For a few hours in Asia, it looked like selling pressure inherited from Wall Street was poised to accelerate a global equity rout.

Ultimately, things calmed down, and regional shares pared losses, but the consternation was palpable.

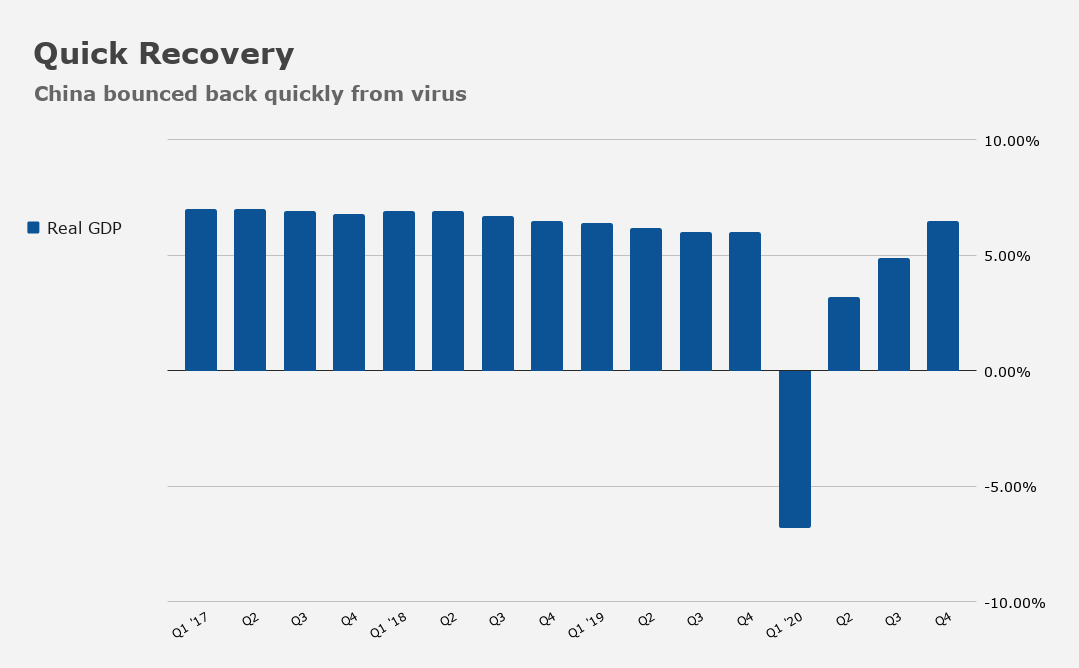

China set a growth target of more than 6% for this year, a bar which, if you go by consensus expectations, should be easy for Beijing to clear. Economists generally see the world’s second-largest economy expanding at around 8% in 2021, coming off an anomalous year during which the country was hobbled by the pandemic, forcing Beijing to temporarily scrap the target. Still, China held up far better than western economies as COVID rampaged across the globe, killing millions and decimating livelihoods.

“A target of over 6% will enable all of us to devote full energy to promoting reform, innovation, and high-quality development,” Premier Li Keqiang said Friday. The budget deficit will shrink to 3.2% of GDP.

Local companies involved in semis and tech manufacturing benefited from officials’ vow to increase spending on chips and AI as part of the new five-year plan. Li described a desire to achieve “major breakthroughs in core technologies” funded by a better than 7% increase in national R&D outlays. “Innovation remains at the heart of China’s modernization drive,” Li remarked.

This comes as China is rapidly moving to cut its dependence on western technology after Donald Trump’s trade war morphed into a bitter tech battle, underscoring the perils of relying on foreign competitors for critical components. Trump’s initial obsession with erasing a bilateral trade deficit and restoring American manufacturing (he achieved neither) eventually gave way to an almost singular focus on tech, which the former occupant of the Oval Office belatedly came to realize is far more important (from a strategic perspective) than any quixotic attempt to revive a handful of steel mills.

China also plans to deal Hong Kong’s pro-democratic opposition further legislative blows going forward, but that’s another story. Democratic activist and political scientist Joseph Cheng captured the gist of it in remarks to Bloomberg. “The Chinese authorities have reached the limit of their patience, and they’ll no longer accept an effective pro-democracy movement [or] any serious checks and balances,” he said.

Mainland equities initially dove as officials sketched out China’s future, but by the end of the session, the losses were modest. For the week, the CSI 300 logged a 1.4% decline, the third consecutive weekly loss.

In Hong Kong, shares managed a weekly gain, but the tech index fell another 2% on the heels of the Nasdaq’s Thursday bludgeoning.

The Hang Seng Tech Index is at the forefront of the global tech selloff, with losses since February 17 at least twice as steep as declines seen in US tech and a broader regional gauge of tech stocks.

“All razzmatazz aside, China, just like the US, is struggling with its own internal and external contradictions, in its case between the planned and the market sides of its economy, and between productive (not loss-making) investment and bubbles,” Rabobank’s Michael Every said Friday.

“The key issue is if we see further such high targets for following years, given the underlying growth rate may be no higher than 2-3% at best, with the balance being over-supply shipped out to global markets, or residential properties sitting empty,” he went on to say, referencing China’s growth goals and adding that “the higher the targets are, the more inflationary –and distortionary– for China and the world, just as the Fed is de facto doing the same thing [even as] neither side seems to be paying much attention to the other.”