It’s all housing on the data front in the US this week, and with Fed officials in their pre-meeting quiet period, consensus isn’t likely to coalesce around a full percentage point rate increase at this month’s gathering.

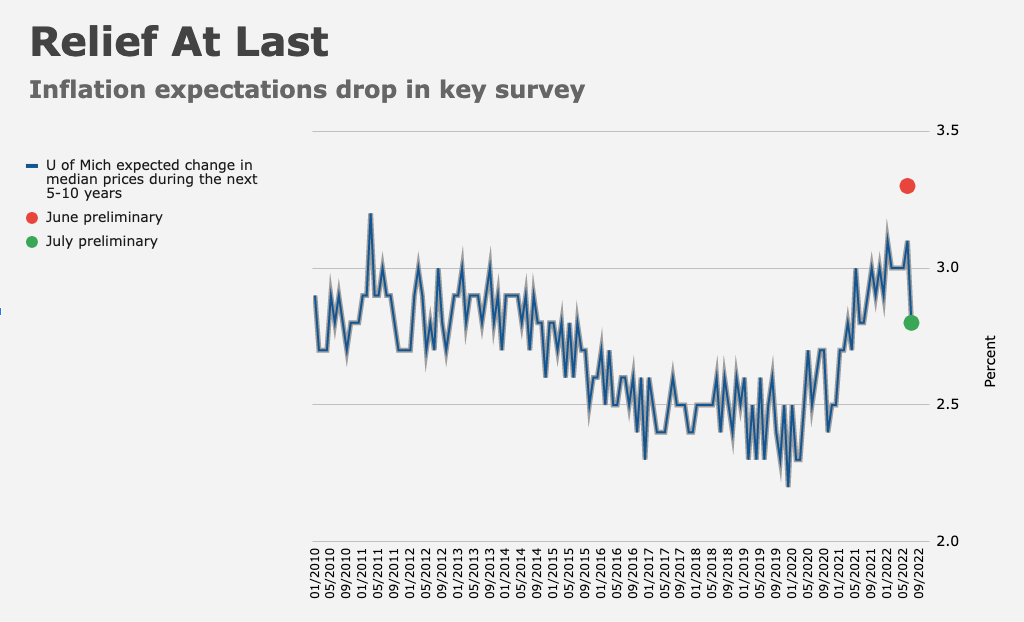

Barring a string of wholly anomalous housing prints or a monumental equity rally that suggests stocks are inclined to make a run at records, June’s CPI report and July’s preliminary read on University of Michigan inflation expectations were the final word. Although you can make a case for a larger move based on the inflation figures, longer run expectations printed a one-year low in the Michigan poll. When taken in conjunction with post-CPI remarks from Christopher Waller and Jim Bullard (who, despite being at the vanguard of alarmist calls for more aggressive hikes, weren’t inclined to wholeheartedly endorse an all-in approach), 75bps is the more likely outcome.

That’s not to say banks calling for a 100bps move don’t have a case. On Wednesday, following the CPI numbers, Nomura said they expect a larger increment from Jerome Powell, Citi echoed that call on Thursday and SocGen followed suit on Friday. Retail sales figures for June beat expectations (you can spin a different narrative by adjusting for prices, but I’ll eschew that temptation) leaving the 100bps thesis largely intact, but the drop in consumers’ outlook for price changes on a five- to 10-year horizon was considerably larger than many expected.

“It’s far too soon to conclude forward inflation expectations are well-anchored [but] the case for 100bps has weakened considerably in the wake of the data,” BMO’s Ian Lyngen and Ben Jeffery said, of the Michigan expectations print. “Similarly, 10-year breakevens below 240bps and 5-year 5-year forward drifting toward 205bps reflect an investor base increasingly convinced that the Fed has the conviction to retain and execute on the 2% inflation target,” they added. The figure (below) makes the point.

Again: 100bps isn’t out of the question. If nothing else, June’s inflation report helped make the case for a third 75bps hike in September, assuming policymakers decide against 100bps later this month.

“Much of the move occurred following the CPI report, where price pressures were broad based; our economists believe the nearly four decade high rent reading poses upside risk to the path of Fed funds in the second half of this year,” Goldman’s Praveen Korapaty said, referencing market pricing for a full-point move. “In addition to increases in hike pricing for the next meeting, market-implied terminal rates, which were within our economists’ baseline 3.25-3.5%, repriced about 20bps higher.” Some of that, Korapaty acknowledged, was attributable to the Bank of Canada’s shot across the bow.

Markets still seem to doubt the Fed’s resolve when it comes to getting rates up near 4%, never mind the 5% floated by the likes of Bill Ackman, Bill Dudley and others. But, as Korapaty went on to say, Goldman’s view is that “absent guidance to the contrary,” recent messaging from Fed officials, who didn’t unequivocally rule out a larger move, “will cause markets to maintain some premium for a 100bps hike for July, a healthy premium for another 75bps hike in September going into the upcoming meeting and presents some asymmetry to the upside to terminal rate pricing.”

Although commodity prices have come down, which should eventually help headline inflation moderate, there are palpable concerns over rental inflation and particularly the relationship with wages. I discussed that at length in “Chickens, Eggs, Hawks And Doves.” The figure (below) suggests shelter inflation hasn’t peaked yet or, if it has, isn’t likely to dissipate in a material way.

“There are significant lags between home-price appreciation, labor compensation and rents,” TD’s Priya Misra, Gennadiy Goldberg and Oscar Munoz wrote last week. “Home price appreciation tends to outpace rent inflation by 20 months and labor compensation tends to outpace rent inflation by 11 months.”

The bank said rental inflation likely won’t peak until January, when it may exceed 6%. TD’s model shows little in the way of moderation from highs seen early next year through the end of 2023, by which time market pricing suggests the Fed will be cutting rates.

Headlines in the new week will also tout the inverted 2s10s. “While we’re sympathetic to the Fed’s implied assumption that outright conditions reflect a robust underlying economy and there’s a window for a soft(ish) landing, the market is signaling the potential for a more problematic touchdown,” BMO’s Lyngen and Jeffery said, adding that “one needs to look no further than the 2s10s spread.” It’s also notable that two-year real yields managed to trek into positive territory.

The Fed will have a very good idea of what the advance read on Q2 GDP will show when they deliver their decision on July 27. One risk (and I’m sure I’ll revisit this frequently over the next two weeks) is that even if the GDP print is lackluster enough to give the Fed a bit of dovish cover, June’s personal consumption data (and PCE prices), as broken out separately on July 29, and particularly Q2 ECI data due out at the same time, could make a strong case for a 100bps hike — two days too late to matter.

On deck this week in the US: NAHB, housing starts, existing home sales and the Philly Fed. It’s possible equities could extend Friday’s relief rally. It says a lot about how far we’ve come when 75bps hike increments are now “dovish.”

{kind=link}

It’s futile to guess. Especially since they are likely to have at least one more bullet anyway. As an investor, my time is better spent trying to figure out what is going on in the real economy now. If you somehow manage to get that right, you are ahead of the game.

I hope they do 100 bps, they’ll have very little room to maneuver if they raise less and inflation is still rising. Zelensky’s talking about success by winter but in this very dynamic environment that’s too far away.

The Fed (and even the government) have a lot more tools to deal with a (hopefully) mild recession.