We’ve reached that glorious point in an inexorable rally when all that’s left to do is publish lists of risks.

The first four “sentences” of a prominent Bloomberg article published Saturday were: “Delta cases. Inflation. Fed tapering. China’s crackdown.”

I’m reminded of Donald Trump’s amusing attempts to list his accomplishments as president. He’d mention the tax cuts and then, confronted with a dearth of enacted policies, resort to mentioning nouns with adjectives in front of them (“Second Amendment,” “strong military,” etc). Imagine someone asks you to list the things you did over the weekend. “Mowed the grass, cooked some steaks, baby bird, big truck, red crayon…”

The visual (below) is the obligatory nod to the “tail risks” list from BofA’s Global Fund Manager survey.

The linked Bloomberg article correctly characterized Jerome Powell’s Jackson Hole speech as dovish. It still felt, into the weekend, like too many market participants didn’t quite grasp that, though. Part of the problem may have been the mainstream media, and in this context I don’t mean Bloomberg or CNBC or the Journal. Rather, I mean mainstream media in the truest sense — national media outlets not exclusively focused on finance, markets and/or economics.

I’ll concede I didn’t actually read their coverage, but at least a handful of the headlines I saw suggested the main takeaway from Powell was that the Fed chair “confirmed” plans to roll back stimulus. That wasn’t the takeaway. The takeaway was that Powell all but confirmed a benign (i.e., dovish) timeline for trimming monthly bond-buying and emphasized that the bar for actual rate hikes is not only so high that we can’t even see it from here, but is in fact so qualitatively (and, I guess, quantitatively) different from the threshold for tapering asset purchases, that the two shouldn’t even be discussed together.

The dovish taper was a boon for risk assets in the here and now, as evidenced by Friday’s rally on Wall Street. The explicit (and somewhat forceful) delinking of rate hikes from the taper presents something of a quandary. The point (obviously) was to emphasize that the Fed is still nowhere near discussing liftoff. Indeed, almost every Fed official is on the record parroting some version of that talking point. But someone Bloomberg TV interviewed on Friday appeared to suggest that delinking the two might open the door to rate hikes before the taper is finished depending on the path of inflation over the next 12 months.

To be clear, that person (to the extent I’m not misrepresenting their position) is wrong. The Fed (and especially the leadership) most assuredly isn’t attempting to somehow emphasize their optionality when it comes to using the bluntest tool at their disposal to tamp down a nightmarish inflation surge. The Fed doesn’t need to incorporate any allusions to the “break glass in case of emergency” option when it comes to spiraling inflation. If the US starts to go the way of Venezuela, nobody is going to argue with rate hikes. Powell doesn’t need to sneakily reserve the right to hike rates if the price of bread soars to $45 a loaf. In short, there’s no risk of a rate hike prior to the end of the taper barring some far-fetched turn for the absolute worst on the inflation front.

With that out of the way, I’m starting to believe the taper isn’t likely to pose that much of a risk either. Trillions up trillions in liquidity has quite plainly served to levitate risk assets in the post-financial crisis era, and the post-COVID experience was no different in that regard (familiar figure below).

But there are multiple mitigating factors to take account of as the Fed prepares to gradually pare bond-buying.

First, forward guidance has now become an exercise so recursive that policymakers are telegraphing the telegraphing. That is, traders now get advanced notice when discussions have commenced around how to go about preparing markets for an eventual policy change that will play out over the course of a year. To the extent it’s possible to adjust your mindset for the slow withdrawal of liquidity support, the adjustment period is as forgiving (i.e., long) as it could possibly be.

The read-through from Powell was that September is off the table for an unveil. Goldman agrees, for whatever that’s worth. “Coupled with the FOMC’s intention to provide ‘advance warning’ that tapering is coming, which we assume means a formal warning in an FOMC statement, these dovish comments indicate that the Fed leadership is not considering announcing the start of tapering at the September meeting,” Jan Hatzius said Friday, following Powell’s remarks.

More importantly, it’s not as if the liquidity is going away. Assuming a November unveil and a $15 billion per meeting clip, the taper won’t be completed for a year. The Fed will likely still be buying more than $100 billion in bonds per month in January.

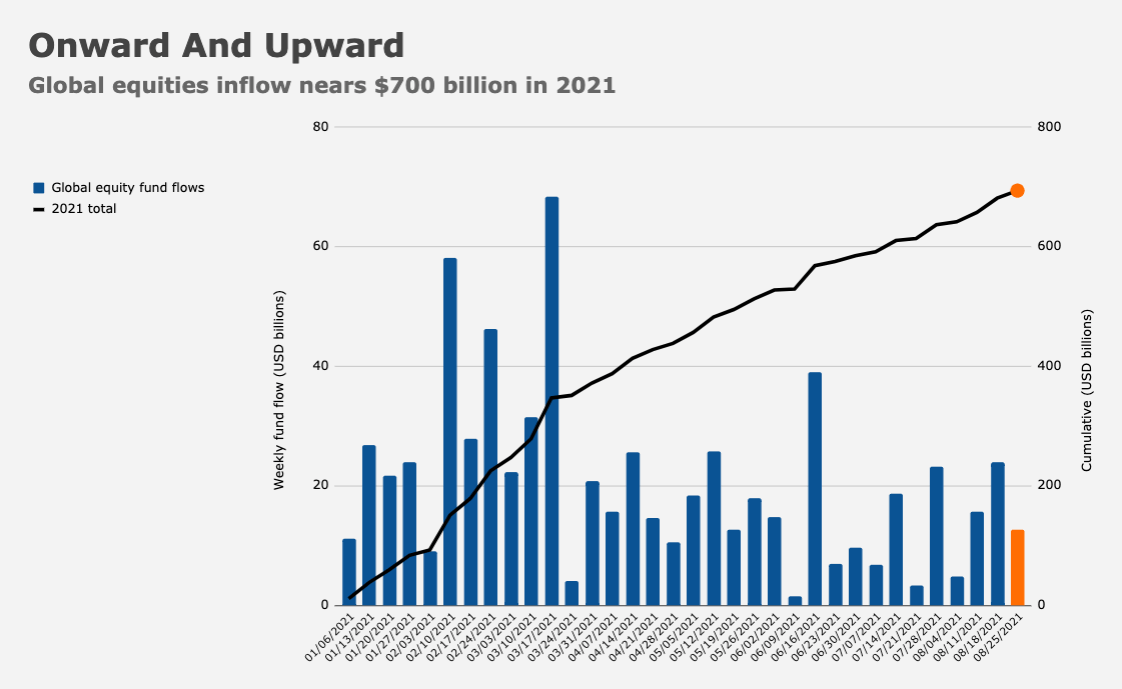

Additionally, there are myriad sources of equity demand to take account of. There hasn’t been a single week of net outflows from global equity funds in 2021 on EPFR’s data. The pace may have slowed, but the annualized figure is quite simply unprecedented (figure below).

There’s ample scope for those flows to continue. On the latest ICI data, there’s still more than $4.5 trillion parked idle in money market funds. If inflation remains elevated, investors would be far better off storing that money in physical form. And no, I’m not kidding. Look at money market fund rates. Now subtract inflation. Tell me it wouldn’t be less punitive to pay whatever cost is associated with storing physical bank notes securely somewhere. Some of that money has to find its way into equities.

At the same time, buybacks are picking up and should accelerate further as corporates ponder what to do with full coffers they no longer need now that the world isn’t ending — or at least now that the apocalypse is on hold.

Finally, you might fairly argue that any rise in real yields associated with even the appearance of Fed tightening conjures memories of 2018, when we learned that in today’s world, equities can’t stomach a rise in real rates even to the “lofty” heights of 1% (figure below).

While acknowledging stocks’ tolerance for higher reals is almost surely lower now, 10-year reals are just ~10bps “above” record lows, with the scare quotes there to denote that we’re still deep in negative territory (figure above). TINA is alive and well.

Ultimately, it’s hard to argue that the impediments to further gains in equities outweigh the bull case, notwithstanding concerns about the Delta variant.

Still, I’d be remiss not to note that if someone at a bar were to slide you a napkin and a pen and ask you to sketch a picture of an asset bubble, you’d probably draw something that looked like the black line in the figure above.

{kind=link}

I still believe that in my lifetime, the US will have socialized medicine, UBI, 35 hour work week, screens/robots replacing entry level workers, significant decline in birth rate. Intelligent immigration policy.

None of these potential big changes have been “factored in”. Many are deflationary.

I also am a believer that we aren’t going back to the way things “used to be”. That doesn’t happen in real life, either.

You’re an optimist… or very young?

IDK, it seems dystopia where those technological advances bungle our social structures into a version of cyberpunk seems more likely? People believe too much in the “just world hypothesis”/are just too conservative to allow for so much hope…

The ultimate long term forecast that I use for planning purposes is contained in the book “2052” by Jorgen Randers. I will probably live long enough to see much of it play out. The powers that be will attempt to maintain the status quo as long as they can but that may necessitate the continuation of even more dovish Fed policies indefinitely.

The calendar is on the list of concerns.

September and October are fraught months for the Farmers Almanac approach to investing.

I’ve always thought there is a reason for that.

Consensus estimates for the year, like newborn babies, start out full of promise and hope: everyone can grow up to be President.

1Q does little to darken any outlooks, the child is just a late bloomer and any shortfall will certainly be made up in being 2-4Q. 2Q sees mothers increasingly anxious, as Johnny’s lagging development is harder to ignore, but he’s a good boy and his worth and enticing price-to-book will surely be recognized soon.

By 3Q, the 45 year old underperformer is still living at home, playing video games in underwear, missing consensus estimates and replacing his CFO. As parents and traders wail, “where did we go wrong” and “someone give me a bid”, middle age ne’er do wells get booted from the basement and the holdings list. If they pre-announce, in September; else, in October.

Then in 4Q, as proud moms glory in their kids who grabbed the brass ring of success, the rest of us, our sad looking portfolios needing quick gussying up, scramble to bid for the defenestrated Johnnies who might in fact be late bloomers, and others trawl through alleys of worn out failures, scooping up meat for the New Year.

In the peculiar world that is the market, stocks only have a one year lifespan but are reborn every January 1, mayflies on repeat, and expectant investors’ hopes spring anew with the start of each new year’s expectations cycle.

TL:DR watch out for the next two months.

Errata: strike “being” and insert “institutional” before “market”.

nice comment!

Poetic but I think this year, estimates and realised earnings offer a more pleasant tale? Or am I just too much in my own (tech) stocks?

Delta, inflation, labor and spending are risks for non-tech earnings. Expectations are a risk for tech earnings. Economic growth forecasts for 2H are being downgraded.

Fair enough. Some expectations are indeed high, though tech stocks have usually delivered.

I find this idea seems fairly consensus. Taper announcement is coming probably Nov although Sept cannot be totally ruled, out, and personally I am more in the Sept camp, albeit it seems less likely than Nov according to post JH consensus. The second thought is that it won’t matter cause markets have been talked to death about. The thrid thought is that if it triggered a 10 or 15 percent downturn in US equities that suddenly the Fed would back away. I do not agree with either of these last two points–when the Fed shifts policy, even when it is well known, they create market upset. Moreover, it would be such a bad look if they hyperventilated over a sudden drop in equities. They may do that but generally, once the Fed starts to go down a path they continue for a while, the one exception being Dec 2015. It would be surprising to grant the market this power. Sure it may happen and it strikes me that there are many who believe that such a modest decline in equities would cause a 180 by the Fed. I am doubtful on this.

What about Q4 2018 then?