First thing’s first: China reopens this week after the holiday and there’s no shortage of information for mainland markets to process and price.

Enter the dragon

Over the last several days, tensions between Washington and Beijing were ratcheted up further following Bloomberg’s blockbuster “tiny spy chipâ€Â exposé and Mike Pence’s contention that China is meddling in U.S. elections, an allegation Beijing called “ridiculousâ€. Pence, China says, should avoid spreading “malicious slander”.

On top of all that, naval tensions are running high in the South China Sea, so if you’re wondering whether trade frictions between the world’s two largest economies are likely to abate any time soon, the answer is probably “no”, or actually “NO” (in Trumpian all-caps).

Over the weekend, China delivered another RRR cut, and that will likely put further depreciation pressure on the yuan, PBoC efforts to downplay the move notwithstanding. As noted earlier, the onshore yuan has some catching up to do with its offshore counterpart.

Following a four-pronged effort to put the brakes on the yuan’s slide in August, the currency looks set to push above 6.90 again.

(Bloomberg w/ annotations)

Although Premier Li Keqiang last month promised not to weaponize the currency, the more fraught Beijing’s relationship with Washington becomes, the more likely it is that China will countenance depreciation if they believe heightened tensions with the U.S. are set to contribute to the ongoing deceleration in the Chinese economy. FX reserves are still some semblance of steady so it doesn’t appear that capital flight is materializing. Ostensibly, that means there’s still scope for the PBoC to devalue without sparking a panic.

“US-China trade tensions continue to cause concern, and as China markets reopen after the Golden Week holidays, we estimate that a USDCNY fix of 6.94 is consistent with a stable CNY CFETS NEER, versus a previous fix of 6.8792”, Barclays wrote over the weekend.

Emerging markets and crude concerns

This is something of a critical week for emerging markets. Surging U.S. yields and a renewed rally in the dollar drove the worst week for EM equities since February last week.

As Barclays notes on Sunday, surging oil prices present a problem for certain EM economies, even as rising commodities prices help support the global reflation meme which, all else equal, is a boon for risk assets.

“Recent gains in oil prices and US interest rates are likely to continue to weigh on the assets of economies dependent on energy imports and global capital”, the bank writes, adding that “higher oil prices are particularly problematic for large net oil importers in EM with current account deficits or countries where energy represents a large portion of CPI baskets. Vulnerable currencies include the PHP, INR, ZAR and TRY.”

Speculators trimmed bullish bets on Brent for the first time in six weeks through Tuesday, as some folks appear to be taking profits after a sharp run up in crude prices triggered by concerns about Iran, among other things.

(Bloomberg)

Also on the radar for EM: first round general election results in Brazil.

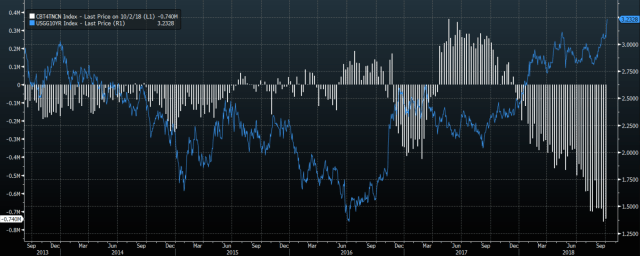

Inflation nation and the burgeoning bond bear

In the U.S., all eyes will be on long end yields after last week’s remarkable bond selloff which spilled over into equities on Thursday and Friday. The rout is now more severe than that which unfolded in January.

The bond market enjoys a three-day weekend thanks to Columbus Day.

Read more

Specs extended shorts in the long end in the week through Tuesday and the 10Y short remains near record territory.

(Bloomberg)

It’s against the backdrop that we’ll get CPI in the U.S. this week. The August print showed inflation cooling a bit, but it’s possible tariff effects will start to creep into the data. “Above-target US inflation should support recent increases in US rates, and Fed rhetoric has indicated an ongoing commitment to tightening that remains underpriced by rates markets”, Barclays cautions, adding that if you ask them, core rose 2.3% YoY in September, while headline should print at 2.4%. Goldman and BofAML are at 2.3% on core as well.

More than a few commentators continue to insist that the market is mispricing the chances of a sudden pickup in inflation. The more data-dependent the Fed, the bigger the risk that a “rogue” print (to quote Nomura’s Charlie McElligott) catches everyone wrong-footed. “Going forward, a rogue inflation beat without a doubt is the largest risk-off threat to risk-asset psyche, as it disrupts the current ‘steady’ pace of normalization and would pivot the ‘risk-positive’ narrative from ‘growing faster than we are tightening’ to then risking ‘Fed policy error’ due to ‘over-tightening risk’â€, McElligott wrote on Friday.

The dollar will be watched closely in light of all the above. The greenback logged its longest winning streak of the year last week, before finally taking a breather on Friday. Positioning is still stretched:

(Bloomberg)

That’s hardly the end of it in the U.S. We’ll also get PPI, trade data, University of Michigan and more Fed speakers than you care to count.

Earnings

Additionally, earnings season gets under way this week with JPMorgan, Citi and Wells up on Friday. This should be another strong quarter for corporate profits, but the outlook after that is decidedly more cloudy, as some say tariffs, wage inflation and rising rates will start to dent margins just as the impact of fiscal stimulus begins to wane.

(Goldman)

Ciao bella

In Europe, the focus continues to be on Italy and the budget. The country made a couple of minor concessions late last week that helped stanch the bleeding in Italian stocks and bonds, but the relief seems likely to prove fleeting. As Barclays rather ominously notes, the risks going forward include “a potentially difficult institutional relationship with Brussels, rating agencies’ potential response, debt sustainability considerations, a loss of credibility, and non-marginal risks of snap elections.” Italian financials have fallen some 13% in the past two weeks.

Oh, and watch for any escalations between Ankara and Riyadh, because it certainly seems as though tempers are about the flare over the disappearance of Saudi dissident Jamal Khashoggi.

Full calendar via BofAML

https://www.youtube.com/watch?v=umMDO_HNlCU from https://heisenbergreport.com/2018/02/12/david-stockman-last-week-wasnt-an-error/

Check out the first 2 minutes of this video…note 0:45 and and 1:15.

I remember reading/watching this and was telling people…wait for October…