It’s possible that Wednesday’s CPI release in the US marked a turning point in the battle to coax the inflation genie back in the lantern.

As documented here in real time and across a pair of subsequent articles, the figures constituted what I’d be inclined to call the first definitive evidence in favor of the notion that the disinflation process has well and truly begun.

Context is important. The below-consensus read on price growth for June should be considered with a third straight drop on a key gauge of wholesale used vehicle prices, moderation in ISM price gauges for both manufacturing and services, as well as a 27-month low in a measure of small business price hike intentions. If you believe shelter disinflation is indeed in the pipeline, the stars might’ve aligned for the Fed, even as it’s unclear how much credit they deserve for decelerating price growth.

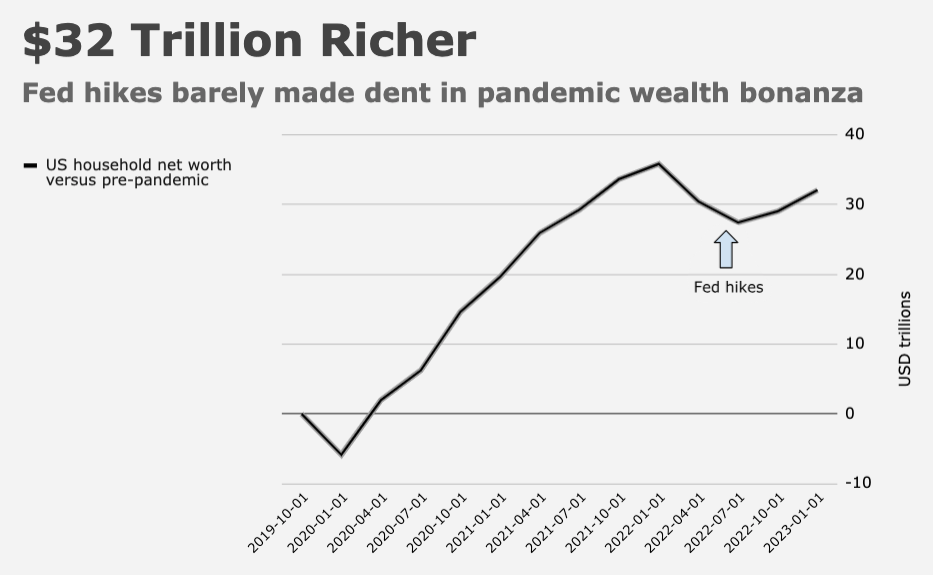

Of course, this is all still tentative. We’ve seen at least two false dawns this cycle, and there’s no guarantee this won’t eventually be remembered as a third. Base effects won’t be as favorable going forward, and it’s certainly possible that commodities could rebound, or that the wealth effect from this year’s equity rally and the resumption of home price gains could rekindle a spending impulse that would’ve otherwise waned. Consumer credit data released this week showed borrowing was the most tepid since November of 2020 in May, and we’re told pandemic savings are finally drying up, but a simple chart of household wealth versus pre-pandemic levels suggests Americans are still sitting on an extra $32 trillion, and that doesn’t count gains notched in Q2.

But, in consideration of the possibility that June’s CPI figures were, in fact, a pivotal moment, I thought it’d be prudent to highlight a few brief quotes from analysts, just to give readers a sense of how the data was perceived on Wall Street. Find a short compendium below.

The inflation battle is won! Will the Fed stop driving the economy into recession? Supercore (ex-food, energy and shelter) actually fell slightly in June — very unusually. And taking the last 12 months, the average monthly rise has drifted back down to 0.2%. Powell has been obsessing about supercore services inflation. If he means services CPI ex-energy and shelter, we are back to spitting distance YoY of pre-pandemic rates. — Albert Edwards, SocGen

Today’s report is consistent with our view that Fed tightening is in its final innings. We continue to expect a final 25bps hike at the July FOMC meeting to 5.25%-5.5%, followed by unchanged policy for the remainder of the year. We continue to believe that residual seasonality in travel categories weighed on the core reading, but the 8.1% airfare pullback was even larger than we had expected and reflected genuine weakness in the not-seasonally adjusted data. The composition of the report was generally encouraging from a disinflation perspective. Shelter categories slowed modestly further and used car prices fell 0.5%. We believe the latter is the beginning of a larger pullback, based on the 10% drop in wholesale auction values. — Jan Hatzius, Goldman

The June core CPI reading sets the stage for the “summer of slowing” for inflation that we have been anticipating: We expect broadly similar core CPI gains for the July and August reports. The momentum in core price inflation is also starting to turn the corner: The three-month AR pace fell to a still firm 4.1% but from an average of 5.0% in Jan-May — we expect it to slow down to 2% by Aug-Sep. Furthermore, the measure of core services ex-housing that the Fed actually tracks (PCE’s) told a similar story in May. Given the lagged impact from private rents data in the CPI series, we are likely already through the final passthrough of peak strength. We remain of the view that housing inflation will continue to bounce around month-on-month, but now within a new range (0.4%-0.5% MoM). Shelter inflation remains a wildcard for core inflation in the near term. A July hike is a done deal; no additional hikes after. — Oscar Munoz, Gennadiy Goldberg and Molly McGown, TD Securities

Unfortunately over the next couple of months we are likely to see headline annual inflation rise again, albeit modestly. This will largely reflect the fact that 0% and 0.2% MoM readings from July and August last year will drop out of the annual comparison. Core inflation won’t have this problem as we saw 0.3% and 0.6% prints for the same periods last year, making it more likely that the annual core rate of inflation will continue to slow through July and August. Moreover, with housing set to slow sharply based on observed rents and used car prices set to fall further based on auction prices we are increasingly confident of a sub 3.5% YoY core CPI print by year-end while headline inflation could be around 2.5%. This is certainly not enough to prevent a July rate hike given the Fed’s current position, but suggests less need for the second hike it is currently indicating. — James Knightley, ING

It wasn’t a CPI report that will keep the Fed from hiking in two weeks, although the breadth of the softness underlying the 0.158% MoM increase in core consumer prices has shifted our expectation from July’s rate move being of the hawkish variety to something a bit more measured from Powell. As it relates to September however, the likelihood of an additional hike being needed has waned in the wake of June’s inflation data. Especially considering there will be two more NFP and CPI reports revealed before the September 20th decision, an extension of the trends revealed in June both in terms of hiring and prices would allow the FOMC to continue the process of keeping rates restrictive and maintain its willingness to tighten depending on the data. After all, by continuing to skew the forward path of policy higher rather than lower the Fed will be able to keep financial conditions sufficiently tight to persist in the battle against inflation. We’re not fading the Fed’s commitment to an extended period at terminal; instead, the longer the Fed remains restrictive, the deeper the cuts the Committee will eventually need to deliver. Funds/10s inversion is a dynamic that implies the Fed is a victim of its own success in reestablishing price stability — the greater strides Powell makes in regaining Fed credibility, the lower forward inflation expectations (breakevens) will drift, taking nominal 10s along for the ride. — Ian Lyngen and Ben Jeffery, BMO

{kind=link}

In a pragmatic-investor sense, I think the inflation battle is “won” in the short term and maybe the medium term.

For most investors, the battle is “won” when inflation slows enough to allow the Fed to stop raising rates and the market to stop raising yields based on inflation. If the Fed delivers one more 25bp hike, or two more, seems not that important. After 500 bp, is another 25-50 bp at the short end going to change things very much? The 10Y UST is already close to 4% and mortgages at 7%. Whether headline CPI hovers around 2.5-3.0%, or declines to 2%, over the next few quarters, also seems not that important – for investors.

By “short term”, I mean next couple of quarters.

Longer term, trend inflation may be higher than 2%, based on deglobalization, deficit spending, labor force constraints, etc. I don’t have conviction on that, and am not sure it matters from a near term investment perspective.

As I see all this data and reactions of various parties, I can’t help remember Pres. Bush and pointing to his silly sign that proclaimed “Mission Accomplished.” Only thing is, it wasn’t true. Wanting and having are two different things. The big inflation I remember in the sixties and seventies, took Nixon and Volcker more than a decade to vanquish. Stocks are high enough for now and five percent never killed anybody.