A few days ago, a reader suggested the Fed, having woefully miscalculated while appraising both the scope and duration of America’s inflation problem, might likewise misjudge the size and speed of the turn.

Although Jerome Powell and his merry band of maladroit technocrats still allude, gingerly, to the idea that inflation could fall faster than currently envisioned, the “transitory” debacle rendered such narratives a national bête noire, especially when they emanate from economists, policymakers or, worst of all, policymakers who practice economics. You can’t be that wrong about inflation when inflation is, by statute, your responsibility.

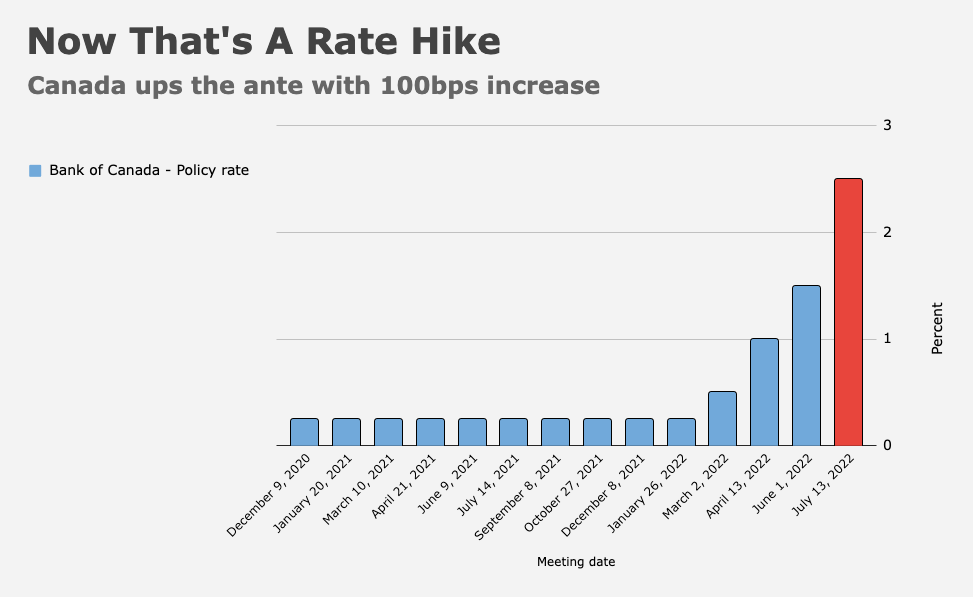

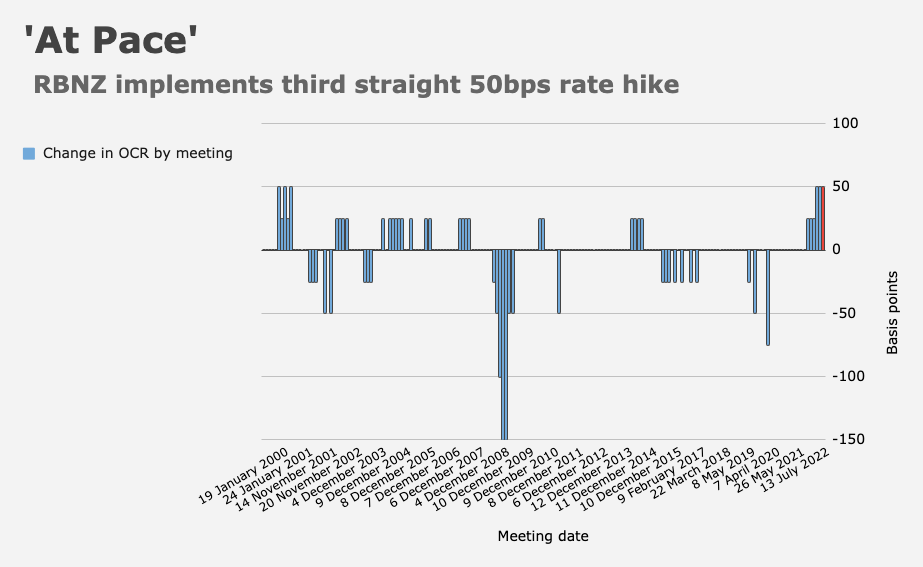

The risk, then, is clear enough: Central banks, including and especially the Fed, are fighting the last war without realizing it, hiking rates at a frenzied pace (figure below), with inflation (headline inflation, anyway) one lucky macro break away from plunging, and economies two or three months removed from recessions.

Yes, inflation is pervasive and it’s the bane of Main Street’s existence, but it’s a manifestation of events that already transpired. Some inflation will, of course, prove “sticky,” but if commodity prices roll over, and headline inflation plummets (exacerbated, ironically, by slower consumption tied to falling inflation-adjusted wages), restrictive monetary policy settings that would’ve been prudent in late 2021 could appear sadistic in the second half of 2022.

“Big rate hikes as central banks play catch up in the coming months risks a ‘recession shock’ morphing into a credit event,” BofA’s Michael Hartnett remarked, suggesting the dollar’s inexorable strength is a “hint.”

Commodity prices are rolling over (figure below). Where they aren’t (or, where they’re at risk of reaccelerating), further gains will almost invariably beget recessions and demand destruction. The UK and Europe are destined for downturns, for example. If flows through the Nord Stream are further curtailed later this month, following maintenance, Germany could face an overnight economic crisis.

The risk isn’t confined to Western economies. Emerging markets are imperiled by the dollar’s inexorable rally (which is in no small part a function of Fed tightening) and China’s anemic Q2 growth data suggested the economic drag from Xi’s COVID containment strategy is even more severe than feared.

And yet, central banks are running a massive credibility deficit. Even if they believed inflation is on the brink of rolling over, they couldn’t say so. Certainly not in public. That raises the odds of a policy mistake even larger (assuming that’s possible) than the one they’ve already committed by staying behind the curve on inflation. The ECB embodies the risk: The bank is set to start raising rates next week with the bloc’s largest economy on the precipice and Italy staring down a new political crisis.

Although Europe (and the UK) are in an especially tough spot, you’ll note that policymakers in Australia, Canada, New Zealand and Sweden are at risk of triggering a destabilizing downturn in their respective domestic property markets, all of which are bubbles. As for the US, BofA’s Hartnett noted that the combination of extremely depressed small business confidence and record low consumer sentiment is reminiscent of deep recessions (figure below).

“The charts increasingly point to a hard rather than a soft recession,” Hartnett remarked. “As does the yield curve.”

None of this is totally lost on central banks. They’re aware of the possibility that, having waited far too long to lean into the inflation fight, they’re now condemned to exacerbating the recessions that some analysts now expect in virtually all developed economies.

All pretensions to data dependence and “nimbleness” aside, policymakers can’t execute anything like an abrupt dovish pivot, even if commodities collapse under their own weight and headline inflation quickly converges to core (or even towards target) as a result. In an effort to ensure inflation is actually dead (not just “resting,” like the Norwegian Blue or feigning death, like the villain from an 80s slasher flick), central banks will almost surely persist in a hawkish bent for too long, just as they loitered in accommodation despite month after month of accelerating price growth.

If true, that’ll mean one of two things. At best, Main Street, by then trudging through the rain-soaked trenches of a shallow recession, will be subjected to a year of self-congratulatory press conferences following policy meetings at which central bankers will keep rates mildly restrictive while taking credit for a “soft-ish landing,” characterized by a relatively modest rise in unemployment and a sharp decline in commodity prices that had very little, if anything at all, to do with monetary policy.

At worst, Main Street will find itself mired in a deep recession brought on by draconian rate hikes executed despite what, by then, could be copious evidence of demand destruction and a total abatement of supply factor-driven price increases. In that scenario, central banks’ credibility deficit with the public will be so large that voters may demand monetary policy be stripped of its independence. “What do we have to lose?” voters will ask, opening the door to populists with printing presses.

{kind=link}

{kind=link}

{kind=link}

All this writing and all we need to hear is when to buy the bottom ?

Oh no, my wink emoji got changed to a question mark. One character, big difference!

Is this a serious comment? This isn’t a stock tips site. If you want Jim Cramer’s real-time alerts or Joe Nobody’s technical buy signals, they’ll be (more than) happy to take your money.

Just feeling feisty. I do read you to time the market though. Or at least to understand the near-term catalysts.

Central banks the world over are in a no win situation. Even if the fomc had perfect timing and called it right, we would still be in the soup. The clue is that they are all in the same boat more or less, despite different timing. Canada is a perfect case study. They withdrew loose policy faster and are still in approximately the same place as powell & co.

Preach. I’ve been following this site for 7+ years, due largely to confirmation bias. I am constantly looking for tidbits of information to make an informed decision about the factors that (may) impact markets. Your ability to capture all of the headlines out of Bloomberg, in addition to synthesizing sell-side research is invaluable. And Cramer is a media clown!

If Bloomberg was even a semblance of competent when it comes to synthesizing the mind boggling number of decent articles they publish into a much smaller (but still huge) quantum of high-quality articles, it’d be the single-best media outlet on the planet. The amount of information they’re able to gather and communicate intelligently is astounding, but they never quite manage to publish articles on par with FT, let alone the Times or something like The New Yorker, despite having access to every conceivable dataset on the planet and despite their formidable roster of reporters. They don’t have any “stars,” per se, but they have hundreds of capable journalists who seem to be confined to a pretty strict template, which prizes conciseness over every, single other consideration. That’s enormously helpful to busy finance professionals who can gather more discrete, individual bits of information in an hour on Bloomberg than they can in 12 hours reading FT, but I personally think it holds them (BBG) back on the media side. I imagine it costs them a tremendous amount of talent. No journalist is going to stick around forever if they’re confined to a cookie cutter, even if it’s the best cookie cutter on the market.

Joe Weisenthal seems like he deserves an exception here!

Joe (and Tracy) are an exception. Sort of. But there again, they’re summarily relegated to the back page, and although I imagine they were probably involved in the branding process, it says a lot about BBG’s view of their work when their segment is called “Odd Lots” and only gets top billing when Tracy can convince Zoltan Pozsar to dial in.

Totally agree. Well said.

Bloomberg does have a governed approach and that formula by extension sometimes begets an irritating but seemingly routine line when speaking to individuals on their exceptional guest roster typically by the way of interrupting; “so are you going to make some news here”. I perceive it as some sort of fluff that can restrict the flow of information on that particular topic from that particular individual, immediately. Having said that, BBG it is the only financial news i listen to or watch. Well except for occasional Saturday PBS Consuelo Mack Wealth Track.

Populists at the helm of the printing press, i cannot wrap my head around the potential outcomes.

If a macro were to calm down (let’s say a truce in Ukraine – after they kick the russians out), and oil/gas were somehow flowing (at least for a more predictable market), and inflation dropped back down… would that make Transitory true (just on a larger timeline)?

And just like nordic NATO expansion was a wonderful own-goal, would these urgent hikes popping Crypto and maybe Chinese real estate bubbles actually be the desired outcome – despite how messy it was to get there?

I was/am on Team Transitory so I think I can speak to your first point.

I think it still counts as a loss because most of the Transitory narrative was based on the idea that supply sided snags and COVID related demand adjustments were going to get solved sooner rather than later.

As it happens, a fair bit of inflation is driven by excess demand (fiscal, supported by monetary). That too is (likely) transitory inasmuch as governments have turned off the spigots AND we haven’t see a wage price spiral take hold but this wasn’t the initial narrative and so we can’t claim victory.

Yeah, I mean, there’s still an argument to be made that “Of course it’s transitory!” in the sense that unless you believe DM inflation is going to run ~8-9% in the interim period between, say, 2024 and our eventual reckoning with all kinds of existential threats, inflation will come down in the developed world, even if it settles ~two percentage points above where it was during the Great Moderation. But it’s far easier for us to make that case here, in the safe confines of the comments section of a website, than it is for Powell to push that line during an FOMC press conference, while speaking to an irritable American public.

For sure.

TBH, I think Powell is doing as well as he can given the renewed paralysis of Congress/the fiscal side of things. Not to mention that, while raising taxes is a theoretical tool to cool off things, in practice, politicians are very unlikely to use it.

And, given that I too did not foresee the second stimulus package being so inflationary, I’m a little hesitant to throw stones at Powell for not hiking earlier.

So, yeah, we are where we are and, apart from sounding confident inflation will come down, I don’t think Powell can do much but hike 75 bps next week.