Coming into Thursday, it was clear that rates were going to be the story.

Of course, rising yields have been the story for weeks now, but fireworks in Kiwi and Aussie bonds set the stage for similar dramatics stateside, and Treasurys didn’t disappoint.

It’s probably fair to say that Thursday will go down as one of the more memorable sessions of 2021 for US rates, and especially for intermediates. Five-year yields screamed higher, in an eye-popping move worthy of all the digital ink spilled documenting it.

On Wednesday afternoon, I “dared” to mention 1.50% on 10s. We got there, and beyond, less than 24 hours later. The peak was 1.6085%. It was a big move (figure below).

I suppose we’re still sticking with the “higher yields are indicative of improving economic expectations” narrative, and indeed, the data on Thursday was encouraging. But stocks are clearly getting a bit wary of the surge.

Just about the last thing bonds needed amid the worsening rout was a horrendous seven-year sale, but when it rains it pours.

“Failed” is never quite the right word when it comes to Treasury auctions, but the 4.2bps tail was pretty big. In fact, it was the largest ever. One commentator called the sale “unimaginable.” The bid/cover, 2.04, was the lowest in at least 11 years. Non-dealer bidding of 60.2% compared to an average of 79.6%. The dealer takedown was almost three standard deviations above average. Five- and seven-year yields leapt to fresh day highs following the debacle, as rates traders cited stop-outs and position squeezes in curve plays, according to Bloomberg’s sources.

It was an all around bloodbath for bonds. There’s no way to sugarcoat it. Five- and seven-year yields were cheaper by more than 20bps.

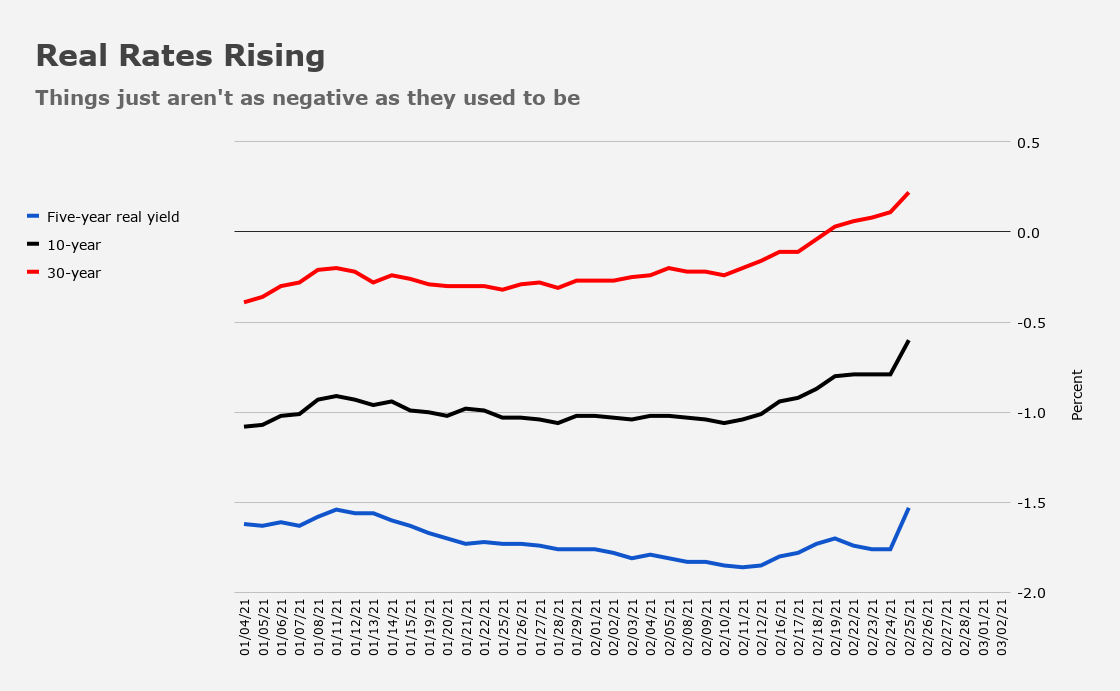

When US traders woke up Thursday, it was a big deal that 10-year reals were back to -0.74%, as that was the “highest” (i.e., least negative) since the onset of the pandemic. By the end of the day, they were just -0.60%. At the long-end, reals are +22bps, up from -4bps just days ago.

If you thought TLT was oversold before, it’s even more so now (figure below). As I put it Wednesday afternoon, “for any brave home gamers looking to catch a falling bond knife, this is your chance to get a finger sliced off.” The ETF has fallen in nine of the past 10 sessions. It’s down 9% this month alone.

There were myriad signs that the market is starting to reprice the Fed. “The market is currently pricing in… some combination that results in the transition which took 31 months last cycle to be truncated with a year,” BMO’s Ian Lyngen and Ben Jeffery wrote Thursday, referencing the eventual path to both a taper and liftoff.

“Certainly, it could happen – but that would imply something has changed dramatically in the Fed’s interpretation of the balance of risks surrounding the inflation outlook,” they added.

Stocks were not amused. Tech, which is in focus due to the vulnerability of secular growth favorites to higher yields, plunged. The FANG+ gauge dropped more than 3%.

It can’t be emphasized enough: High-flying tech names and other equities expressions tethered to the yearslong “duration infatuation” in rates are in the firing line right now. Anything that’s benefited from years of “slow-flation,” falling yields, and a bull flattening curve, is in peril.

Tesla and the ARK Innovation ETF were bludgeoned. Cathie Wood is staring down a daunting environment after a meteoric rise predicated on big bets tied to trendy investment themes that are in some way, shape, or form supposed to be in step with the evolution of technology and humanity more generally.

This is the third serious tech selloff since the pandemic catapulted growth shares into the stratosphere. The others were in late October and, of course, early September, when the summer tech frenzy finally tipped over.

On imagines the selloff in bonds will take a breather after Thursday. If it doesn’t, Fedspeak will likely begin to skew towards a message that any undue tightening in financial conditions as a result of rate rise isn’t welcome. Remember: At the end of the day, bond yields are just a policy variable. And yet, as the RBA is learning, the market can sometimes lose track of that, even in the face of central bank asset purchases. Maybe a more forceful reminder is in order.

Until Jerome Powell whispers “QE 7,” cash looks pretty good to me.

I’m ready to risk my fingers catching a falling knife, bought TLT calls, but I’ll admit it feels awful risky, like buying bitcoin…

Yeah, risky. On a long enough timeframe, Treasuries can go to zero, too.

I’m with you Evil Twin. But sure would be nice to catch that negative convexity train steaming the OTHER direction for a day or two. Hopefully J-Pow is in the telephone booth getting his Superman costume on!

The following quote is from CME Group, Dec 29, 2020, posted as Fed Balance Sheet:

“The Fed desk began its operations with an immediate purchase of $40 billion in nominal coupon securities and Treasury Inflation-Protected Securities (TIPS). In further action related to the coronavirus pandemic, the Fed announced on March 23, 2020 that its purchases of Treasury securities will be in amounts “as needed” to promote a swift recovery.”

I ran across that story last week, because I was curious about the massive amount of inflation jawboning related to inflation.

I was also looking at FRED: https://fred.stlouisfed.org/graph/?g=Bpgx

It sort struck me that this is like the scene in It’s a Wonderful Life:

“Can’t you understand what’s happening here? Don’t you see what’s happening? Potter isn’t selling. Potter’s buying! And why? Because we’re panicky and he’s not. That’s why. He’s picking up some bargains. Now, we can get through this thing all right. We’ve got to stick together, though. We’ve got to have faith in each other.”