It’ll be back to something like business as usual in the new week, when traders nursing the remnants of New Year’s hangovers will be greeted by a slate of top-tier data out of the US.

For some of us (e.g., me), the comparatively lively docket will come as a relief. Although this holiday season offered more opportunities to editorialize than most thanks to geopolitical tumult, we nevertheless came dangerously close to “copy for the sake of it” territory by the final trading day of the year.

I exhausted my 2022 retrospectives and year-ahead pontificating weeks ago (see “Addiction Liability And The Roaring Twenties,” “Visualizing Macro History” and “Existential Questions For 2023,” for example), so allow me to bid this year a not-so-fond adieu by way of an updated stock-bond drawdown chart.

More than $36 trillion in value was vaporized across global equities and fixed income. That figure is around $38 trillion if you toss in crypto. It was a year to forget. But, unfortunately, it was a year everyone will remember vividly.

The first week of 2023 will give market participants an outdated snapshot of the US labor market by way of December payrolls and November JOLTS. We may be approaching the point in the cycle when one month makes all the difference, or at least if you subscribe to the Wile E. Coyote description of recession realization. That said, the higher frequency jobless claims data suggests we’re nowhere near cliff’s edge.

Consensus is looking for ~200,000 from the headline NFP print. You’ll recall that November’s jobs report was discouraging for a Fed that desperately wants to cool the labor market. Not only did the headline come in much hotter than forecast, but average hourly earnings rose at double the expected monthly rate, and participation ticked lower. Policymakers want slower (but still respectable) job creation, cooler (but still robust) wage growth and higher (not lower) participation.

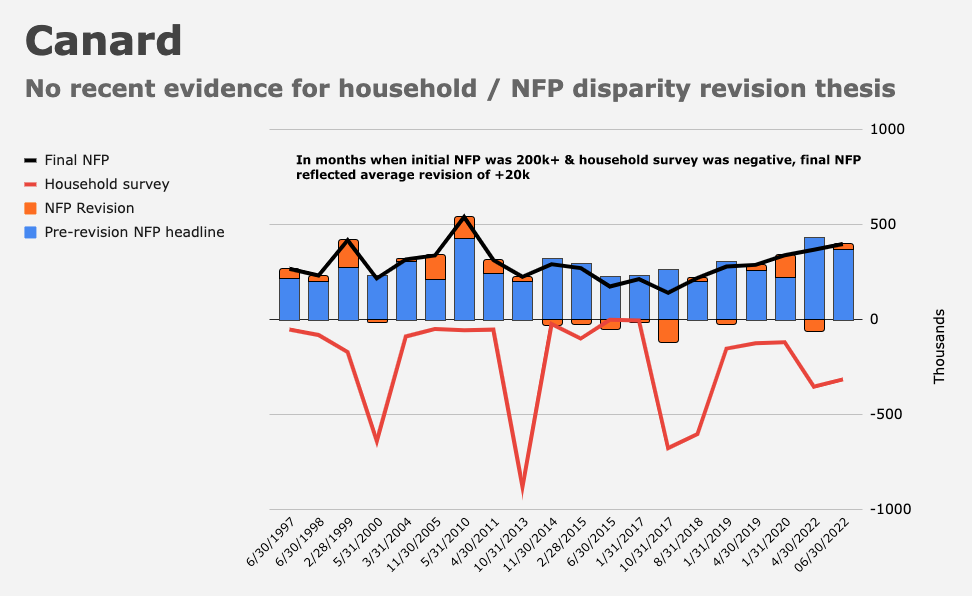

Some have suggested lackluster response rates and negative readings on the household survey are a harbinger of downward revisions. We’ll see. The jury will be out on that for months. As a reminder, history shows no obvious relationship between negative household prints and subsequent revisions to the headline NFP figures.

The trajectory of the labor market is seen as the key to inflation moderation in 2023, and as such, developments on the jobs front will be parsed obsessively for clues as to the likely course of Fed policy.

Jerome Powell is still convinced that the extraordinarily elevated number of job openings across the economy leaves the door open to a soft landing. This refrain isn’t just familiar, it’s ad nauseam. If slower demand renders scores of job openings superfluous, the labor market can rebalance and wage growth can cool without too many Americans actually losing a job.

Many economists doubt that narrative. That’s the context for JOLTS data due Wednesday. It’ll reflect job openings on the last business day of November.

Although there are very convincing arguments for the contention that matching efficiency is irreparably impaired, it’s difficult to imagine a scenario in which at least some of the millions upon millions of excess job openings that currently exist across the economy don’t disappear in 2023. Take that pseudo-prediction for whatever it’s worth.

ISM manufacturing for December will be released concurrently with the JOLTS figures. A few hours after that, minutes from the December FOMC meeting will give traders an opportunity to exercise their tasseography skills. ISM services is on deck Friday, shortly after the NFP release.

The market remains wholly unconvinced that the Fed will manage to hold terminal once the funds rate peaks, presumably in the second quarter. In fact, traders aren’t even sure Powell will manage to get rates above 5%. Some of the tension between, on one hand, market pricing, and, on the other, the Fed dots and policymaker rhetoric, should be at least partially resolved within 45 days. If the labor market doesn’t bend, let alone break, and the earnings “reckoning” top-down strategists have been calling for since Q2 (in stark contrast to the relatively rosy forecasts of company analysts) doesn’t pan out in Q4 results, then the burden of proof for expecting rates to peak below 5% will fall to those placing dovish bets.

Of course, at the end of the day, it all comes back to the incoming inflation data and, relatedly, whether the Fed’s dependence on those stale figures proves to be just as ill-advised with price growth receding as it was when price growth was accelerating.

{kind=link}

I just finished reading what I’d call a biography of Charlie Kindleberger. More an economic historian than theorist/statistician, he suggests ‘muddling through’ is what actually happens during global economic crisis. Looks a lot like what’s happening.