Larry Summers thinks Jerome Powell might have it all wrong.

Well, not all of it. But a lot of it. Maybe.

Summers, you’re reminded, is a card-carrying member of the gig economy now. As a paid contributor to Bloomberg Television, Summers gets a check to show up every so often on the network’s “Wall Street Week” program, where he complains about monetary and fiscal policy to an attentive mannequin called “David.”

In essence, Summers’s shtick entails doing a Homer Simpson impression: “Boy, everyone is stupid except me.”

This week, he (Larry, not Homer) weighed in on Powell’s Jackson Hole address, which wasn’t so much “address” as it was a short recap of the July FOMC minutes with some minor tweaks to account for developments since they were released 10 days ago.

Read more: Powell Says Nothing In Anticlimactic Jackson Hole Speech

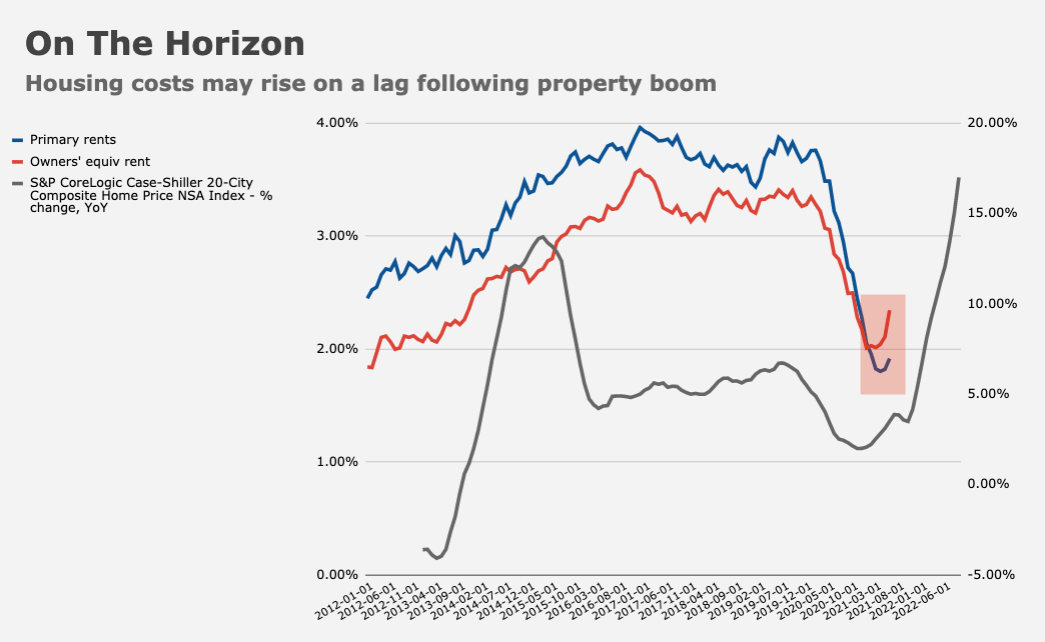

On inflation, Summers reckoned Powell is too “serene.” “He made a whole set of arguments on the serene side,” Summers said. “He may turn out to be correct [but] I was struck that he didn’t say anything about the housing sector,” Larry continued, noting that, based on a statistic he saw (conveniently) on Bloomberg, new renters are paying around 17% more than old renters on average.

“None of that is being reflected in our price indices and yet, on any common sense definition, that’s surely inflation,” Larry added.

He’s right. And many expect it’s just a matter of time before some of the dynamics associated with the surge in house prices are reflected in various measures of inflation (familiar figure below).

Summers continued. “My guess is you’ll start to see the housing component of inflation show up [and] rise pretty rapidly or if you don’t, it’ll reflect defects in the way we create price indices,” he said. He’s right again.

The problem I have with Larry — and I’ve mentioned this countless times since he started an exciting new career as an on-air curmudgeon — is simply that he has better things to do than sneer at everybody who’s trying to help. God knows Larry has the keys to every door one might need to open in order to actually impact policy, and his iPhone contact list is doubtlessly just a who’s who of America’s policymaking elite, past and present.

He certainly doesn’t need the money, so the fact that this notoriously arrogant fixture of “the establishment” decided to demand Bloomberg pay him for the privilege of bi-weekly Zoom calls, is even more odious (to me anyway) than Janet Yellen cashing huge checks for speaking engagements between stints at the highest levels of the US government.

Whatever the case, Summers went on to suggest Powell might be wrong on the other side of the mandate too. Citing labor market frictions (e.g., record job openings and turnover), Larry said “we’re having far more structural change in the economy as businesses rethink their business model, as people rethink their lives after a year without commuting [and] as the whole structure of the economy changes.”

“You’re likely to see some substantial increase in the level of unemployment that the economy can sustain without excessive inflation,” Summers mused.

Here again, I find myself compelled to say that Larry is probably right. And, as Bloomberg noted in their coverage of their own programming (it must be nice when you can literally create news and then report on it after the fact), this is “a debate that cropped up in the Fed’s July policy meeting, where ‘several’ officials thought the pre-pandemic state of the job market ‘may not be the right benchmark’ to judge when the economy reaches full employment.”

Policymakers may well believe that the unemployment rate can be sustained at even lower levels once the labor market fully heals, while Summers is apparently taking the opposite side of the debate (a different “interpretation of the implications,” as Bloomberg put it), but the point is just that many believe the pandemic altered the way laborers conceptualize of their bargain with employers.

That doesn’t (necessarily) mean everyone, in every sector, will demand more money. But it might well mean that workers in many sectors demand more flexible working arrangements or otherwise rethink what counts as acceptable vis-à-vis terms of employment. After all, corporate America just logged record profits, on record margins, while operating under various virus protocols. Folks like Jamie Dimon insist that a return to full-time office work is somehow a prerequisite if we’re to reestablish pre-pandemic vibrancy and dynamism. Someone forgot to tell JPMorgan’s bottom line, though. You can say the same thing for hundreds of other corporate behemoths.

Of course, remote work (“flexibility”) isn’t an option for some sectors, with leisure and hospitality the most obvious example. In those businesses, the only way to entice workers may well be with higher wages.

Ultimately, then, Summers might be (mostly) right about (most) things. At the same time, though, he seems to have adopted the tried-and-true modus operandi of all “successful” pundits and Monday morning quarterbacks: Whatever it is you’re asked to weigh in on, criticize it and implicitly claim that you could do better if only everything were up to you. Never mind whether, when everything actually was up to you, outcomes were suboptimal.

What a zurullo.

Larry Summers is really smart. But he was in error during the financial crisis. And many of his points as you say are right. But his prescriptions are probably not so great. I thought Jay Powell was a poor choice as Fed chair. But he has improved as he learned his job. The fact that he can admit he may be mistaken and correct course, that is showing some humility goes a long way with me. Monetary policy is an iterative process. You have a fed chairman and board who are now pragmatic and willing to change. It makes all the difference in my book. Right now it looks like they are on the right track. If they need to pull back stimulus faster, I am confident they will. Likewise if events change or facts and circumstances change, they will keep the stimulus going. They will watch data and respond. Cannot ask for more than that.

I certainly hope Powell gets reappointed, as generally expected. He’s been a good combination of bold and cautious. His elevation of inequality alongside employment and inflation as a Fed goal may someday be seen as a turning point. Okay, he’s not as good at obfuscatory oratory as one might hope. But market participants need to develop some thicker skin.

Why should the fed obfuscate? Those in the know could still front run the fed or wag the dog or whatever other saying we can use here.

Obfuscations might serve to further marginalize the smaller players in the market while not actually slamming the door on the dialogue the market has with CB’s.

Obfuscation is useful, if the market never really knows what you’re saying then it’s harder to trade on it. Greenspan et al.

You had me at “attentive mannequin called David”!

We appear to be grinding closer to a serious stagflationary environment with each passing day. Continued Covid-related supply chain disruptions, rising housing costs, and the likelihood of increasing wage pressures will keep inflation buoyant while weighing on corporate profits. Price elasticity will surely be tested. And we cannot rule out the imoact of rising energy costs as current wells deplete while oil & gas companies continue to favor returning cash to shareholders vs increased production.

But this is all clearly a worry for another day as investors squeeze remaining juice out of the market during the remaining days of ultra-accommodative monetary policy.

“Whatever it is you’re asked to weigh in on, criticize it and implicitly claim that you could do better if only everything were up to you. Never mind whether, when everything actually was up to you, outcomes were suboptimal.”

We should add this as an amendment to our Constitution, since it defines the current state of our political/economic environment better than any of the existing text.

I LOVE your writing. To respond in kind, I’ll resist the temptation to blather about inflation or the Fed, and observe that Larry has a particularly severe case of Ray Dalio Syndrome, as evidenced by his tireless efforts to expand the Room in which he is the Smartest Guy.

Summers is really smart, and so are you. Apologies, but I don’t understand the quote: “You’re likely to see some substantial increase in the level of unemployment that the economy can sustain without excessive inflation,” Summers mused. –Aren’t high levels of unemployment deflationary, not inflationary? It would make sense to me if he said “employment” instead of “unemployment.”

I’m a little more forgiving of him personally. If Larry didn’t charge Bloomberg for speaking to him, Bloomberg would have even more money. And he needs it even less than Larry. As smart as he is, Summers will likely never again serve in an important policy role. No Republican will appoint him, and he is also out of favor with the Democratic Party (even though he advised Biden early in the primaries). He does have access to policymakers, but I doubt much influence. So perhaps this is how he thinks his ideas can get attention. On fiscal policy, he has been more specific about what he would do. Earlier in the year I watched him and Paul Krugman debate on stimulus in a Princeton finance event (which is not my school, but I got a zoom link from a friend), where was pretty quantitative about stimulus levels he thought were right. I haven’t heard specifics on monetary policy.

I generally find that when policymakers are in the job of policymaking they are less convincing in their analysis than when they are no longer in the seat. Diet Coke Larry concerns are probably worth paying attention to. In GFC the policy support was something like 0.5% of GDP, this time it was 5% of GDP, and inventory is shifting from “just in time” to “just in case” and lets not forget the housing and financial sector were deleveraging post GFC, and it is completely different this time around. I am completely ready to throw transitory under the bus, but this inflation normalisation is still far trickier this time around and the point on rents is important and you should also remember that pre Covid goods inflation was a huge drag, near 0% for 20-years, thanks to deflationary wind from China, I am guessing it will be closer to 2.0% going forwards. So many disinflationary forces have gone bye-bye.

Yesterday Fortune released an armchair perspective of longer term risk for the economy and the Fed’s management of the money supply, based upon hazards/risks that Summers points out, but in the context of Biden administration borrowing and spending. Here is a link:

https://fortune.com/2021/08/31/us-economy-risk-treasury-low-interest-rates/.

It’s over my head, honestly. But I do fret that this dance with risk can result in falling down if the administration doesn’t abide with the choreography.