Have we seen the turning point for bonds?

I hope so. I like being right as much as the next guy, and I’ve variously suggested the US long-end was a knife worth trying to catch over the past 10 or so sessions.

Yields tumbled on Tuesday in a catch up to the holiday futures rally and the long-end was supported early Wednesday too, despite a warm PPI print.

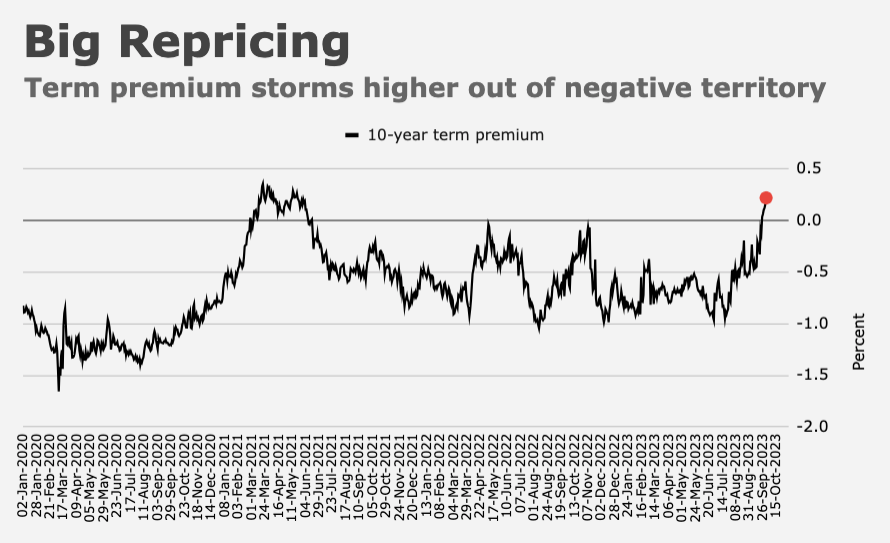

As noted in the first linked article above, the nascent bullish reversal is widely attributed to a shift in the Fed rhetoric, which now suggests the Committee is amenable to the idea that recent term premium repricing and the attendant rise in real yields can stand in for the final rate hike tipped by the dots.

On Wednesday, Nomura’s Charlie McElligott weighed in. “A move into rates / duration upside has been the right one following the peak of the capitulatory selloff last Tuesday, as the Fed’s coordinated ‘end of tightening cycle’ messaging shift in recent days has proven the turning point for US Treasurys,” he wrote, noting that the Fed’s tone shift is occurring amid a flight-to-quality in consideration of the multi-faceted spillover risks from the Israel-Hamas war.

“It’s now highly probable that Fed hikes are complete, and that we have seen the peak in front-end rates,” Charlie went on, noting that nearly a full 25bps cut has been added back to 2024 pricing in just a few days.

After falling in 10 of the last 11 weeks, the popular long-end US Treasury ETF was on track for its best week since March. Plainly, a hot CPI print had the potential to derail things, but a cool read (or even an in-line print) could perpetuate the bid.

That product (TLT) is at the heart of what one ETF expert recently called “the new ‘fight the Fed’ trade.”

McElligott described the macro thinking among traders. “The now widely-held market perception is that the Fed’s ‘September SEP shocker’ finally got them their much-desired FCI tightening” which then did some of “the remaining dirty work on inflation for them, via a profound term-premium repricing.”

So, what now? Well, in addition to any help from cool data, there’s some potential for the nascent long-end rally to extend on the market’s assumption that regardless of what officials decide about another hike in 2023, they aren’t likely to give up on the “higher-for-longer” narrative anytime soon.

Sticking with that narrative “increases the likelihood of a larger-magnitude economic slowdown, or even a ‘hard landing’ accident, which is then further helping to shift the risk / reward on USTs locally after such a profound recent cheapening,” McElligott said.

{kind=link}