It’s fair to suggest the macro consensus headed into 2022 is that inflation will remain generally elevated (even if it starts to abate in the back half of the year), prompting central banks to tighten policy, quite possibly to the detriment of risk assets.

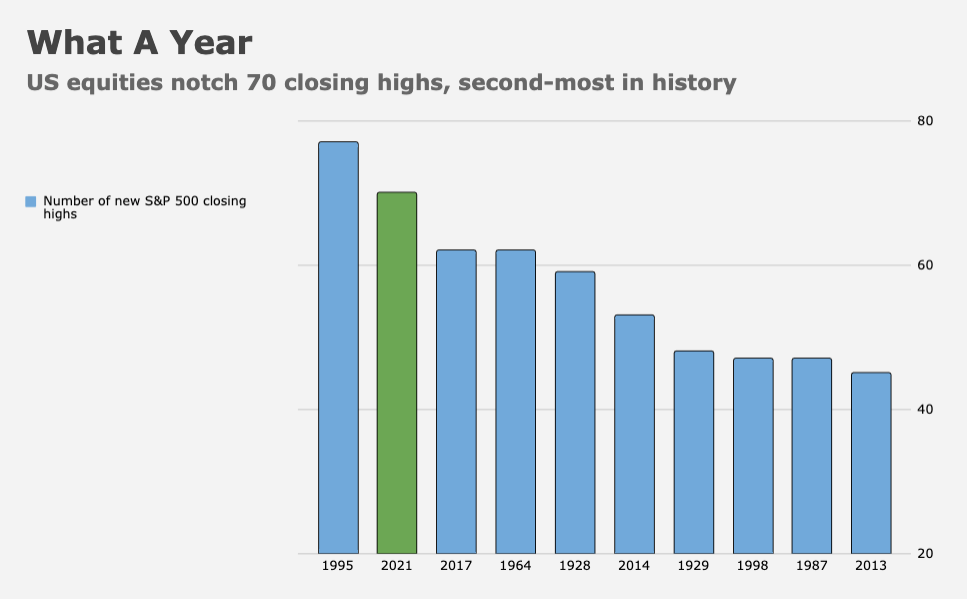

Take the S&P, for example. It remained above its 200-DMA for the entirety of 2021 (figure below), notching nearly six-dozen record closing highs in the process.

Only four times in 40 years has the index gone an entire year without breaching that magic line. In three of those cases, stocks fell the following year.

The S&P’s historic run left multiples stretched, ostensibly arguing for a de-rating in the event of tighter monetary policy which, again, the vast majority of analysts and strategists expect.

“The biggest surprise of [2021] was the global inflation surge, which was particularly pronounced for US goods, global energy and Latin America,” Goldman’s global economics team wrote, in one of their final 2021 notes, published Thursday.

“As a result, G10 central banks tapered or ended asset purchases earlier than expected,” Jan Hatzius and friends continued, adding that “the rate normalization process started in Norway, New Zealand, the UK and much of Latin America and CEEMEA, and is set to broaden and deepen in 2022.”

The figure (below), is useful if you’re looking for a pocket guide to policy normalization, both delivered and expected.

Given what we know about Fed tightening cycles (namely, that they always end in some manner of financial “event”), you’d be forgiven for questioning the plausibility of projections for taper completion, multiple rate hikes and the commencement of balance sheet rundown, all within the next 12 months. Or at least for questioning whether such a pivot could be executed in a way that doesn’t destabilize something, somewhere.

Goldman, you may recall, expects a trio of hikes in 2022 and the start of balance sheet runoff in Q4.

If you wanted to posit a kind of worst case scenario for equities, you might suggest that the very same inflation that’s poised to prompt aggressive monetary pushback will erode profit margins and curtail consumption. As a reminder, real consumer spending flatlined in November.

Margin forecasts have moved sideways for months (figure above).

If Omicron prolongs supply chain disruptions and labor market frictions continue to push up wage costs while consumers retrench, corporate America could experience a profit squeeze.

I’m not sure what the right adjective is when it comes to describing the outlook for equities trading on nosebleed multiples in an environment of margin compression, nervous consumers and Fed tightening.

I suppose any synonym of “bad” would work.

{kind=link}

It was not Rocket Science to predict Inflation at levels seen in this last year but that is not the same as making windfall profits in the Equity markets.. Lasting impacts of all the Sociological issues will destabilize the Economic playing field and much like our Climate issues yield huge changes . I predict 2022 will yield a Geopolitical Nightmare to remember just like Economic and Climate issues will .

H-Man, while “bad” things may be on the horizon — the challenge is turning a “bad” thing into a “good” thing for your portfolio. Covid was a “bad” thing in March of 2020 but depending on how you dealt with volatility, it could have been a “good” thing.