he remarked, suggesting that’s a daunting prospect for those eying their near- to medium-term asset allocation “versus, say, owning and rolling 3-month US T-Bills yielding 3.10% in ‘risk-free heaven,'” especially considering the favorable spread to dividends (figure below).

The notion that “TINA” is dead has come up again and again in 2022, a year during which Bills have outperformed at least 90% of global assets. Such conjunctures are exceedingly rare, occurring only a relative handful of times over the past 120 years. 2018 was one such instance, by the way.

“This idea that there now is actual competition for equities as the de facto ‘bulk weighting’ for US investors is going to be critical as we move forward, particularly when thinking about ‘Who is the incremental seller of equities from here?’ especially if there’s going to be another leg down, as the Fed is forced to ‘crash-land’ the plane,” McElligott went on to write.

The buy-side is bombed out on the equities side. The September vintage of BofA’s Global Fund Manager survey showed cash levels at post-9/11 highs and record Underweights in stocks (figures below).

As I wrote last week, fund managers can hardly be blamed. Again: It’s not just that there are worse places to park your money in 2022 than cash, it’s that there are virtually no better places.

You can also use the rolling beta feature on the terminal with the HFR/HFRX indexes to get a read on sentiment and positioning. The figure (below, from Nomura) suggests the Long-Short crowd’s beta to US equities sits in just the 2%ile looking back almost two decades.

It’s a similar (if far less pronounced) picture if you look out across macro funds, mutual funds, vol control, CTAs and risk parity.

But, as everyone who follows the weekly EPFR flows data is acutely aware, retail investors haven’t capitulated. That’s an ongoing theme. Although flows into global equity funds turned negative in H2, very little of the massive haul from 2021 has come out.

In fact, 2022 is itself still shaping up to be a good year for inflows. The figure (below) was current as of September 1. It’s meant for context. Those interested in precision will note that as of September 14, a net $17 billion had come out of stock funds in H2 so far, compared to a $190 billion inflow during the first half.

The implication is that the incremental seller of equities going forward might be retail investors. Especially as cash becomes more and more attractive. If stocks keep selling off and cash is yielding 3% (or better), cash is pretty compelling. Just ask the guy in the tracksuit with his feet on the desk in the corner office at your local BofA branch.

“When looking at EPFR fund flows, you can see that ‘Ma and Pa’ investors have never capitulated out of US equities, which is not crazy when considering that since the start of 2020 (pre-COVID 12/31/19 to present returns), the S&P 500 remains +19.9% and ‘high flyer’ Nasdaq +35.8%,” McElligott wrote.

He continued, driving home the point: “A ‘next leg’ shock-down in equities in the coming months would probably require the ‘401(k) investor class’ to see years’ worth of positive equities performance wiped out first, which, in conjunction with the ‘return of cash’ as a viable asset class, would drive a larger asset allocation regime shift out of equities and back towards fixed-Income now yielding at levels which allow it to act as AAA — ‘An Actual Alternative’ to equities, but at a much lower vol.”

{kind=link}

With unemployment still low (so nobody is emergency-selling) and everyone having been told to just buy and hold for years, is it likely retail investors (like me!) will start selling, though? Presumably you’d need unemployment to tick up to provide the impetus. I mean, I read you pretty regularly, and I haven’t really touched my meager holdings in the last couple years. Although i’ve also been in a bit of a bubble with school and cheap debt fueling me along (thanks for the $20k, Joe!).

Speaking of which, here’s hoping the impending hard landing holds off until I’m barred and employable. Someday I’d like to be able to throw my dirty shoes on a bankers desk and not be nightsticked by the security guard!

Oh, they’re not dirty.

I certainly get your point. It makes sense. Cash is king, and T-bills are a thing now. But in my philosophy, one never knows when a dispassionate and influential force or person similar in certain ways to Paulie Walnuts himself would get the better of me and silence my voice and will to action.

Of course, I don’t take unnecessary risks and do not want to make regrettable investments. After all, we may yet see the SPX at 3400, or even lower when the recession hits us harder. I believe it’s a real possibility. I am assuming that it will actually happen. But on the other hand, I’m not getting any younger and I can’t take it with me. I happen to like investing in good stocks when they don’t cost a lot.

If I was not such a crochety old smart aleck, compelled by the life-force to carry on with my own brand of business, I’d probably feel less audacious. I’m thankful for the experience of painful losses that I suffered in past recessions and I’m glad to see better investment results as I age. But that doesn’t mean I’m wise. I sincerely hope readers that have not previously experienced a long and deep recession will take note, but not imitate my approach, which is not unlike that of a loser. Loss is in the nature of the market. It just is. Take care.

They still make FILA shoes?

I basically live on a metaphysical island.

I am somewhat amused when people cite their 2022 YTD investment returns on various investment blogs (although, most assuredly better than mine), as it seems kind of like assessing hurricane damage during the eye of the storm.

I have learned the hard way- and more than once! – that one good call at market timing is pretty much worthless because knowing when to go to cash is worth something only if you know when to get back in and you don’t hesitate. There is also “going to cash” as in anything where I don’t have to pay taxes to do that vs “GOING TO CASH” as in I will pay tax and reset my basis….

Buy and hold has worked very well for me over the long term- so long as I am willing to “time” my large expenditures- which I am.

I have, however, been buying Treasuries for my (almost) 90 year old parents, as their CD’s mature. We are even considering paying the early termination fee to get out of some CDs that were paying less than 1%, which means they will be tripling or quadrupling their interest income in 2022 vs. 2021. Inflation has had minimal impact on their lives because they still live in the same house they have lived in for 57 years and require minimal help- other than their lawn care/house repairs. I usually wash a few windows every time I visit because they would never pay retail for that service, but they can no longer do that themselves.

And I can’t help myself- classico or comfort trainers?

Aren’t more deposits just free NII for BofA? I feel like I’m missing something.

You can Google it and read about it. I mean, it’s more of a conversation starter than it is an actual logistical constraint for individual depositors. For corporates, it’s a real discussion, though.

Google was not as edifying as I would have hoped. More specifically, there were some very relevant answers from summer ’21 that no longer obtain. Seriously, choose your keywords, you get a raft of info, all from spring-summer 2021, with the odd 2020 mention thrown in.

Awash with deposits then, with no way to generate enough loans to put that money to work, banks were left facing a pile of cash balanced against a risk-free rate of ~0%. Bad for all kinds of ratios and capital structure reasons, but also just a giant pile of overhead with no yield.

The risk-free rate is no longer 0%. Now they can just flip it into bills and count the interest income. While this ain’t exactly 3-6-3 banking, it’s still 0.05-2.5-3 banking, so I’m still unclear on why banks wouldn’t want deposits. (I tried to DYOR, I really did. I’m not the type who expects others to do basic search on my behalf). Is it a capital structure thing? Something stress-test adjacent? Some kind of negative convexity thing if the FED starts slashing rates a year from now?

On the corporate side, I can see that it was a screaming issue in ’20-’21. That makes sense given both the size and the need to deal with astute CFOs. I can’t begin to imagine the constipation this caused European banks in the initial days (and years) of negative rates. But does any of that still apply?

Aren’t track suits hot? I don’t mean fashionably “hot”. I mean thermally hot.

Sounds like you live in the Florida Keys.

I’d think shorts and flip flops would be more apropos.

Have you never worn a track suit? They are the pinnacle of breathable comfort. It’s like wearing loose-fitting polyester boxer shorts over your entire body.

H – do you ever give the ML rep the link to these pages? She might benefit ( or at least be entertained).

So, what investment did you eventually park your cash in? I am looking for something I can get in and out of quickly, but could only get 1.9% through money markets. I would love 3.1% right now with the ability to quickly get into new positions without any cash-out fees. Any 3 month treasury ETFs or similar products that look good?

Just park in in Gerbils. 0-12 month rolling t-bills, GBIL.

You should be able to buy 3 month treasuries paying ~3.5% at Fidelity or Vanguard or some investment broker.