How is this cycle different? Let me count the ways.

On second thought, let me not. Because “this time is different” are famously dangerous words when arranged exactly in that order. By extension, enumerating the ways in which this time is different could be an especially perilous exercise.

Dry humor aside, there’s a sneaking suspicion even among rally skeptics, pessimists, bears and so on, that sundry “playbooks” won’t necessarily work this time, given any number of distortions associated with the pandemic, inclusive of those brought about by fiscal and monetary measures aimed at rescuing economies from the pestilent abyss.

Given that, it’s hard to know whether to be concerned about apparent anomalies or whether to just write them all off as examples of a world turned upside down. Specifically, charts juxtaposing the trajectory of asset prices, macro variables, recession indicators and so on, with prior cycles, may not be especially useful, or could anyway be deceptive to the extent the comparison is apples to oranges.

That said, it’s probably safe to venture some simple comparisons involving equities, and Morgan Stanley’s Mike Wilson did just that this week while addressing the contention (popular in some bullish corners) that we’re witnessing a “new cyclical upturn,” which is just a fancy way of suggesting stocks were priced for a recession at the lows in October.

Wilson first looked at the trajectory of equal-weighted performance relative to the cap-weighted benchmark to get a sense of how breadth is developing this time versus eight “last times,” if you will.

Market breadth is obviously a hot topic in 2023 amid a blistering rally for the so-called “Magnificent 7” US tech stocks.

“Each of the past eight cycles has seen equal-weight index relative outperformance at this point [but] this cycle, it has lagged,” Wilson wrote. The figure above is rather poignant. You can clearly see the impact of the mega-cap, A.I.-driven rally (the sudden drop in the black line starting five months from the lows).

Next, Wilson looked at ISM manufacturing which, you’re reminded, printed in contraction territory for an eighth straight month in June.

“In prior cycles, the PMI has made upward progress off the lows at this point,” Wilson remarked. “This cycle, it just made new lows.”

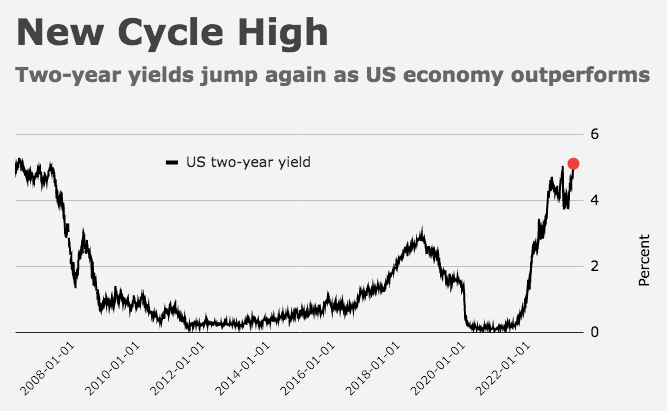

And it’s not just breadth and growth. Wilson looked at front-end rates, which he noted “have historically been flat-to-down at this point post-equity market price lows… as the Fed is typically shifting toward a more accommodative policy stance which supports the recovery.”

Needless to say, that’s not the case currently. Two-year yields hit new cycle highs last week, and Fed officials are adamant that more hikes are coming.

{kind=link}