Earlier this week, US junk bond yields hit all-time lows amid the rampant euphoria that accompanied Pfizer’s coronavirus vaccine news.

It was a remarkable achievement: The lowest borrowing costs on record for high yield issuers came during a year that featured a pandemic and the worst economic downturn since the Great Depression.

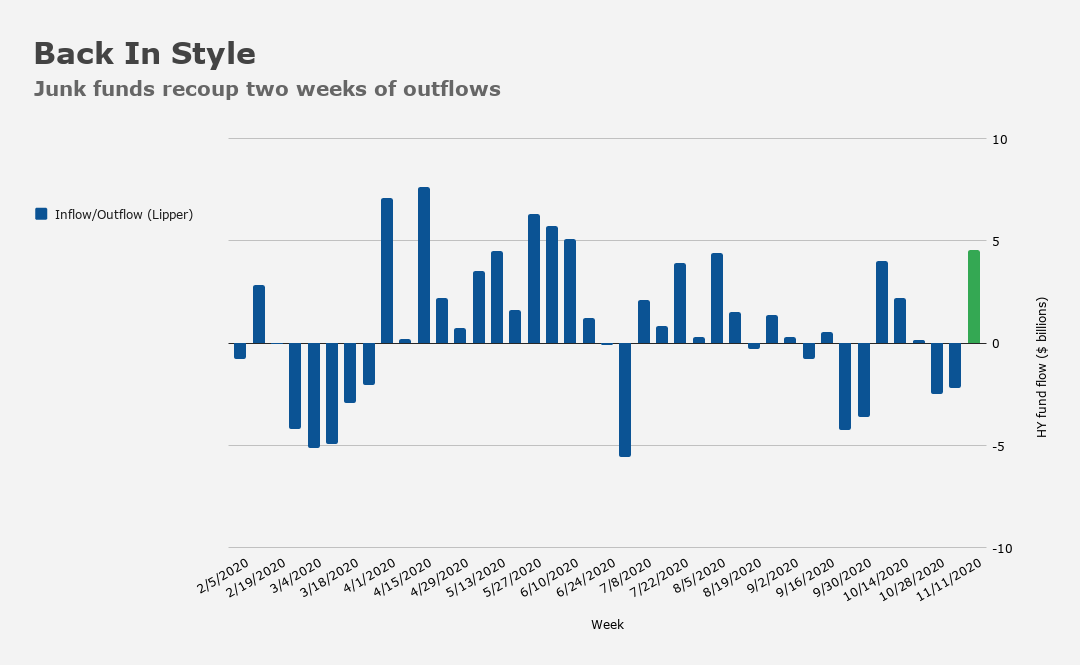

While documenting the milestone, I noted that the timing was fortuitous. Junk outflows accelerated prior to the election, and Lipper’s data showed high yield funds lost another $2.2 billion in the week through November 4.

Read more: Meanwhile, More Milestones In Junk

Given the post-election risk-on mood and the pro-cyclical rotation that played out across Monday and Tuesday, it probably won’t surprise you to learn that those outflows reversed in the week through Wednesday.

Indeed, US junk funds swung to a $4.56 billion inflow during the period, effectively negating the exodus from the prior two weeks. It was the seventh largest flow ever into junk on Lipper’s data.

EPFR data, meanwhile, shows a decidedly risk-on lean. Global equities saw their largest weekly inflow ever, while US equities raked in $32.5 billion, the second most on record. Emerging market stocks enjoyed their fifth best week of inflows, while energy shares took in $1.5 billion, the most since April of 2015.

Note also that investment grade funds returned to inflows in the week to November 11, after suffering the first outflow since April in the prior week.

Junk yields are now off the record lows hit Monday. Thursday’s risk-off session found yields jumping some 25bps, the most in five months.

$9.2 billion in junk deals priced this week. Indeed, a trio of deals managed to get done Thursday despite the less friendly market backdrop, defined by virus worries and a stay-at-home advisory for Chicago.

If you ask Barclays, high yield issuance will be robust in 2021, albeit slower than this year’s blistering pace. “Given that the High Yield Index is 17% larger this year based on amount outstanding and the addition of some frequently issuing fallen angels, we think that supply will remain near the higher end of historical ranges,” the bank said, in the course of projecting supply of between $300 and $320 billion next year.

Through this week, junk borrowers had tapped the market for a record $381 billion in 2020. Investment grade issuance is up to nearly $1.7 trillion.

I’ll just recycle some familiar language in closing. The Fed’s unprecedented backstop for investment grade bonds and controversial decisions to buy fallen angels and high yield ETFs, together served as a Linus-style security blanket.

Jerome Powell was a psychological support pillar of incalculable value to a market staring down a public health crisis that posed an existential threat to entire sectors of the global economy.