For the better part of a dozen years after the financial crisis, central banks were widely viewed as responsive to market outcomes.

In itself, that was nothing new. The vaunted “Greenspan put” predated derisive social media memes about policymaker complicity in financial asset bubbles by a quarter century.

But in the post-Lehman era, monetary policy’s responsiveness to developments in risk assets became more frequentative and iterative to the point that markets, and particularly equities, acted as a real-time referendum not just on policy decisions, but on the trajectory of future policy as communicated by officials in various public speaking engagements.

This became an open exchange of ideas. Markets were granted a license to co-author the policy script. The audience was no longer confined to the role of observer, and central banks not only acknowledged the existence of the audience, but solicited their input. Not surprisingly, this resulted in market-friendly policy outcomes.

During Janet Yellen’s tenure, volatility was nearly extinguished in its entirety. That state of affairs culminated in the rise of the stay-at-home vol-seller, a purportedly ubiquitous (but mostly apocryphal) character, embodied by a Florida man who, according to his own account as documented by The New York Times, quit a managerial position at a big box retailer to day trade the VIX using a popular retail product which famously imploded on Jerome Powell’s first day as Fed Chair.

Following Yellen’s decision to postpone liftoff at the September 2015 FOMC meeting amid market upheaval triggered by China’s overnight devaluation of the yuan the previous month, Deutsche Bank’s Aleksandar Kocic suggested this dynamic had effectively been formalized. “[The] Fed’s communication strategy, it is becoming clear, is an equivalent of what in theater context is referred to as removing the fourth wall whereby the actors address the audience to disrupt the stage illusion,” he wrote. “An unalterable spectator becomes an alterable observer who is able to alter. The eyes are no longer on the finish, but on the course — what the audience is watching is not necessarily an inevitable self-contained narrative.”

That changed in 2022, not because anyone acknowledged that the dynamic was perilous and, through its impact on asset prices, conducive to worsening inequality, but rather because the persistence of inflation required central banks to turn a deaf ear (or, more aptly for the metaphor, a blind eye) to markets. With inflation triple and, at the peak, quadruple, target, the protestations of markets to aggressively tighter policy were rendered irrelevant.

Writing in his year-ahead preview (which doubled as a retrospective for 2022), Kocic referenced the above in explaining what happened. “Such an aggressive pace of rate hikes has been disruptive for the market which had developed, over the past decade, a special fondness for, and emotional attachment to, low rates and accommodative monetary policy,” he said, adding that,

The sudden switch to a superhawkish stance was practically an overnight erection of the fourth wall in the Fed/ market dialogue. In the markets’ view, it was a removal of the safety cushion and, effectively, a massive withdrawal of convexity with which the market used to be flooded since 2008. All these undermined the market’s confidence that its complaints would be heard or that they would matter this time around.

The result was an anomalous year for financial assets in virtually every respect. Complicating matters immeasurably was the creeping suspicion that inflation’s return was more than a “transitory” phenomenon destined to fade as pandemic disruptions resolved.

Inflation is famously difficult to dislodge once it’s embedded in wage-setting and consumer expectations. That meant that even if the factors which contributed to its initial rise in 2021 disappeared entirely, its drivers might shift by then — like the pandemic itself, it might evolve.

As supply chain frictions resolved and consumer demand for things like home goods and electronics abated, disinflation set in on the goods side, but by that time, the lagged effect from the pandemic housing boom was beginning to manifest in shelter inflation (figure below).

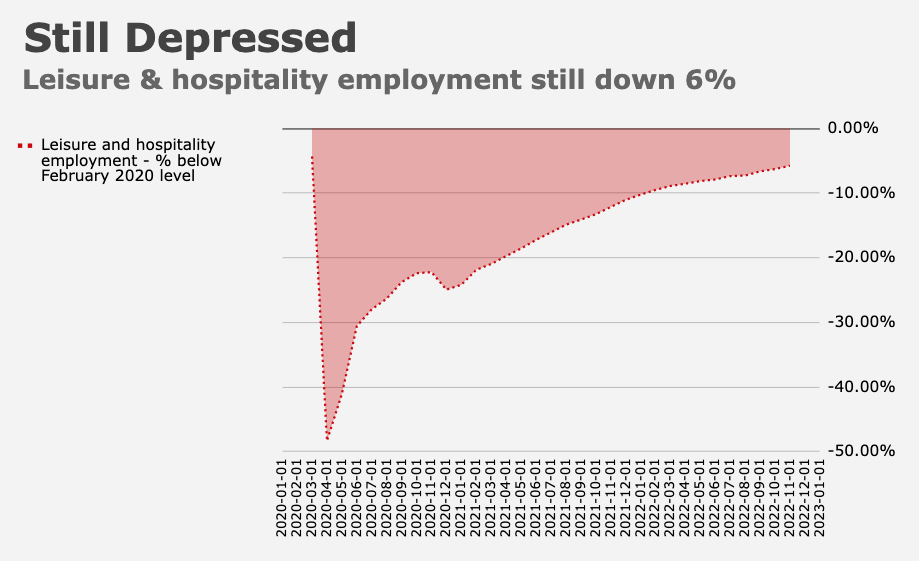

At the same time, the shift in consumer spending strained a services sector running woefully short on labor. As of the November US jobs report, the leisure and hospitality sector remained 6% short of pre-pandemic employment levels.

As Powell conceded during remarks for a Brookings event in late November, early retirements attributable to pandemic dynamics aren’t likely to come back to the labor force, which, when considered with a well-documented immigration shortfall, suggests chronic and structural worker shortages, with potentially long-lasting ramifications for wage growth.

As you might imagine, there’s a link between unfilled job openings in key services sectors and the drop in foreign workers. “In spite of upward pressure on wages in several sectors… the number of unfilled job openings relative to employment has remained very high,” Giovanni Peri and Reem Zaiour, from the University of California, Davis, wrote earlier this year, adding that “the absence of foreign-born workers plays an important role [as] the sectors that had a higher percentage of foreign workers in 2019 had significantly higher rates of unfilled jobs in 2021.”

Labor’s efforts to reestablish itself as an economic actor with clout likewise suggest upward pressure on wages may be an issue in virtual perpetuity. I’d note that the phenomenon isn’t confined to reinvigorated union activity in the US. In December, the UK grappled with mass strikes and walkouts staged by public sector workers demanding better pay to help close an unprecedented pay growth disparity with their private sector counterparts (figure below).

Tellingly, both public and private sector workers in the UK are experiencing deeply negative wage growth when adjusted for double-digit inflation.

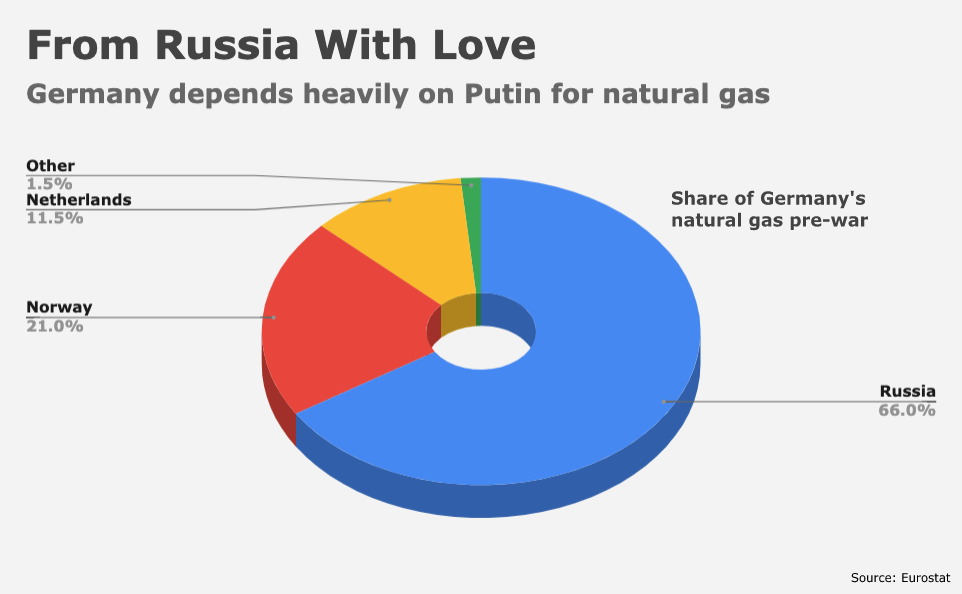

The war in Ukraine injected additional uncertainty into an already fraught macro conjuncture. The suspension of disbelief inherent in the juxtaposition between Europe’s dependence on Russian energy and Vladimir Putin’s annexation of Crimea and ongoing efforts to assert dominion over his neighbor through separatist movements, was emphatically shattered by the invasion. Shortly thereafter, Russia was disabused of the notion that its reserves were safe as G7 claims. Like the fantasy that a confederation of Western democracies could safely entrust its energy security to a hostile, autocratic state, the notion that an autocrat unwilling to accept Western economic and political hegemony could entrust his reserves to Western inside money was a myth of convenience. Both sides had to face reality in 2022.

The ensuing energy crunch in Europe threw the climate crisis into stark relief. Tragic irony lurked around every corner. For example, Germany, the hardest hit by Russia’s curtailment of cheap natural gas, was at one point compelled to consider leaning on coal, but that entailed shipping the dirtiest of dirty fuels up a waterway which, in places, was too shallow to facilitate transport thanks to the very same climate change the country was trying to combat.

Prices for all sorts of traditional energy skyrocketed (figure above), as did power prices, threatening to plunge Europe’s largest economies into deep recessions.

The capacity of the ECB and the Bank of England to cushion the blow was constrained by soaring inflation which was, of course, the direct result of the very same war-related dynamics behind the looming recessions.

Meanwhile, Russia, cut off from Western financial markets and laboring under more sanctions than Iran, Syria, North Korea, Venezuela and Myanmar combined (figure below), sought to expand its flowering strategic partnership with Xi Jinping’s China.

That raised the specter of a so-called “new world order,” loosely defined by the rise of an alternative, commodities-based reserve system backed (implicitly or explicitly) by the Chinese yuan. That thesis was expounded by Zoltan Pozsar to quite a bit of fanfare and, in some corners, to trenchant criticism.

Even after all this, central banks remained reluctant to countenance the idea that the world had changed, even as some policymakers, including the Fed’s Tom Barkin, readily conceded that monetary policy’s price-growth management efforts during The Great Moderation benefited from structural disinflation. “I’m concerned that our success in managing inflation over the last twenty years was partially enabled — it was good policy but it was also tailwinds which were disinflationary,” Barkin said, while chatting with reporters after a June speech in Richmond.

If some of those tailwinds (the enablers) have now turned into headwinds, the effectiveness of monetary policy in controlling inflation may be commensurately diminished. As I never tire of reminding readers, humanity’s natural state isn’t orderly peace. Indeed, the period we typically associate with economic and geopolitical calm was marred by unspeakable tragedies, including famine, war, terror, burst financial bubbles and economic crises aplenty.

2022 may, in hindsight, be seen as an anomaly, or it may one day be remembered as the year during which two generations of humans fortunate enough to be born into democracies during Pax Americana and The Great Moderation, were reminded that in fact, Pax Americana and The Great Moderation were the anomalies — that our assumptions about the world, and, far more narrowly, about markets, are the product of recency bias.

In that context, 2023 could be the first year of a return to “normal” (in scare quotes) or the third year of a return to normal (with no scare quotes). If it’s the latter, and central banks refuse to accept (or fail to understand) that The Great Moderation is no more, they’ll likely persist in a quest to restore inflation to target while refusing to revisit the definition of price stability. In that scenario (i.e., a scenario in which the macro conditions that defined The Great Moderation don’t reassert themselves), policymakers’ quest will be futile in direct proportion to how much of central banks’ success over the past two decades was attributable to the disinflationary tailwinds Barkin spoke of in June.

Powell’s press conference following the December FOMC meeting suggested the Fed isn’t inclined to reinstate the market’s license to co-author the policy script until inflation is on a sustainable path back to 2% which, again, may mean never even if policymakers don’t yet realize it. Christine Lagarde’s aggressive remarks the following day represented an even more forceful reclamation of central banks’ sole discretion to write the script, and given inflation dynamics in Europe, hers may be a particularly quixotic quest to restore headline inflation to an arbitrary target.

We often speak of the market’s dependence on cheap money, abundant liquidity and forward guidance as an addiction liability for central banks. To mix metaphors, the audience are the addicts, and revoking their license to co-author the policy script (rebuilding the fourth wall) is to provoke shrill protests, confusion, withdrawals and, in the most extreme cases, death.

Prior to the pandemic- and war-era inflation, the argument for the removal of accommodative monetary policy was straightforward: The time for emergency-like policy settings had long since passed, so all we were doing by keeping them in place was perpetuating a dangerous addiction conducive to carnival-esque dislocations in capital markets which, in the event an exogenous shock were to force the overnight abandonment of accommodation, would unwind to disastrous effect.

But anyone who’s ever experienced or dealt with real-life addiction knows there’s a threshold beyond which the accumulated liability is so pervasive that proactive detox is objectively suboptimal in the absence of evidence to support the contention that the addict is in imminent peril. As late as 2015, there were no outward or, really, inward, signs that my famous affinity for fine spirits put me in imminent peril. Sure, there was a long list of people who would attest to the idea that the mounting cost of my decadesold love affair with scotch and bourbon was unsustainable, but crucially, until mid-2015, that list didn’t include anyone for whom my problem mattered in a professional capacity, and until 2016, didn’t include any medical professionals.

A voluntary, proactive breakup with Balvenie, Laphroaig, Blanton’s or, on “poor” days, Buffalo Trace, would’ve had a demonstrably adverse effect on my capacity to, for example, deliver enraptured speeches to undergraduate students at schools I couldn’t have gotten into myself when I was a young man. At the time, standard blood panels revealed no obvious evidence in support of emergency detox. In short: The argument in favor of abandoning my several inebriant soulmates rested solely on improving social interactions I had no interest in in the first place. But, much as Larry Summers described the likely sequencing of America’s looming recession, my reckoning took longer to happen than anyone imagined, but when it did happen, it played out faster than I ever imagined it could.

In 2016, the psychological drain from seeing my name in the national press tipped my physical health into crisis. The process was hastened by my suddenly perilous accumulated addiction liability. Upon successfully completing a lengthy hospital stint (where successful completion means that I lived, much to the chagrin of at least a few people), I was forced to rebuild the fourth wall between the play that is my life and the addiction which, for half of that same life, enjoyed a license to co-author the script. Much as central banks’ consultation with addicted markets led inescapably to market-friendly policy as the path of least resistance, my own consultation with my inebriated self led invariably to the accommodation of alcohol as the surest avenue to an uninterrupted status quo which, much like never-ending stock rallies, was an enjoyable experience facilitated by the artificial suppression of volatility.

I was spared the anguish of the many unwinds that would’ve normally accompanied the resolution of myriad biological dislocations — by a coma. When I woke up, I was in a different hospital, in a different state, in a different month. The detox process was complete. And that was that.

A half dozen years later, markets enjoyed no such easy out. In 2022, an acute economic health crisis (inflation) compelled central banks to remove accommodation in cold turkey fashion. Cognizant of the extreme ambiguity that forced policymakers’ hand, financial assets reacted violently, not just to the deprivation of the acronyms to which they’d become addicted (ZIRP, NIRP and LSAP), but to the terrifying prospect that the macroeconomic conditions which gave central banks the plausible deniability to keep administering the drugs, might not be restored anytime soon.

“As inflation continued to show unexpected resilience above 6% in this cycle in the light of multi-dimensional space of risk, breakdown of the standard frames of reference and ambiguities regarding the rates path and its long-term consequences, market confidence has gradually eroded and risk premia and market volatility reached crisis levels,” Kocic wrote last week. “Persistence of high volatility and occasional outbursts of outsized exotic modes of the curve continue to remind us that these times are different from anything we experienced in the past.”

I’d submit, again, that our lookback window is clouded by recency bias. The figure (below) shows the long history of inflation in the UK for context.

Of course, Wall Street strategists are constrained by occupational necessity to speak in terms of recent history — clients aren’t likely to glean much from a derivatives strategy piece which casually notes that if you look back at 5,000 years of history, there were plenty of periods during which rates volatility (for example) would’ve likely been much higher had anyone bothered to measure it.

But that brings us right back to the same question for 2023: Will policymakers in developed markets be compelled to conceptualize of the nexus between macroeconomics and markets as something other than the kind of controlled laboratory experiment it’s been since the onset of The Great Moderation?

If the answer is yes and policymakers accept that answer, it could open the door to the reestablishment of a dialogue with markets, but on healthier terms. If, for example, 3% core inflation is achieved and risk assets protest loudly against additional monetary tightening aimed at bludgeoning demand until inflation falls back to 2%, central banks may do well to listen out of respect for the possibility that the world has changed.

If the answer is yes and policymakers don’t accept that answer, it could open the door to ongoing withdrawal symptoms and intractable volatility as markets accept the new macro regime while policymakers insist on living in a world that no longer exists. The tension there would surely be too much for markets to abide.

The least likely outcomes, in my view, are scenarios that don’t entail some manner of reckoning with a permanent (or, at the least, a semi-permanent) macro shift. I alluded to one such scenario above. It’s possible, I suppose, that markets will simply get over it vis-à-vis their addiction to low rates, liquidity provision and forward guidance, much as I was able to bid a once-and-final farewell to single malts. In such a scenario, true price discovery returns, models gradually incorporate a wider distribution of outcomes, risk parameters adjust accordingly, and with the exception of a few “near-misses” here and there (e.g., the UK LDI blowup in October), markets are able to adapt and cope with central banks which pursue price stability at all costs, as long as “all costs” doesn’t mean economic depressions (with a “d”).

Alternatively, 2023 could be the year inflation recedes sharply, freeing central banks to revert to some version of business as usual as we’ve known it since the late 80s. That seems far-fetched to me, particularly given that a return to The Great Moderation macro norm would also require the near complete resolution of supply chain disruptions, a reinvigorated globalization push, a Russian retreat into geopolitical obscurity and a re-acquiescing of the proletariat in developed economies to a fate of modern day serfdom after tasting bargaining power for the first time in decades.

Last week, Rabobank’s Michael Every reminded his own readers that just prior to the pandemic, unnamed “optimists” (I’m sure he had some people in mind) tried to sell market participants on the idea of a new Roaring Twenties. So far, that hasn’t panned out. “As warned, the 2020s have not held the promise of flappers and speakeasies,” Every joked. “At this stage, it looks like 2023 will make it four bad years in a row.”

{kind=link}

{kind=link}

You must be logged in to post a comment.