The Nasdaq careened towards correction territory Thursday, as Jerome Powell failed to assuage a market that desperately wanted clarity following last week’s bond rout.

That Powell didn’t manage to hit the right notes was both predictable and surprising at the same time.

He isn’t a great communicator, or at least not vis-à-vis markets. And yet, it was abundantly clear what markets wanted to hear. To the extent Powell’s webinar with the Wall Street Journal represented a rhetorical challenge, it wasn’t a particularly daunting test. Simply acknowledging that the Fed’s toolbox includes the option to “twist” and a nod to the unresolved SLR question would have probably sufficed. Alas.

Read more: ‘Feel The Market’ Next Time, Jay

Yields moved higher on Powell’s sin(s) of omission, and that caused more problems for tech.

Globally, tech shares may be teetering on the brink of a bear market, and the Fed Chair didn’t do them any favors on Thursday. The Nasdaq 100 fell near correction territory and the FANG+ gauge is similarly beset. If it’s a dip you’re looking to buy, this probably counts as a “legit” swoon.

Investors’ Classical conditioning (i.e., their Pavlovian tendencies) may kick in, especially with the memory of Monday’s dramatic bounce still fresh. But this is a falling knife. With the reopening narrative, rising oil prices, an accelerated vaccine push, and fresh stimulus all arguing for higher yields, secular growth and bond proxies are a perilous proposition.

Cathie Wood’s flagship fund is now down nearly 25% from its peak last month. Your wings are melting, Icarus.

“This Nasdaq / ‘Secular Growth’ / Expensive Stock pain has now dragged SPX into ‘negative gamma & delta’ territory with it [but] it’s the extreme magnitudes of the current QQQ greeks which make this market so fragile,” Nomura’s Charlie McElligott said Thursday.

Energy shares, meanwhile, managed to gain on an otherwise abysmal day for the broader US market. OPEC+ surprised with a decision to refrain from adding too many barrels to the equation at what the Saudis still clearly believe is a delicate juncture.

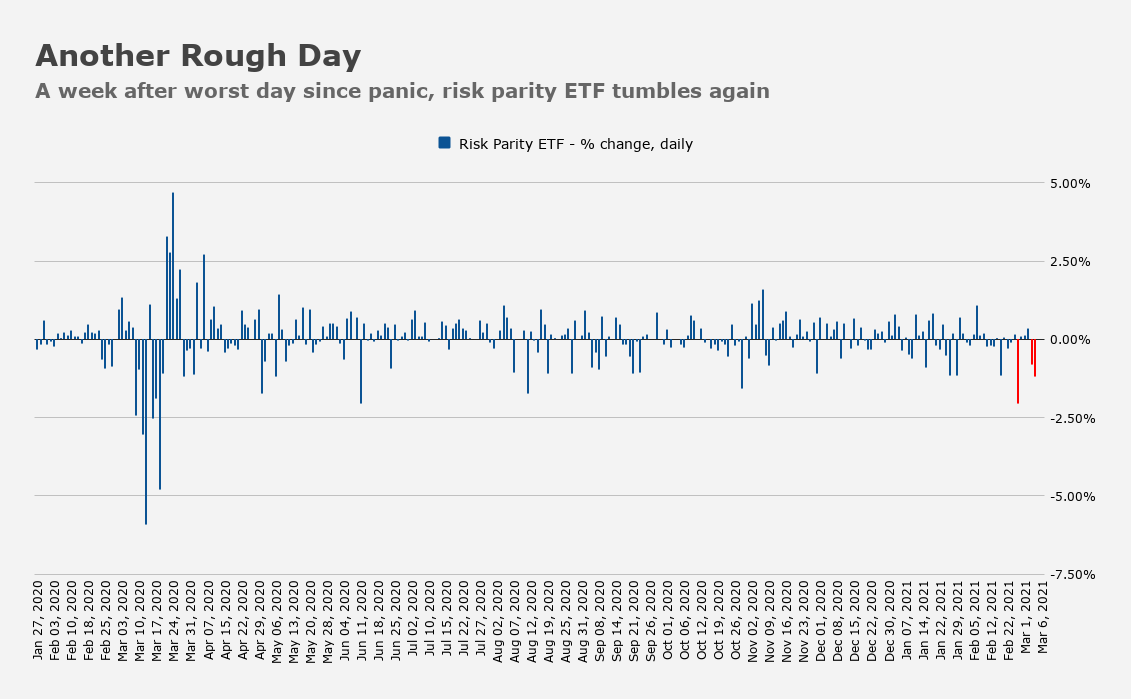

But this is a market that lives and dies by the high-fliers, which means that on days when the Nasdaq is bleeding out, there’s no real “offset,” so to speak. And because the proximate cause of the pain is higher yields, bonds aren’t your hedge. So, “diversification desperation” it is.

10-year yields were higher by ~6bps and hit 1.554% at the highs. Goldman raised its year-end forecast to 1.90%, up 40bps from 1.50%.

“A retracement from record high equity valuations isn’t a negative thing for monetary policymakers, as it releases air from potential asset bubbles,” BMO’s Ian Lyngen and Ben Jeffery said Thursday afternoon.

“One thing is certain, the traditional correlation between stocks and bonds has been set aside for the time being,” they added, noting that while “higher yields were interpreted by equity investors as a ‘positive sign’ for the economic outlook” during the early days of the bond selloff, “the transition to a paradigm in which discount factors outweigh recovery optimism will give policymakers pause.”

Powell’s passive faux pas managed to catalyze a sharp spike in the dollar Thursday, which is just about the last thing you want. The Bloomberg dollar index rose to its highest since December 1.

This dynamic is becoming unsustainable. Until recently, it was wholly plausible (indeed, it was rational) to argue that higher yields reflected economic optimism and that financial conditions weren’t threatened by the backup. At this point, though, with the dollar rising, real yields up 42bps in 2021, and stocks looking increasingly nauseous, it’s becoming more difficult to make that case.

Now, all eyes turn to Friday’s jobs report and the stimulus debate in the Senate.

Dollar dead cat bounce now becoming a leap, along with a FED at ease with letting air out of bubbles. As stated earlier today, inflation probably a temporary concern and not realistic but having an effect.

Not knives I want to catch just yet.

Yeah, the knives!

One of these times, and I hope it’s after I’m dead, the markets won’t recover, and they’ll just keep going down…kind of like the months, and years, following the 1929 event.

All said, we had the liquidity event already (last March). So, whatever happens next, it won’t be another one of these.

Speaking of diversification desperation, where does this leave VaR?

Yes!! Great question, we need an update about Mr. McElligott line of thinking given the moves the last two or three days and what’s next.

No ‘dis on H as he (she?) provides much abundance on these topics…nonetheless.

I rather admire Powell and his occasional attempts at straight talk..How his comments are interpreted becomes an issue of ideology and what we desire to happen .The Fed is an appointed position but should not be so highly political to as to be required to feed the baby crying in the back room .That task is left to the realm of Politicians . The Horizon is clearer now than it has been for a while so selling gold and buying Banks and oil and commodity stocks was a good idea about last week… Geopolitics and generally logical Economic consequences may yet prevail temporarily.

Indeed, first the markets pulled forward good economic news and now bond investors have brought inflation expectations forward.

What’s left??

When do we start to pull forward the impact of the inevitable economic slowdown once the travel/leisure sugar rush runs its course? That is the last bit of unsatiated pent up demand.

There is little unsatiated retail demand left and housing-related spending is bound to slow as higher rates price out many buyers and Covid-panic buying subsides.

As George hints at, maybe it’s time to say “thank you” and reduce your financials and miners. (The comments out of China last night might be another warning signal when it comes to commods?)

It brings to mind something worth remembering — MOST longer-term investors cannot sell bonds and stocks and sit in cash. That has turned out to be a career-ending move over the past 50 years.

“MOST longer-term investors cannot sell bonds and stocks and sit in cash. That has turned out to be a career-ending move over the past 50 years….”

Just to be clear, you’re talking about people who run other people’s money for a living, right? Seems to me that cash is the only option for older retail investors at this juncture — those nearing retirement age and focused on capital preservation. (Lot of boomers who fall into that category.)

Yes mfn. In the context of those who quickly move large sums of money, large enough to impact the markets.

I’m probably in your age group so get what you are speaking of.