Jerome Powell’s webinar with The Wall Street Journal didn’t go well.

Or at least not if you define “well” by reference to the market reaction.

That Powell “failed” to pacify the market was hardly surprising. His cadence and demeanor are not amenable to a job that has, over the years, become heavily dependent on the use of academic doublespeak to placate investors and traders. “Plain English,” as Powell famously dubbed his approach, was doomed from the beginning to result in episodic bouts of volatility, with the fourth quarter of 2018 being the quintessential example.

Ironically, the crisis spared Powell the trouble of having to master the art of obfuscation. Starting in March of 2020, there was no need for nuance. The Fed would do anything necessary to keep the universe from imploding. It’s pretty hard to bungle the message when the message is just “We’ll do whatever it takes — and then some.”

But as soon as the situation called for nuance (so, starting with last week’s rates tantrum), Powell’s “plain English” was destined to become a liability again.

The market was looking for several things out of Powell during Thursday’s chat with the Journal, and he arguably didn’t deliver on any of them. On Wednesday afternoon, I gently reminded folks that,

… he usually sticks assiduously to the script. Even if he does attempt to placate a nervous market, it’s hard to imagine he’d do so in emphatic/dramatic fashion.

Sure enough, Powell was repetitive. Too repetitive. The market knows the Fed intends to be “patient.” The market knows the Fed is hyper-focused on the labor market. The market knows that the Fed will be predisposed to viewing inflation pressures as either transitory phenomena or else as a welcome development on the way to the kind of “benign” overshoot that’s now enshrined into policy via average inflation targeting.

What the market doesn’t know is when (or even if) the Fed intends to extend the maturity profile of its holdings. The market also didn’t know, as of Thursday, whether the Fed intended to extend SLR relief, and had no clarity on whether officials had recently discussed options (e.g., a new “twist”) to help alleviate obvious points of stress in the bond market.

It’s true that nobody expected Powell to address those issues in a definitive way. After all, his colleagues gave no indication that any such overt communication was forthcoming, and the idea is probably just to hope the situation “resolves” by the March FOMC.

And yet, the market needed something from Powell, even if it wasn’t much. He was either unable (or unwilling) to oblige.

“Treasurys simply cannot hold a meaningful bid despite [Wednesday’s] modest data disappointments and shaky risk sentiment,” Nomura’s Charlie McElligott said, ahead of Powell’s Thursday remarks. “If Powell were to shock us with language that spoke to enhanced willingness or reinforcement of policy flexibility with QE purchases or, separately, spoke to SLR exemption extension, a bullish UST response could get squeezy fast,” he added.

Charlie’s use of the word “shock” was indicative of the extent to which the market wasn’t expecting much. But Powell arguably didn’t give the market anything at all, other than a reiteration of the same talking points he’s leaned on for weeks.

He did say that last week’s volatility in rates “caught my attention,” but that came across as a rather odd way of describing his interest in a market he effectively controls. That is: One certainly hopes it “caught his attention.” What would the alternative be? “I didn’t even notice. Tell me more” maybe?

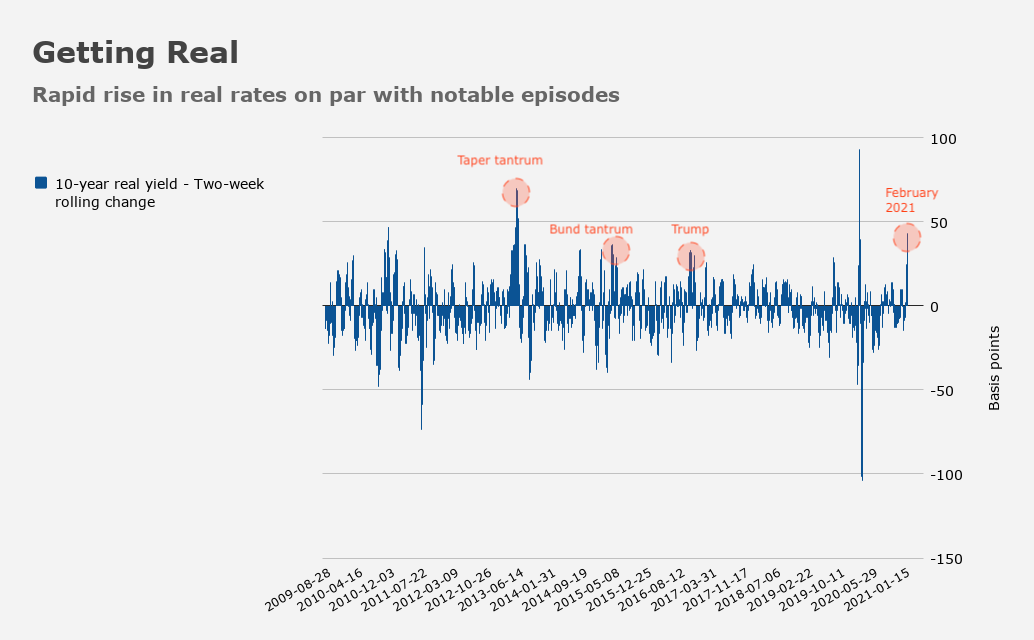

Powell was speaking specifically to the rise in real yields. He also said the Fed would “use its tools” if conditions changed and it was necessary to address some threat to the achievement of the Committee’s goals.

That simply wasn’t good enough for market participants. It suggested last week’s sharp rise in real yields (figure below) wasn’t deemed “material” or, at the least, wasn’t seen as a serious threat to financial conditions.

While that’s probably accurate, it came across as tone deaf, at best. At worst, it was seen as insufficiently attentive to an angry child (i.e., the market), who, absent proper attention, might just persist in a state of tantrum. Indeed, the 5s30s steepened to session wides as Powell spoke. He insisted that current policy is appropriate.

Again, it’s not just the rise in rates that’s at issue. It’s illiquidity at the long-end, too much cash chasing too little collateral at the short-end, and an unresolved regulatory issue that demands attention sooner rather than later.

Some will probably applaud Powell for standing up to a market that pretty clearly wants to push officials in the direction of providing additional succor.

The problem, though, is that he needn’t have promised anything or mentioned any specifics. It wouldn’t have been terribly difficult to nod at WAM extension or acknowledge that there are risks on both sides of the SLR extension debate and that the Fed would be prepared to address and/or offset any adverse reaction to a “disappointing” decision.

When he demurred, Treasurys sold off, triggering a fairly acute slide in equities and, tellingly, a spike in the dollar.

You can draw your own conclusions, but there were myriad headlines on Thursday afternoon drawing attention to the fallout from Powell’s apparent flop. Examples included: “Powell Signals Fed Is Reactive Rather Than Proactive,” “Treasuries Fly Flips Positive as Wave of Steepener Demand Rises,” “S&P 500’s Breach of Key Technical Levels Presages Further Losses,” and “Latam Currencies Drop as U.S. Treasuries, Stocks Slump on Powell.”

He clearly didn’t “feel the market,” as a former president once put it.

Maybe the Treasury Secretary has some thoughts she’d like to share with the market during the Fed’s quiet period. I hear she’s got a knack for such things.

Even before reading anything about Powell’s remarks, I knew the gist from the early afternoon market reaction.

One would have thought that by now Powell would have developed a better sense for calming markets. His continuing lack of subtlety is in a position where nuance is frequently important is something of a concern.

It is hard for me to see this as anything other than an opportunity for anyone who wants to move some of their retirement account from bonds to equities.

The answer to the question relating to monetary policy and the causes of inequality made even me cringe.

If I’m the Fed chair and I’m seeing the bubble stocks implode but indices cushioned considerably by resurgent cyclicals I’m feeling pretty good….. nervous of course, but aware that there are far worse alternatives (TAFWA).

How far does the S&P 500 need to drop until the central bank thinks financial conditions are tightening? I’d say it’s another 20% lower.