If you were impatiently waiting on the next easing nod from the PBoC amid an incessant barrage of monetary accommodation from developed markets, you were placated on Monday.

China slashed the 7-day reverse repo rate by 20bps, a large move to be sure, in what might very well be a sign that Beijing is expecting a prolonged hit from the coronavirus containment measures adopted both domestically and, now, abroad.

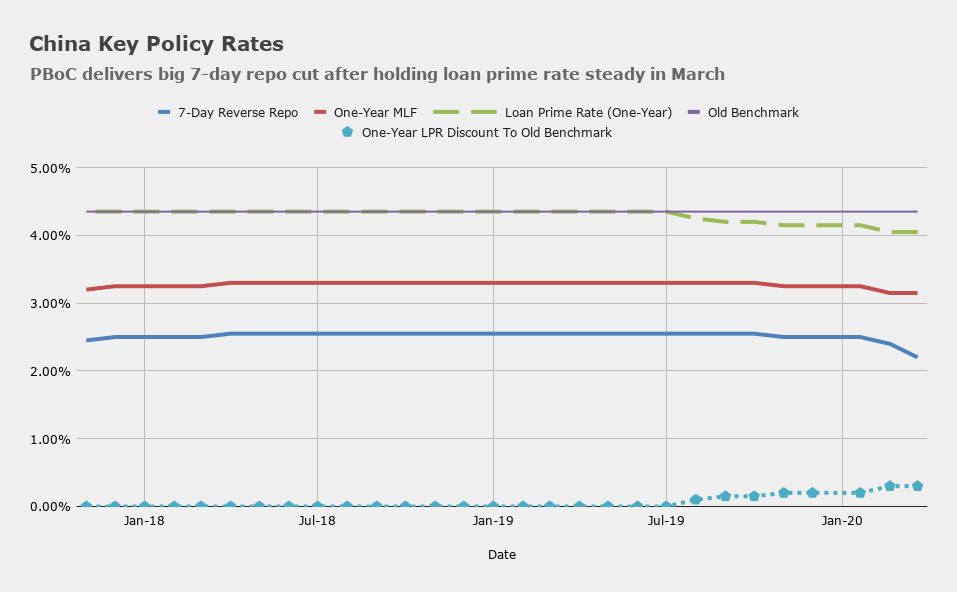

China completed the first round of what’s expected to be multiple waves of post-epidemic monetary easing on February 20, when the PBoC slashed both loan prime rate tenors, with the one-year cut by 10bps to match an identical cut to the medium-term lending rate. LPR was held steady in March, much to the surprise (and chagrin) of some market watchers.

China last cut the 7-day repo rate on February 3, the day mainland markets reopened to a horrific selloff following the Lunar New Year holiday, which was extended in a bid to help contain COVID-19. At the time, the virus was still mainly a “China problem”, so to speak.

That day, China cut both the 7- and 14-day repo rates by 10bps. Monday’s move is twice that size.

This lays the groundwork for an MLF cut which would, in turn, pave the way for a much lower LPR fixing at the end of April.

Recent data has been predictably terrible, with the most recent bad news coming in the form of a laughable 38% plunge in industrial profits. PMI data is due this week, and it should be ghastly, much like February’s prints.

Alongside Monday’s OMO cut, the PBoC injected a net 50 billion yuan.

That’s not very much, but it’s symbolic. The central bank had refrained from adding cash to the system for 29 straight days.

Late last week, news out of a Politburo meeting suggested Beijing will widen the deficit and sell more debt in order to fund stimulus after the outbreak crushed the world’s second-largest economy in the first quarter.

It’s been at least 10 years since China’s official deficit topped 3% of GDP. Some have urged the leadership to abandon that tacit red line amid the dramatic hit to the Chinese economy, which is now seen contracting sharply.

Seems like odd little baby steps? The evidence shows that their SWF de-risking triggered the cascade in US equities and bonds. Are they playing the system or are they getting played?

Jeff Snider freaking out about Libor

.

How huge? The TED spread, that is, the difference between 3-month LIBOR and the 3-month T-bill yield, has blown out to the highest since GFC1 surpassing even 2011. Since TED is a measure of credit risk in the interbank markets, it is telling us something important about Jay Powell as well as those falling fed funds and repo rates.