At this point, it’s scarcely worth mentioning how far we’ve come on the monetary policy front. But I’ll mention it anyway.

There was a time when suggesting the Fed might resort to 50bps rate hike intervals to tame inflation made you a hawkish outlier. Such a view was considered extreme, if not outright laughable, when 2022 dawned.

Six months and six increasingly severe inflation escalations later, markets priced a 100bps rate hike at the July FOMC meeting as a coin flip. That was the situation on Wednesday afternoon in the US, following another dastardly CPI report which, among other things, featured a fourth consecutive upside surprise on the headline print, no small feat considering how hot those prints are running.

Jerome Powell, in an effort to placate those concerned about the impact of extremely aggressive monetary tightening on the US labor market, recently adopted a talking point centered around the notion that even if some jobs are ultimately lost to the inflation fight, an economy beset by unanchored consumer price expectations won’t work for anyone.

The June minutes, which gave markets some context for the thinking behind last month’s 75bps move, were generally seen as “stale” given i) the deceleration in economic momentum observed since June’s policy gathering and ii) concurrent speculation about the rising odds of an imminent US recession. On Wednesday, following another blistering CPI report, one passage from the account of June’s proceedings echoed loudly:

Many participants judged that a significant risk now facing the Committee was that elevated inflation could become entrenched if the public began to question the resolve of the Committee to adjust the stance of policy as warranted.

A lot hangs on the definition of “as warranted,” and specifically who gets to make that judgment. Some readers are occassionally frustrated by my insistence on precise language, but there’s a reason I demand it beyond being a pedant.

The seemingly straightforward passage excerpted above can mean two different things. It could mean the Fed is concerned that the public will start to doubt monetary policymakers’ commitment to do what they, policymakers, believe is necessary to tamp down inflation, or it could mean the Fed is concerned that the public will start to doubt monetary policymakers’ commitment to do what they, the public, believe is necessary to achieve the same goal.

It’s possible, of course, that given the nature of the problem (i.e., the extent to which inflation is a product of supply factors the Fed can’t control), no adjustment will be wholly sufficient. But the (erroneous) assumption harbored by economists is that there’s some quantum of tightening which, one way or another, will be enough to corral inflation. It matters quite a bit who renders that judgment.

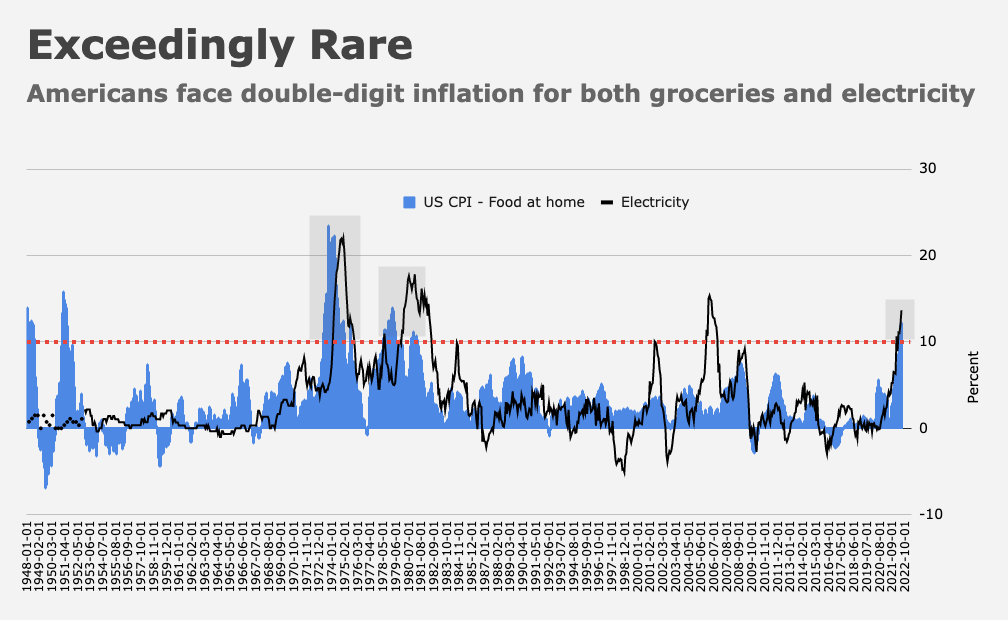

Inflation headlines were above the digital fold on Wednesday, and not just on the financial pages. In addition to feeling inflation at the gas pump and at the grocery store, Americans are now seeing it and reading about it too. It’s not just their imagination. “I told you it was getting worse!” someone might exclaim, in the direction of their significant other, while perusing Wednesday’s top stories before a home cooked meal which was 12.2% more expensive than it was this time last year.

The public is now part of this debate. And not just the investing public. The voting public. Main Street. The people who purchase the goods and services for which prices are rising the most.

The nexus between Fed policy and the bond market is pernicious enough on its own without regular people starting to form their own ideas about what counts as a sufficiently forceful response to generationally high inflation. “One percentage point” is a round number. It doesn’t sound esoteric to regular people like “75 basis points” might.

There’s a material risk that the media echo chamber will shape public opinion such that regular people come to expect a 100bps move later this month — that, after reading about it, Main Street defines “as warranted” by reference to the full percentage point rate increase bandied about in the news. Consider also that if you tell the average person the cure for inflation is higher rates and that person becomes acutely concerned about inflation, they might well expect larger rate hikes in succession given successively higher inflation prints.

Whether any of that is rational (or “warranted,” as it were) is largely irrelevant given the Fed is concerned with the psychological component of inflation, that being one of the only two components they can control (the other being demand, which is related to, but not synonymous with, inflation psychology). The latest vintage of the New York Fed’s consumer survey showed one-year expectations hit a new series high in June (figure below).

Longer-term expectations were more muted, and, as ever, there was some interesting nuance to be had in the demographic breakdown.

But as Powell put it in May, this is “not a time for tremendously nuanced readings of inflation.” He meant actual, realized inflation, but the same could be said of inflation expectations.

Yes, the Fed finds some solace (a lot, even) in the idea that consumers still don’t expect the kinds of totally unacceptable inflation outcomes currently manifesting across the economy to persist longer than, say, 12 to 18 months. But real wage growth continues to be deeply negative. As long as that’s the case, and labor remains scarce, workers have every incentive to demand higher pay. There’s no sense in which sharply negative real wages are a “good” thing. You want cooler wage growth, but not that way.

Up to and until the Fed does so much that they either engineer a deep recession or reach some threshold beyond which it’s possible for Powell to throw up his hands and say “We’ve done our part,” CPI reports like June’s mean policymakers are duty bound to keep up the pressure. It’s either that, or confess there’s nothing they can do.

The 2s10s inversion deepened Wednesday, as the short-end sold off on policy expectations and long-end yields fell, at least in part on recession concerns (i.e., in consideration of the implications from an even more aggressive Fed for growth).

At one point, the inversion tagged -24bps (figure above). It’ll get more extreme. It’s just a matter of when.

TD’s Priya Misra took profits on her two-year short from late last month. “The market has pushed pricing for July to 83bps and September to 64bps,” she wrote Wednesday. “Market pricing of the terminal rate rose from 3.25% when we put the trade on to 3.6% [and] while rates can sell off further, high volatility and ongoing worries about recession (likely pushing equities lower) should prevent a move higher in front-end rates.”

Note that there’s still scope for this week’s data to make an even stronger case for a 100bps hike. Or not. Markets will get PPI on Thursday and the preliminary read on University of Michigan sentiment Friday, which will come packaged with an update on inflation expectations. It was the CPI-University of Michigan expectations combo that tipped the scales in favor of a 75bps hike last month. That same combination has the potential to move the Fed in the direction of another escalation this month.

I suggested early Wednesday that the Bank of Canada’s 100bps shot across the bow raises the odds of a matching hike from Powell. “It certainly set the stage for the Fed to mirror the move, although it’s ultimately the underlying US inflation fundamentals that will drive the Committee’s decision,” BMO’s Ian Lyngen and Ben Jeffery wrote, adding that “global central bankers are contending with the same factors increasing consumer prices — energy, food and housing [so] entertaining a 100bps hike isn’t unreasonable given the prevailing balance of risks.”

“We believe the Fed is extremely data dependent right now. Considering the further acceleration in monthly inflation, and the additional upward pressure it may put on inflation expectations, we now expect the FOMC to raise rates by 100bps at the July FOMC meeting,” Nomura’s economics team wrote, in an update. The bank called it a “close call” but said that in their view, it’s “the ‘right’ call both from a forecasting and optimal monetary policy perspective.”

“I think they have time, if they want, to change that expectation to 100,” JPMorgan’s Michael Feroli remarked. “I don’t think they’ve given us a great reason why they should be going slow here, or being gradual.”

Asked at an event in Florida whether the Fed would consider hiking by a full percentage point later this month, Raphael Bostic said “everything is in play.” Pressed to confirm that “everything” includes a hike larger than last month’s, Bostic said “it would mean everything.”

{kind=link}

I would characterize myself as one of the more ‘regular people’ among your readership. My family’s combined income is around 130k. We have a mortgage we were lucky enough to take on just prior to the pandemic (and refi during). Last year at this time I was shouting on this forum (and shot down hard) about the pains of inflation.

On the playground this weekend I was talking to another parent I’d never met before, a plumber.

We were discussing how many kids we had/wanted and he mentioned he and his partner were considering another kid but might hold off because recession.

Point of the story is that regular people are onto the recession and not hung up on inflation expectations. We’re hoping to hold onto our jobs.

$130,000 doesn’t make you “regular people.” It makes you well-off, depending on where you live. “Regular people” is between $40,000 and $65,000, again depending on locale. I realize that many people living in hugely expensive cities are just “barely making it” on $150,000, but it’s not reasonable to expect everyone in the country to take that into consideration when assessing what “regular people” means. A family in a “regular” town (so, let’s call it <150,000 people) making $130,000 is doing just fine right now and is far from “regular.”

Imagine how you’d be feeling right now if your combined household income was $40,000. You’d be worried about a recession, sure. But you’d be terrified every, single time you went to the grocery store, because for “you” (i.e., the hypothetical family making $40,000), $150 is a lot of money.

Please note the qualifier in my comment of ‘among your readership’.

Earning approximately 65k each in the tri-state area is pretty ‘regular’ though even without a qualifier.

Yes, I understand, but I just want to ensure we’re being appropriately sensitive here. I mean, the majority of American families don’t make $130,000. A two-earner income of $65k each in “regular ol'” Mayberry makes you the richest couple in town besides the local coal baron.

That may be true, although I confess I don’t know where Mayberry is.

Wherever it is likely not an apples to apples comparison. A teacher who’s married to a non profit employee in Mayberry (assuming they have such things) likely aren’t the richest people in town…

Unless they are… again, can’t speak to Mayberry…

I do see your point though. The lowest earners are in danger of not being able to stay in the labor force. Either their cars break down, or get repossessed, or they can’t afford gas, or they have a heat stroke to save electricity, or a myriad of other enormous and life altering problems.

wages will have to rise or government assistance will have to pick up the slack, thus the makings of a wage price sprial.

The REAL Mayberry is Mount Airy, North Carolina.

Hawks are flying high. This will not end well. But we will be in a disinflationary environment if powell and the Fed have anything to say about it. Reports I hear suggest retailers will be cutting prices drastically very soon.

The best cure for a recession is…lower prices?

They (the Fed) will crash everything, it is just a matter of how fast it happens and whether they’ll have a chance to put it back together. A mild recession now is starting to look like a pipe dream, a few weeks ago I thought folks predicting a GFC-like slowdown were overreacting, I’m ready to join their choir of doom now.

“CPI reports like June’s mean policymakers are duty bound to keep up the pressure. It’s either that, or confess there’s nothing they can do.” You hit the nail on the head HR.

The Fed is between a rock and a hard place. And furthermore flying blind, as they try to figure out how much pain they must inflict on the economy to get inflation under control, all with no previous playbook to follow or fall back upon!

Hard to manage something like inflation when you are not exactly sure of what it is or isn’t.

Inflation is a condition which reflects a general rise in prices, consumer prices, producer prices, etc. During inflation some prices will be up and some will be down but on average, the overall trend in the prices of a typical basket of purchases is up. A sense of this condition can be had by visiting the website of the US Bureau of Labor Statistics (Google CPI to get links). Tables of data over time will show what has happened in the past several years. The site will also show what the basket is, peoples’ typical expenditure budgets and even the changes in prices of individual items. there are price indexes for houses, pickles, etc. With some effort one can actually use the data on this site, along with personal expenditures by category, to calculate a CPI tailored for just oneself.

With regard to pedantic people- based on my own personal experiences- it seems that the overwhelming and vast majority of pedantic (generally annoying) people fall into the category of:

Those who speak with great authority but questionable accuracy on every single subject they encounter- even to the point of contradicting other people (who are correct).(1)

Obviously, you are the exception- your authority and accuracy displayed in the written words on The Heisenberg Report are a much appreciated combination.

(1) see the character Paul in Woody Allen’s “Midnight in Paris”.

Who is actually enjoying this fear-wrought grind-down? Who would prefer to get it over with, have rates whacked up to where they are duty-bound to go and valuations whacked down to where they need to go, without needless prolongation? If that sounds good, then maybe great big hikes are better than mincing little ones.

It’s meant to make unemployment grow slowly. If credit stops suddenly and we still have high inflation (those with savings can continue to push prices up), we get a depression with lots of suffering.

Producers still need the demand signal to increase output and manageable loans to grow.

As inflation continues to grow, it feels more and more like central banks will be forced to engineer a global depression to tame it. If that’s the only way out of this problem, history will not look very kindly on the era of QE.

QE postponed the recession, that’s all. And don’t forget that QT has barely started.

But there’s no reason for concern! The models say that consumers are awash in savings and jobs are plentiful.

So now we have inflation. Naturally, we examine the variables that affect inflation and consider how the broader economy achieved the current state, how it may have been mishandled, how issues can be addressed, and how the Fed might respond. But money and the economy are also issues on the political playing field.

I loathe political ineptness. The US is a politically conservative country. Whether Republican or Democrat, I want competent leadership in the President’s office.

It’s about time the democrats, especially Joe Biden, go on the rhetorical offensive and tell the broader story about the economy he inherited. The main point to make is the difference between investment in the American people and the US economy, and giveaways to the absurdly wealthy, as in the tax cut of 2017.

I’m not wealthy like Joe Biden or Trump or Paul Ryan. But I did not need the Trump tax cut in 2017. I barely perceived it. It was absolutely unnecessary. In my opinion, it was (purely) a bribe that Trump and Paul Ryan, in the hopes of retaining their offices, paid to the wealthy and the more well-off members of the electorate. But we all know how that ended, of course – Trump and Ryan are gone.

Throw a pandemic into the economic mix in 2020, and the war in Ukraine this year, and you have a virtually guaranteed political and economic mess. The democrats and the President need to see through the fog and point the finger at the excesses of the Trump administration that make the mess worse.

With the growing, and clearly relevant information from the Jan 6 hearings about Trump’s management and conduct of his administration, it’s clear that he was inept, utterly self-serving, and he did not act in the interest of the American people.

Unfortunately, what distinguishes Joe Biden from other Presidents is the distinct absence of his own voice in the bully pulpit. And even more unfortunately, Trump used rhetoric as weapon each and every day, and still does.

Not everyone can make an effective argument. Biden seems to be among the less able. But someone in the administration needs to convey the message about the track record of the far right MAGAs and cite specific facts to the American people about how Trump’s administration did business. The Biden administration is leaving all of its arguments for the 2022 election to the media. Sure, the Jan 6 committee paints an ugly picture of Trump, the republicans, and the MAGA movement. Of course, it will help the democrats. But the facts dug up by the media and the White House records used by the Jan 6 committee are political cannon balls that need to be used for political purposes.

What remains of Donald Trump, the MAGAs, and the Republican Party is a juicy political plum. At the very least, Trump was a self-serving, ego-maniacal buffoon who abused his power and mismanaged the US economy. The time now needs to be seized and used by the Biden administration to shape and support the national, rhetorical story that precedes the elections later this year. Leaving the story to sit untold and, in turn, allowing the MAGA right to tell the story of US inflation, where, in effect, the democrats are abiding without reaction to its potentially terrible impact on the US economy, will undermine any hopes of democratic success in the November election.

On the other hand, active rhetoric by the democrats is required to tell their view of the MAGA and republican story in the 2017 tax-cut, Trump’s downfall and lies, the pandemic, inflation, and the war. Lacking blue voices, an outcome with any blue results becomes far less likely. If Biden is Daddy Warbucks, the democrats running for office in 2022 will be impoverished.