Well, the US manufacturing sector is apparently on fire — in a good way, with the caveat that inflationary pressures continue to build.

December’s ISM print, 60.7, was a scorcher. Consensus was looking for “just” 56.8, which would have been solid enough.

The range of estimates was 54 to 58.5, so the actual read came in well above even the most optimistic guess from nearly five-dozen economists.

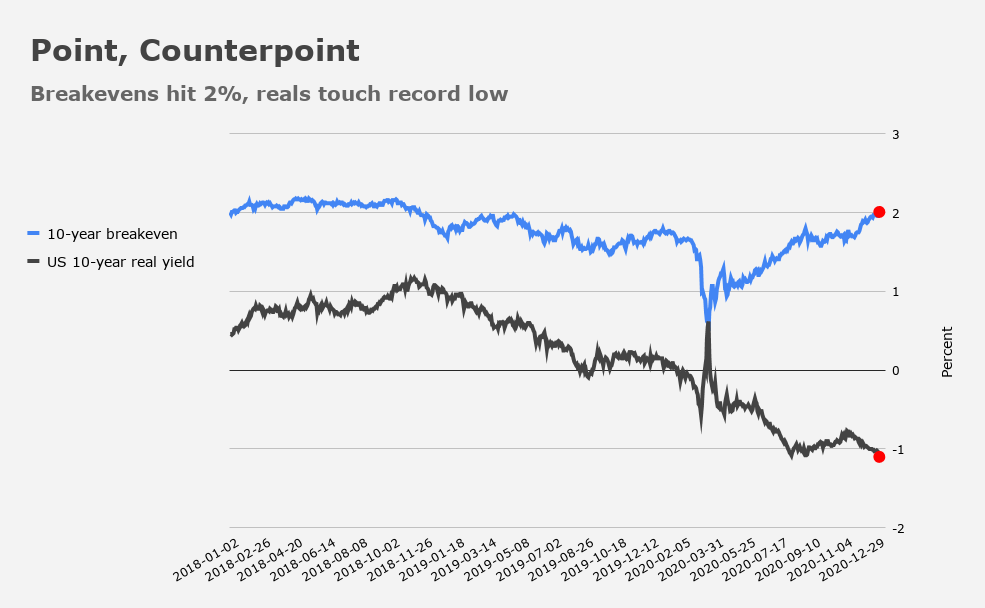

As the subheader in the figure (above) notes, December’s headline print is the highest in more than two years.

Essentially every underlying gauge rose, with the exception of new export orders and imports. Production hit the highest since 2011. At 67.9, the new orders index was the strongest in 16 years.

Employment ticked back into expansion territory, which is good news.

You’ll note prices paid rose to 77.6. That’s the highest since May of 2018 and it partly reflects the inflationary impact of supply chain bottlenecks. “Bottlenecks” is usually just a euphemism for “disruptions,” and there’s no shortage of those in the pandemic era.

Every industry reported paying higher prices last month.

That’s consistent with the message from IHS Markit. “Although supported by further substantial increases in output and new orders, the headline [PMI] was pushed higher by severe supply chain disruption,” the color that accompanied the final read on Markit’s own manufacturing gauge for the US read. “The rise in input prices was substantial and the fastest since April 2018, driven by raw material shortages and supplier price hikes,” the same Monday release went on to note. “Firms were able to partially pass on higher costs, however, as selling prices increased at the sharpest rate since May 2011.”

ISM delivered similar commentary Tuesday. “Aluminum, copper, steel, petroleum-based products including plastics, transportation costs, electronic components, corrugate, temporary labor, wood and lumber products all continued to record price increases,” Timothy Fiore, chair of the survey committee, remarked.

If you’re curious, consensus was looking for a 66 print on ISM prices paid. So, that 77.6 read is a near 12-handle upside surprise. This comes just a day after breakevens hit 2% in the US for the first time since 2018.

There are plenty of obvious jokes here, and Bloomberg’s Cameron Crise, apparently feeling chipper after the holiday break, didn’t waste the opportunity. “Amusingly, Loretta Mester was on the tape at the same time saying that more accommodation might be needed to reach 2% inflation,” he quipped. “Are we fighting the last war?”

Maybe. But before anyone gets ahead of themselves based a few months’ worth of PMIs, allow me to remind you that the world just experienced the biggest deflationary supernova since the Great Depression.

While it’s true that the unique nature of the crisis raised questions about possible inflationary side effects (e.g., supply chain disruptions and re-shoring), output gaps and labor market slack won’t disappear overnight.

Additionally, it’s worth noting that just because your input prices are rising doesn’t mean you can simply raise prices all the way down the line. At some point, you’ll meet the end consumer.

And the end consumer is, colloquially speaking, broke as hell, and quite possibly jobless. So, you can try to “pass along” higher costs if you like, but that doesn’t mean they’ll pay it.

Now here we are pondering stagflation again.

Bummer.

Hence the FED being flexible about inflation targets.