In addition to a cacophony of policymaker soundbites, traders will be compelled to grapple with what could be a double-digit inflation print out of Europe this week.

The flash estimate for price growth in September is due Friday and although consensus expects 9.6% from the headline, a handful of estimates suggest CPI may have reached (or exceeded) 10% this month.

Whatever the actual number is, it’ll doubtlessly underscore the urgency of the situation, as will country-level data due prior to the bloc-wide reading.

The juxtaposition with the ECB’s policy settings remains farcical, even after this month’s upsized hike increment. The bank’s staff projections (figure below) are mostly meaningless. Nobody has any idea what inflation will be in the eurozone next year, let alone the year after that.

The projections show price growth moderating and falling back to target, because what else are they going to show? What’s the ECB supposed to say? That it’s wholly indeterminate? That, for all they know, inflation could be 20% in 2024 just as easily as it could be 2%? Forgive me, but their task is to goal-seek a steady decline back to target. So that’s what they did. They surely employed some math along the way, but they needn’t have bothered. They could’ve just used a Sharpie to append the chart like Donald Trump’s Hurricane Dorian cone.

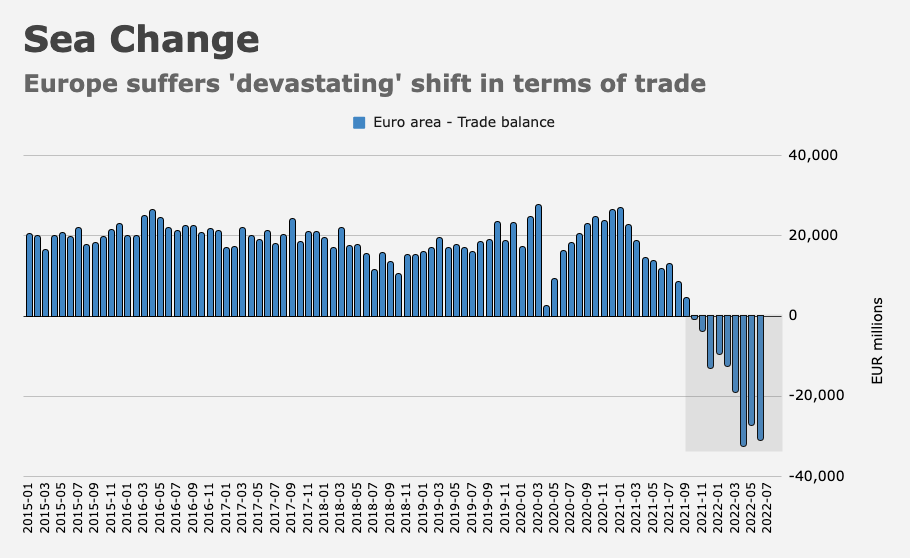

The ECB ostensibly believes they can help the inflation situation by delivering a series of additional aggressive rate hikes, but I’m skeptical. As discussed at some length here following this month’s 75bps rate hike from Christine Lagarde, the ECB is largely irrelevant. Inflation in Europe depends on efforts to tackle energy prices and developments in Ukraine. Gas and power prices are such that demand destruction is inevitable with or without tighter monetary policy.

Last week, a reader wrote to ask whether I think the ECB’s increasingly hawkish policy stance makes sense considering so much of Europe’s inflation impulse is out of the central bank’s hands. I said it does make sense in that,

- It’s what they’re “supposed” to do. Inflation is too high, so you hike rates. Or so says orthodoxy.

- A better argument might be that emergency settings didn’t make sense in the first place a decade removed from the EU debt crisis. So, now that monetary policy has done its part to cushion the blow from the pandemic, and with the ECB committed to capping spreads via TPI, now’s a good time to get back to more normal policy settings.

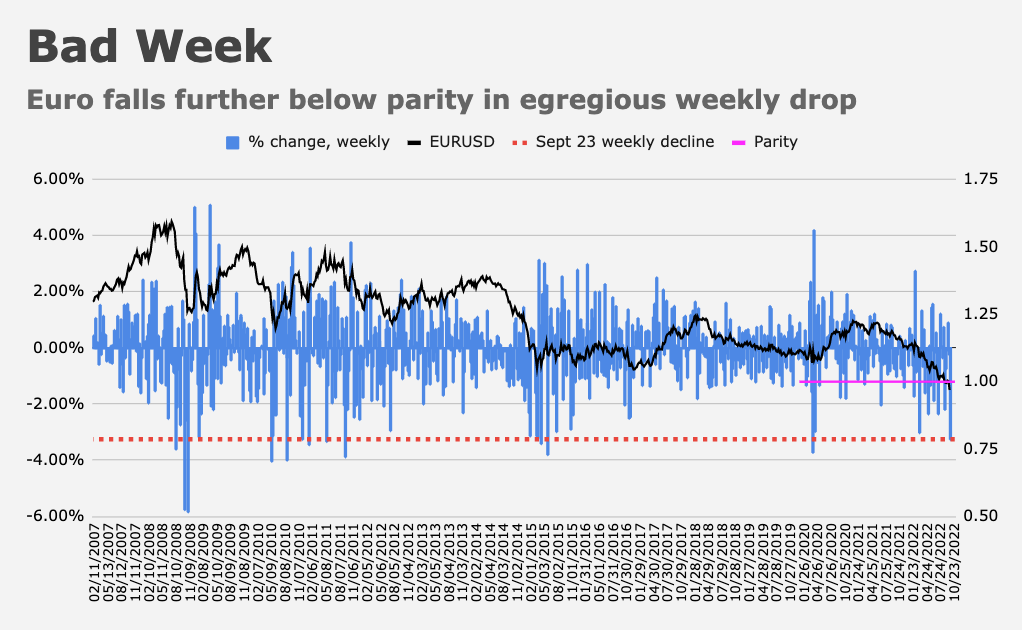

- Another decent argument is that the euro is in free fall, so hiking rates is necessary to put a floor under the currency and avoid pass-through inflation and additional terms of trade shocks.

Having enumerated those three (admittedly important) caveats, I’d still suggest aggressive rate hikes from Lagarde will prove mostly fruitless.

For one thing, the ECB is so far behind the curve that even if it was the “right” course of action, they couldn’t possibly move fast enough. Rates were still negative when headline CPI sported an 8-handle. A lot of that was due to the sequencing they committed to in their forward guidance (vis-à-vis PEPP, then APP, then rate hikes) but irrespective of the excuse, they were running NIRP with 8% inflation. It’s not possible to recover from that unless you move in monumental (e.g., 200bps per meeting) strides.

More importantly, I’m not convinced the ECB has any hope of impacting inflation expectations. Monetary policy transmission in the eurozone is already convoluted enough given the difficulty inherent in crafting a unitary monetary policy for disparate countries all running different fiscal policies. When you throw in the dominance of food and energy in the inflation mix in Europe, it’s not obvious that the ECB can materially impact the expectations channel, let alone in any uniform way across locales.

Recessions are assured (depending on the country), and while I guess monetary policy can make those recessions worse in an effort to destroy demand, the depth of the downturns depends more on what individual governments do to subsidize power costs and cushion households, and what happens in Brussels regarding an EU-wide plan to intervene in energy markets.

I’m sure readers active in EU rates will dispute this, but personally, I don’t see a scenario where the ECB is even a swing factor, let alone the driving force. Rather, it seems to me they’re just hiking rates because that’s what they’re supposed to do, and because there’s an outside chance they can stop the bleeding in the currency.

Obviously, what the ECB does will have direct implications for the banking sector, but when it comes to demand for credit (and the willingness to extend it), I think that too comes back to how the energy crisis and the war develop.

One major lesson from the past two years is that when it comes to generating real world inflation (as opposed to asset price inflation), fiscal stimulus and supply constraints play a larger role than monetary policy. Who knew, right? Yes, massive liquidity injections and the wealth effect (from higher stock and home prices) matter, but the post-Lehman era had plenty of that, and all we had to show for it was richer rich people, falling money velocity and below-target price growth. You needed fiscal largesse on a massive scale and a historic negative supply shock to create real world inflation. Given that, I doubt it’s possible for monetary policy alone to snuff out above-target CPI, even if they can undercut asset prices. Or at least not without an offsetting positive supply shock and more targeted fiscal policy.

If it turns out that only massive industrial policy will be sufficient to deliver the necessary positive supply shock, then central banks will have a huge role to play, likely through yield-curve control and the funding of government spending. But that’s another debate.

{kind=link}

{kind=link}

All CB flying blind ?

Like H_ said it well. Central bank is one force that can influence inflation, but not really control it.

Central bank can only control money, which is really just demand. In a supply constrained world, their only hope is demand destruction to bring price into balance. When debt is expensive enough, debt and hence money will be destroyed.

Thanks Mr H. Would be great if you could share more thoughts specifically on EUR/USD in light of all teh above