With trade tensions running high, no one should be surprised by this outlook.

That rather blunt assessment comes from WTO Director-General Roberto Azevedo, who earlier this week detailed the rationale behind the organization’s downgraded outlook for global trade.

“Trade cannot play its full role in driving growth when we see such high levels of uncertainty”, he continued, before warning that “if we forget the fundamental importance of the rules-based trading system we would risk weakening it, which would be an historic mistake with repercussions for jobs, growth and stability around the world.”

It’s probably safe to say that most people (even undereducated voters in western democracies who are otherwise vulnerable to the siren song of right-wing populism) understand, intuitively, that there are myriad benefits to a well-oiled system of cross-border trade. America’s farmers understand it, that’s for sure. And if something were to go “wrong” in trade discussions between the US and China, many low income Trump voters would get a crash course in macroeconomics in the event tariffs on the $200 billion in Chinese goods that were taxed at 10% from September 24 were hiked to 25% and/or duties were slapped on all Chinese imports, driving up prices for cheap consumer goods.

In any case, it’s important not to lose track of the fact that global trade is decelerating markedly and that trend is unlikely to reverse itself immediately even if Trump does manage to seal what he pitched on Thursday as a “granddaddy of them” trade deal with Beijing.

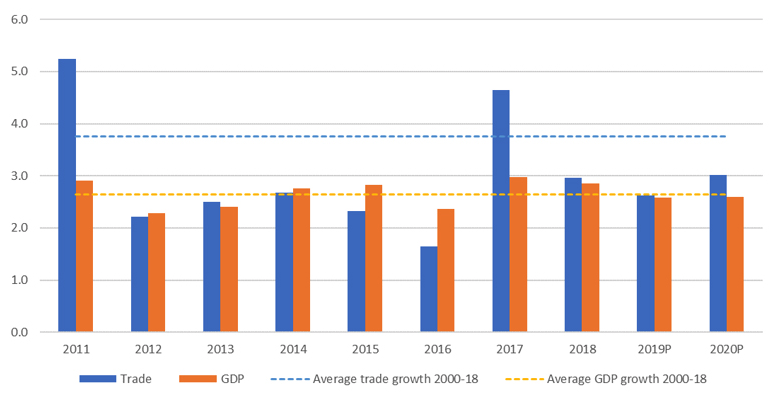

Here’s a snapshot of the WTO’s new forecasts versus the organization’s projections from September:

Of course, trade dynamism had been waning prior to Trump and in that context, robust trade growth in 2017 (a banner year for financial markets and prior to Trump ramping up trade threats) appeared to bode well. But as the WTO lamented this week, that now looks like a false dawn.

“The above-average trade growth of 4.6% in 2017 suggested that trade could recover some of its earlier dynamism, but this has not materialized”, the organization wrote, adding that “trade only grew slightly faster than output in 2018, and this relative weakness is expected to extend into at least 2019, partly explained by slower growth in the European Union, which has a larger share in world trade than in world GDP.”

(WTO)

BofAML’s Barnaby Martin underscores all of the above in his latest note. “One less benign statistic of late has been world trade volumes. The latest data point suggests that global trade activity has fallen to its weakest level since mid-2009, and is now far below the growth rates in global industrial production”, he frets, adding that “in pre-Lehman times, however, note that world trade growth would often be much stronger than world GDP growth.”

(BofAML)

As noted above, it’s not likely that this situation is simply going to inflect for the better as soon as Trump shakes hands with Xi over more chocolate cake at another surreal summit in Mar-a-Lago. In fact, given the precarious state of the euro-area economy, things could get materially worse if any subsequent rebound in China’s economic fortunes isn’t enough to offset a situation where Trump turns his (figurative) guns on Brussels.

Martin touches on this in the same cited note. “Populism in the form of tariffs and trade wars has clearly not helped global export volumes over the last year”, he writes, on the way to cautioning that “the extent to which global trade bounces back after a US-China trade deal remains to be seen: if President Trump pivots to Europe and further escalates trade tensions there, then global trade volumes may be a lot slower to recover.”

Credit Suisse echoes the above in their latest quarterly outlook piece. Although the bank harbors a generally upbeat assessment of where things go from here, they admit to being a bit surprised at the “severity” of the deterioration in some growth metrics. To wit:

- The global tradeable sector has seen a sharp slowdown. Global industrial production and trade, having slowed steadily during 2018, decelerated abruptly late last year. By Q1 2019, both output and trade were contracting. A situation rarely seen outside of recessionary conditions.

The bank’s James Sweeney attributes this to four main factors: Slowing Chinese domestic demand (in part due to Beijing’s efforts to squeeze leverage out of the shadow banking complex), capital outflows from emerging markets (catalyzed in part by Fed tightening), trade disputes (namely US tariffs on China) and idiosyncratic shocks (e.g., the US government shutdown, signs of political discord in France, Brexit jitters, Italian politics, etc.).

Again, Sweeney is optimistic, but his tone is a bit more cautious than it was in some of last year’s notes. Here’s an additional excerpt:

- Our central view remains that this is a slowdown concentrated in the industrial sector, and not one that will broaden into the rest of the economy with recessionary consequences. And we think it is a slowdown that is set to trough imminently, if it has not already. But its severity means the risks of it broadening and deepening are higher than we expected. The global economy is extremely vulnerable to an additional negative financial, economic or confidence shock.

For his part, Martin worries that the risks around protectionism might be skewed to the upside simply by virtue of the fact that tariff levels have already declined as much as they have.

“Tariff levels have already fallen significantly over the last 30 years, and room for further declines looks much more limited now”, he says. Here’s a bit more from his note:

- Since the early 90s, Emerging Market tariff rates, in particular, have fallen substantially thanks to transformational trade agreements. After 2008, though, global tariff rates have been roughly stable, and the global average tariff rate is now just 3%. With limited room to fall further, the marginal boost of new trade agreements to world trade volumes has decreased significantly (new trade agreements act more to provide trade ‘frameworks’ etc.). Moreover, non-tariff measures have become a popular approach since 2010 to restrict trade flows (as opposed to resorting to tariff increases). Chart 15 shows how the growth in discriminatory trade measures has jumped lately.

(BofAML)

(BofAML)

Needless to say, the US president’s latest threats with regard to using auto tariffs (“the big ball game”, as he called them) to punish Mexico for the flow of illicit substances across the border suggests Washington will continue to weaponize trade to fight political battles.

And speaking of that, the WTO rendered a watershed decision on Friday when the organization waded into the national security discussion for the first time. “The landmark ruling, on a dispute between Russia and Ukraine, both affirms the rights of nations to impose trade restrictions on national-security grounds and asserts the WTOs authority to determine whether a security threat warrants such restrictive measures”, Bloomberg writes, adding that “the Trump administration has said the WTO doesn’t have the power to rule on these matters.”

Weighing in on the situation Thursday, Roberto Azevedo said this:

- Issues that are sensitive enough to bring up national security concerns should be treated politically and not technically at the dispute settlement mechanism of the WTO. But they are bringing the cases and we don’t have an option.

Nothing further.

{kind=link}

Have long speculated because the huge emphasis on the China Deal would cause an overshoot situation whereby Europe winds up a loser. This is a zero sum game especially with downward trends described in this post solidly entrenched