Meanwhile, from the “why not?” files.

On a day when Tesla disclosed a $1.5 billion balance sheet “flier” on Bitcoin, RBC’s Mitch Steves upped his price target on Apple to $171 from $154.

Those two things might not sound like they’re related — and they aren’t — but there’s an amusing tie-in.

Over the past couple of weeks, the volume of the perpetual background chatter around a possible push by Apple into the electric vehicle market increased materially. And while RBC thinks an EV adventure “could be a long-term opportunity” for Apple, they caution that “competing with Elon Musk and Tesla is a higher risk proposition” compared to utilizing the company’s existing install base.

What does that mean? Well, I’m glad you asked. For RBC it means that the better near-term opportunity might be leveraging Apple Wallet in the crypto realm — specifically to create an exchange.

“If the firm decides to enter the crypto exchange business we think [Apple] could immediately gain market share and disrupt the industry while simultaneously making the USA a leader in crypto for the next 10-20 years,” RBC said, before putting some math to this ostensible madness, as follows:

Square generates ~$1.6B/qtr in Bitcoin related revenue on an active install base that we estimate to be in the ~30M range. Apple’s install base is 1.5B and even if we assume only 200M users would transact, this is 6.66x larger than Square. Therefore, the potential revenue opportunity would be in excess of $40B/year.

That, RBC went on to note, would represent a “15% incremental top-line opportunity.” Apple is, of course, coming off its first $100 billion quarter.

One selling point is what they describe as “the removal of friction.” Apple, RBC said, could make it easier for individuals to acquire crypto assets by “offer[ing] a closed system which prevents nefarious activity, improves security of the assets, and [provides] instant access to the buyer/seller.”

The bank imagines this would all be extremely simple. I don’t mean to come across as pejorative by using the word “imagines.” Far be it from me (sincerely) to question tech analysts’ assessment of how easy it would be for Apple to tap into this prospective “opportunity.” But I’ll be forgiven for suggesting that perhaps it would be at least a bit more difficult than RBC suggests. They described it as something akin to flipping a switch. “The firm could unlock a multi-billion dollar opportunity with a few clicks,” the note reads.

Forgive me, but it’s never (ever) the case that a company can simply conjure a reliable 15% increase in revenue “with a few clicks.” No sane CEO would forgo such an opportunity. And maybe that’s RBC’s point. My point, though, is that quite a few folks seem to be underestimating the headaches that would accrue to the C-suite at blue chip companies from wading into the crypto business.

There are myriad reasons why this isn’t a no-brainer for companies with the resources. It’s not that everyone is a “hater,” as crypto proponents are fond of suggesting. Rather, it’s that this is risky. And part of running giant multinationals is risk management. There are regulatory issues, accounting issues, and just generalized angst from tying the fate of your company and shareholders to something as volatile as Bitcoin. I’m reminded of the exchange between Pablo Escobar and George Jung from the film “Blow”:

These complications with Diego… it’s causing me much inconvenience. And I don’t like problems.

Cinema jokes aside, and “problems” notwithstanding, I’ll admit this thesis of RBC’s makes infinitely more sense (at least to me) than simply buying Bitcoin for the balance sheet for the sheer sake of it, like Tesla appeared to do.

Speaking of that, Steves also suggested that one good way to jumpstart participation in a nascent Apple crypto exchange would be for the company to buy a billion worth of it themselves. This is one case where it’s impossible to argue the company “can’t afford it.”

“While less relevant, if the firm were to acquire ~$1 billion in Bitcoin for their balance sheet we think this would send even more users to ‘Apple Exchange,'” RBC remarked, adding that such an investment would amount to just ~4 days of cash flow.

“Where would the price of Bitcoin go if Apple purchased the asset?,” they went on to ask.

It was a rhetorical question.

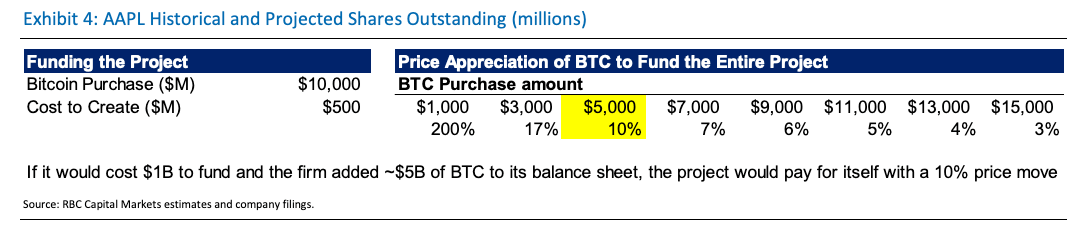

If the cost of development were, say, $500 million, RBC suggested Apple could “synthetically pay for the development cost by acquiring the underlying asset.” As the following table shows, if Apple bought $5 billion of Bitcoin, it would only need to rise 10% to, and I’m quoting RBC here, exclamation point included, “fully fund the entire project in the first place!”

Make of this what you will.

I’ll respectfully refrain from further editorializing, other than to say that if Apple were to do something like this, it could change the dynamics materially. Early Monday, I wrote that regulators are unlikely to consider Tesla’s balance sheet health when making decisions about the crypto universe. By contrast, if Apple were to launch an exchange and tie up its fate with Bitcoin, regulators in the US would likely think twice before making any draconian decisions.

Outstanding! This starts to look like a trip from the Sixties. Thanks for the mood lightener for today.

If Apple actually does this… I’m a little lost for words. Regulators need to send a message ASAP that it will be banned and introduce a bill. The fact this discussion continues shows that Washington does not understand what is happening, and will likely miss the opportunity. That was my last holdout honestly.

Big revenue jump. But why didn’t he extrapolate the SQ profit from the exchange rather than just the revenue?

Never mind, what a silly question.

AS Fed rates remain stuck near zero, with little hope of going anywhere this year (or decade) maybe it makes sense to hedge bets with crypto and take advantage of the evolution of Capitalism. The general disconnect from reality during the last few years has opened up Pandora’s Box of magical digital experiments, so the idea of Apple opening a digital wallet sandbox seems fairly tame.

Meanwhile:

Zoltan Pozsar

8 February 2021

We begin our analysis with the observation that the long, three-year period of front-end collateral glut – which lasted from early 2018 to last week – is over. Treasury bill yields no longer push o/n rates up within the Fed’s target range, and after three years of “irrelevance,” the o/n RRP facility, not Treasury bills, is the true floor to the o/n tri-party repo rate. Broadly speaking, these rates collapsed to zero last week; however, the effective fed funds rate (EFFR) hasn’t.

https://plus.credit-suisse.com/rpc4/ravDocView?docid=V7pAR92AN-VHSK

I noticed a headline today how Miami city officials are considering adding bitcoin to the municipality’s investments.

It also happens that I just started reading McKay’s 1841 book “Popular Delusions and the Madness of Crowds.”

Mixing state finances with speculative monopoly or private schemes has a long history. If only John Law, Ivar Kreuger and the directors of the South Sea Company could aid in these plans we could reach complete ruin even faster.

Reminds me of Orange County, but that’ll never happen again, because now, people have smart phones …

From Wiki: “Citron controlled several Orange County funds including the General Fund, the Investment Pool, and the treasury Commingled Pool. He sent out the county’s tax bills with catchy slogans, such as “Taxes paid on time never draw fines.”[6] He won re-election seven times; in his last election victory, his opponent, John Moorlach, charged that his handsome gains were the result of risky betting.[6]

As controller of the various Orange County funds, Citron had taken a highly leveraged position using repurchase agreements (repos) and floating rate notes (FRNs). The loss incurred by the use of these financial instruments reached the amount of $2 billion and was caused by being too highly leveraged for rising federal interest rates.[6] In other words, if federal interest rates had not risen, the massive trading position would have been a substantially profitable position; if interest rates did rise, the trading position would result in substantial losses. In fact, rates rose.

The Orange County funds, managed by Citron, were worth $8 billion.[6] However, Citron went out to the repo market and leveraged the County Pools to amounts ranging from 158% to over 292%. To obtain this degree of leverage, he used treasury bonds as collateral. Profits of the fund were excessive for a period of time and Citron resorted to concealing the excess earnings. He pleaded guilty to improperly transferring securities from the Orange County General Fund to the Orange County Treasury Commingled Pool.”

I thought there was a set limit of Bitcoins? If the acceptance and use of Bitcoins increases doesn’t the number of Bitcoins also have to increase or do you divide the set number of Bitcoins into smaller and smaller fractions of Bitcoins? I don’t see how, at any point, offering to pay for something in fractions of a Bitcoin is ever going to work.

Set limit of 21 million (not counting forks), each can be divided into 100,000,000 parts. The smallest unit being a ‘Satoshi’, or .00000001 bitcoin. The payments probably won’t ever work, for a variety of reasons.

Having seen my share of large notional gains and losses during the ’17 run, I remain amazed at what the last month has brought. Absolutely rampant speculation, across nearly every altcoin project. And yet, as someone who dumped half their btc at ~33 and knows this run is divorced from reality, even I am starting to feel my share of regret and fomo. If companies continue to buy, even stodgy retail types will have to hold their nose and follow. Whatever the end is for bitcoin, the current bull run has some serious legs. Bill Miller is right. The upside is just too great. And we are all too greedy.