There’s desperation in the air in Riyadh.

A week on from warning that the country will be forced to take “painful” adjustment measures to cope with the double-barreled crisis from collapsing crude and the coronavirus, Saudi Arabia’s Finance Minister Mohammed Al-Jadaan unveiled nearly $27 billion in austerity measures.

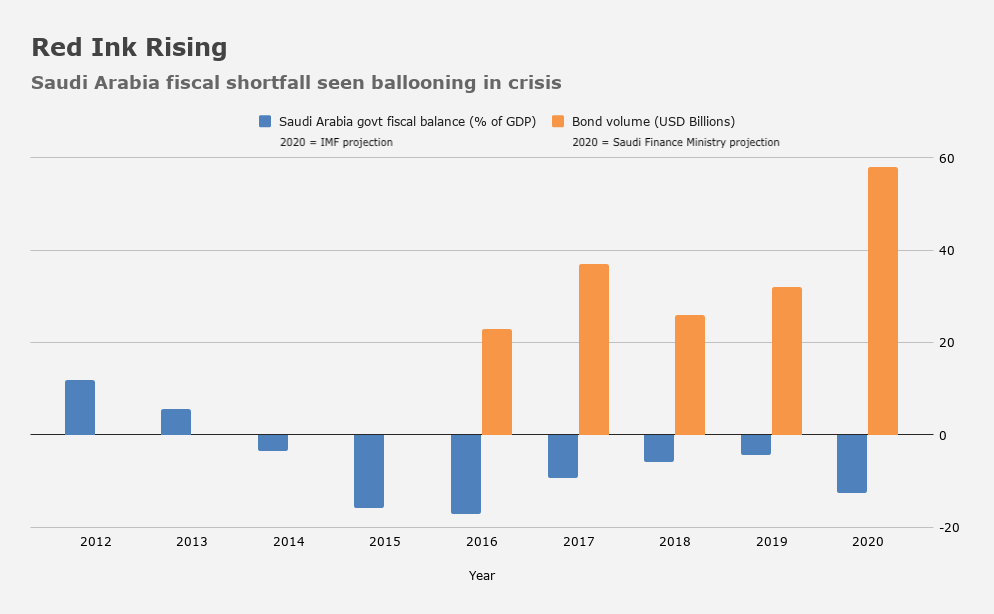

Headlining the package is a tripling of the VAT tax beginning on July 1, a step that could prove unpopular. In addition, a 1000-riyal per month allowance for state workers will disappear, and spending on costly projects will be trimmed or delayed. Taken together, the steps could help limit red ink, which is expected to total between 12% and 15% of GDP in 2020.

Late last month, Al-Jadaan said the government may issue another 100 billion riyals in debt this year in an effort to help stop the expected budget bleed. When you add that to the 120 billion riyals in issuance already announced, it means the kingdom could tap the market for around $60 billion in 2020, the most since its debut four years previous.

The government is walking a fine line. Austerity risks sparking social unrest, a non-starter for the monarchy. That means fiscal belt-tightening needs to be paired with measures aimed at pacifying everyday people. King Salman on Monday said families on welfare will get 1,000 riyals and 500 riyals for every dependent in a cash handout. That comes on the heels of additional assistance in the form of cheaper electricity and guarantees aimed at preventing private sector job losses.

“The kingdom hasn’t witnessed a crisis of this severity over the past decades”, Al-Jadaan said earlier this month, noting that the government will need to adopt “very tough and strong measures” which will be “painful” even as they are “necessary”.

The kingdom’s reserves are sitting at a nine-year low after crude’s epic collapse.

That is supremely ironic, given that this was, in part anyway, a self-inflicted wound. The Saudis spitefully flooded the market in March to punish Russia for its recalcitrance in Vienna, a move that proved disastrous as the scope of virus-related demand destruction became apparent.

On Monday, the Saudis said they will unilaterally slash output by 1 million barrels per day on top of their commitment in the new OPEC+ deal.

Aramco will pump less than 7.5 million barrels per day next month. That would be the least in – get this – 18 years.

As Bloomberg notes, “the cut is particularly symbolic as it brings Saudi production below 8 million barrels a day, long seen by many consultants and traders as a red line the kingdom wouldn’t cross”.

Desperate times call for desperate measures, I suppose.

Last week, Aramco raised prices in a bid to help juice momentum already building in the market, as the worst of the demand destruction from the virus is seen having passed, while major developed economies begin the gradual process of reopening.

Commenting in a phone interview with Bloomberg on Monday, Prince Abdulaziz bin Salman said “We have to be ahead of the curve”.

It’s far too late for that.

Read more: Royal Reckoning: Saudi Arabia Faces Daunting Reality After Crude Crash

When they couldn’t pay the real malcontents to shoot civilians and occasionally a few Houthi’s looting an NGO’s food truck in Yemen anymore, you knew there was trouble brewing.

It may be in the worlds best interest if the Dollar would depreciate. I have no single nations self interest in mind.

Zero sum game does not fit the COVID bill.