Although last week was uninspiring for equities and appeared to suggest the market has reservations about the capacity of monetary policy to reflate the global economy and bring about a sustained rebound in risk assets given the rather challenging macro and political backdrop, let us not simply pretend like January didn’t happen.

If December represented a downside overshoot predicated on overblown recession fears and what Marko Kolanovic described as a “collapse of confidence“, then January restored some semblance of sanity, effectively resetting things to late-November status – a mulligan, of sorts.

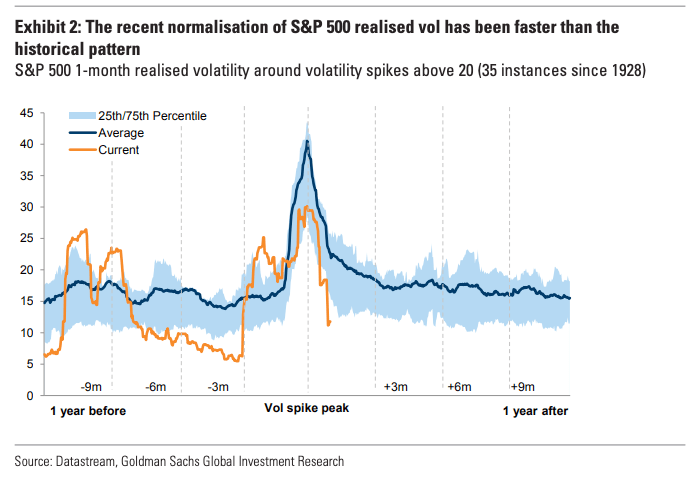

You probably won’t be surprised to learn that the best start to a year for equities since 1987 was accompanied by a rapid “normalization” (if that’s how you want to couch things) of volatility.

Specifically, Goldman notes on Monday evening that the drop in 1m realized (from 30% a month ago to 11% now), is “one of the largest drops since 1928.”

(Goldman)

You might recall that one of the defining features of the “buy the dip” regime was the rapid snapback of volatility on any fleeting spike. The flipside of “buy the dip” in equities is “sell the rip” in vol., and it was a bulletproof plan for years. We’ve spent a ton of time in these pages documenting how “BTFD” morphed from a derisive meme about retail investors into a virtually infallible “strategy.” Here’s a quick recap:

How was “BTFD” legitimized? How did it come to be that “BTFD” went from being a standing joke to a real thing?

The vaunted “Goldilocks” narrative of synchronous global growth and still-subdued inflation underpinned the low vol. regime by allowing traders to point to upbeat economic indicators while citing well-anchored inflation as a reason to expect central banks to remain accommodative for the foreseeable future.

And when it came to central banks, the two-way communication loop between policymakers and markets became a self-fulfilling prophecy. Markets became so conditioned to policymaker intervention and dovish forward guidance that no one saw any utility in waiting around for it anymore. After all, if you know it’s coming, why wait on it? Why not buy the dip now?

Well, in 2018, a simple BTD strategy stopped working, much to the chagrin of every retail investor on the planet.

Read more

Heresy! For The First Time In 16 Years, Buy-The-Dip Has Failed

In any event, January’s rapid snapback in volatility was reminiscent of the Goldilocks era. In fact, as Goldman goes on to write in the same note cited above, “the volatility normalization is currently one of fastest compared to other historical spikes.”

(Goldman)

That’s a sight for sore eyes for those of you who are nostalgic for the low vol. regime.

The bad news is, Goldman doesn’t see us returning to a true “Goldilocks” environment anytime soon. While inflation remains subdued (giving central banks the cover they need to lean dovish), the bank notes the obvious, which is that “the macro backdrop is unlikely to be as supportive as in 2017.”

That’s probably an understatement.

The message for whatever BTFD’ers are left after 2018: enjoy this flashback to the halcyon days while it lasts.