“Our track record at understanding inflation is really, really bad.”

That rather stark admission, from David Romer, was included in a summary of the American Economic Association’s annual meeting, which wrapped up two days ago. It was the first in-person gathering since the pandemic.

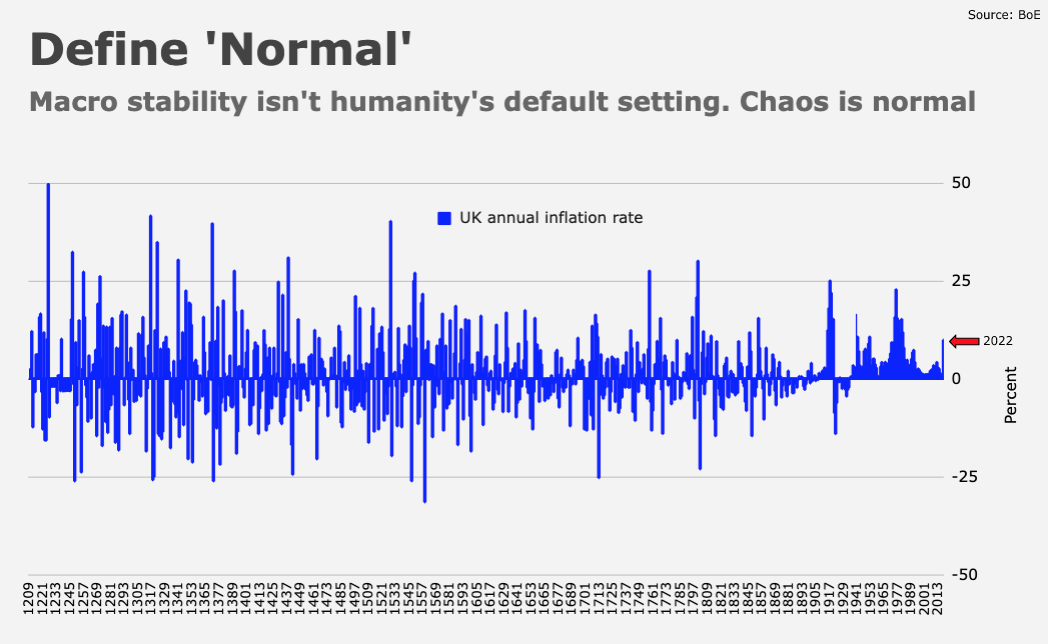

In addition to underscoring my long-standing contention that inflation may look disconcertingly stochastic in the years ahead, Romer’s remarks spoke to another, more controversial, claim I’m fond of — namely that macroeconomic outcomes aren’t amenable to forecasting. Economics isn’t a science.

Somewhat ironically (albeit befitting of a seemingly genuine, at times disarming, modesty), it was Jerome Powell who offered what I still consider to be the most honest concession regarding economists’ failure to see inflation coming. “One way to say it would be that I think we now understand better how little we understand about inflation,” he said, to nervous laughter at the ECB’s yearly conference in Sintra. “That’s not very reassuring,” Bloomberg’s Francine Lacqua half-joked.

It wasn’t so much what Powell said (his concession wasn’t as unequivocal as the quote above from Romer) but the way he said it. I can’t speak for Romer’s sincerity, but there was little doubt that Powell meant it. He was humbled by recent events. If his capacity for humility does exceed that of his colleagues and associates, perhaps it’s attributable to the fact that Powell isn’t an economist.

It’s impossible to overstate how important this discussion is in the context of stimulus unwind. It’s important in all manner of other contexts too, of course, and you could easily argue that the implications for Wall Street are less important than the impact of elevated consumer price growth on Main Street. But, I wanted to offer a companion piece of sorts to “Fear The 4th Quadrant,” published here on Tuesday morning, and that entails looking at this through Wall Street’s lens.

That linked article cited the latest from Deutsche Bank’s Aleksandar Kocic, who juxtaposed the path along which markets travel during traditional recessions and recoveries with that traversed in the post-Lehman years. I encourage readers to peruse that article for the details, but the gist of it is that, as Kocic wrote, “the unwind of the recession trade in conventional settings goes along the grain of the market trade [while] the unwind of QE essentially becomes a de-risking move [going] against the grain of recovery.”

A corollary is that because traditional recoveries are collinear with the unwind of a recession trade, volatility tends to be subdued. Not so when recovery is accompanied by the unwind of the QE trade. “Convexity and its management play an essential role in the process of policy unwind,” Kocic wrote. “The inertia of a financial repression unwind is the withdrawal of convexity supply and a vol-enhancing mode.”

Fortunately, the Fed has become a reasonably adept convexity manager. But that management process depends heavily on the absence of urgency. And, as you might’ve noticed, inflation’s return, and policymakers’ failure to forecast it, made for a very urgent situation. That, in turn, left the Fed with few options.

“The previous tools of convexity supply through Fed gradualism, excess transparency, forward guidance and removal of the fourth wall were all suspended in 2022 in favor of an unconditional war on inflation,” Kocic went on to say.

In the early stages of the pandemic, the Fed jumped into action, with an aggressive effort to tamp down volatility, close bases, provide liquidity and generally restore order. Naturally, that was accompanied by a massive risk rally, and the usual misallocation of capital. It was also accompanied by a virtually unprecedented fiscal impulse, which served to amplify the risk rally and associated bubbles.

“The thing that made the unwind of stimulus different this time was a massive fiscal injection (we recall that in the post-2008 period, fiscal policy was tight),” Kocic wrote. “As a result of combined fiscal and monetary easing, together with COVID-induced disruption of supply channels, inflation returned with unexpected forcefulness [and] this was a perfect storm for volatility.”

They key point is that both the 2015-2018 experience and the current tightening episode were unwinds of the QE/financial repression trade, but during the earlier cycle, the Fed benefited from benign inflation outcomes. No such luck this time around.

Without well-behaved inflation, the convexity management exercise wasn’t feasible. That opened the door to an anomalous rise in rates volatility. I’ve been over this on countless occasions, specifically in the context of the macro regime shift. Regular readers might remember “Normal Is War,” published on September 15. Here’s an excerpt:

Central banks’ increasingly panicked efforts to coax the inflation genie back in the bottle have resulted in violent selloffs in rates and associated volatility. The dominance of rates vol is new. Of course, some of this is by design. The Fed sought to enlist volatility — the “best policeman of risk assets” — in the inflation fight. But rates volatility is perilous. Especially considering the extent to which unbridled fiscal policy and unruly commodities could mean that previously docile bonds, domesticated by decades of structural disinflation and a dozen years of forward guidance, become lawless, and difficult to tame.

Although rising real rates in 2018 did ultimately destabilize stocks (and credit), that episode was a managed affair, even as Powell’s famous faux pas (“long way from neutral” and “auto-pilot”) alongside the US-China trade war and Trump’s border wall shenanigans made the entire episode feel more chaotic than it actually was.

“The main reason [rates] volatility did not ignite [from 2015-2018] was a careful effort of convexity management by the Fed on top of the slow pace of rate hikes,” Kocic said. “Despite the baggage of years of administered markets and misallocation of capital, the unwind was orderly.”

By contrast, 2022 was genuinely harrowing. And it’s no secret why. “None of the tools of convexity management could be deployed in the current cycle, and, in addition, the Fed had to raise rates quickly and aggressively,” Kocic wrote. “Unlike 2015-2018, when there was no urgency to hike, the current cycle is all about urgency dictated by the unprecedented pace of inflation rise.”

Needless to say, 12 months of rate hikes wasn’t enough to correct all the distortions associated with a dozen years of the QE trade. Just ask the UK LDI complex, which nearly imploded in October when gilts suffered a multi-sigma selloff. That means the stakes are high going forward when it comes to inflation. If it doesn’t recede or, perhaps worse, shows itself to be every bit as unpredictable and unruly as it’s been throughout history, central banks will struggle to contain volatility.

During the same remarks cited here at the outset, Romer said that, “The range of plausible [inflation] outcomes over the next year or two is very, very wide.” As Lacqua might put it, “That’s not very reassuring.”

{kind=link}

Thanks for delving into this.

It’s human nature to look and hope for some kind of structure in so many aspects of our lives. That includes economics.

I entered trading markets in 1976 and as the years passed, I’ve come to share many of the conclusions expressed by Chairman Powell and the others you cited. Bravo Powell!

That extends over to the idea of using earnings to value stocks in the aggregate.

The dominant narrative seems to be an orderly disinflation with perhaps a long tail. Nice to have the reminder that just as very few correctly mapped the ascent, we likely won’t get it right on the way down either. China’s reopening is likely the largest wrench thrown in the mix. The Economist thinks China will account for 2/3 of global growth this year. China (usually) consumes 1/5 of the world’s oil, over 1/2 of copper, nickel and zinc, and 3/5 of iron ore. Goldman recently reported that Chinese metal inventories are the lowest in 15 years. These will need to be (rapidly) replaced if economic activity picks up. LNG purchases will pick up too, giving Europe some competition. Despite the forecast global downturn, commodity strength may return. Inflation may have a long tail indeed.

The US currently consumes 20-25% of the earth’s major resources with ~ 4% of the world’s population. China has more than 4 times our population which means our current resource consumption is grossly unsustainable. Even if China were to achieve a standard of living equal to half of that in the US, we will soon be overwhelmed in the market for resources, including food. Much of our food comes from sources off-shore, Chile, Peru, Mexico, and many other places. China gets food from those places also. China is a growing competitor and constantly accusing them of lying about their data will not ameliorate any problems we will have in this inevitably growing competition. Of the top four largest meat producers in the US, JBS, top beef producer, is a Brazilian firm and Smithfield, top pork producer, is now controlled by its Chinese parent co. Context will become an increasingly important factor controlling the management of our economy. As we become a smaller player in terms of our “economic market” share, it will harder to manage our outcomes. Keeping up that leading reserve currency thingy will be a top priority.

A tip of the hat to your writing style on this one. Managing to fit these things together coherently, that’s something. Kocic’s quadrants deserve reflection. Unwinding should be its own field of study.

“Unwinding should be its own field of study.” Brilliant observation! I don’t know who the top teachers will be but right now I see very few, if any, standout candidates for top brain.

The key for me is avoid false reassurance. Whether I see it or not, there is always a high degree of risk, uncertainty and ignorance. You have to have some ground rules, and you have to admit when they aren’t the keys to success. The source of good judgement is experience, and the source of experience is bad judgement….