Are central banks “locking in” above-target inflation?

You’d like to think not. And policymakers would recoil at such a notion.

But according to one popular strategist, that may be just what’s happening. Developed market monetary policy is either on hold, or close to pausing, even as core inflation across advanced economies remains very high.

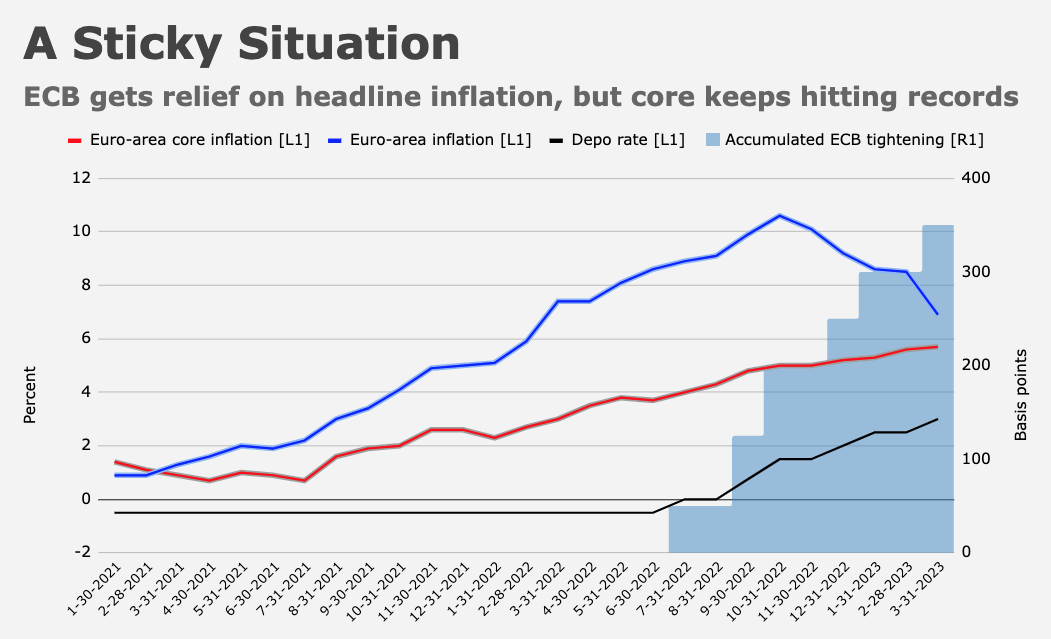

Core inflation in the eurozone hit a new record last month, for example, the UK is vexed by price pressures which refuse to moderate and the situation isn’t much better in the US, although recent data suggests the world’s largest economy is finally beginning to cool.

The simple figure above from BofA’s Michael Hartnett tells the story. Or it tells a story, at least.

On some days, I see a light at the end of this particular tunnel, on others not so much. Suffice to say the odds of core inflation remaining elevated in perpetuity are probably as good as the odds of underlying price growth moderating back to target. And that’s a problem.

We have “high core inflation plus low unemployment plus negative real policy rates, yet almost all central banks are on hold or close to the end of rate-hike cycles, thus ‘locking in’ high inflation, as is the trajectory of government spending, deficits and debt,” Hartnett wrote, in the latest installment of his popular weekly “Flow Show” series.

The heading on the table shown below (i.e., “…mean weakened CB incentives to reduce inflation”) is Hartnett finishing a sentence. The preceding charts showed the US national debt and the federal budget balance. Those charts carried the headings: “National debt at all-time highs…”, “and elevated federal government deficits.” So, the full sentence is: “National debt at all-time highs and elevated federal government deficits mean weakened central bank incentives to reduce inflation.”

“No central bank is truly looking to ‘whip’ inflation despite protestations to contrary,” Hartnett went on, adding that “secular inflation is the core reason US 10-year Treasury yields are struggling to break below the 3.5% 200-DMA despite the ‘peak CPI,’ ‘peak Fed,’ ‘impending recession’ narrative.”

With that in mind, I do think it’s important to acknowledge that as antiquated (both from the perspective of practical usefulness in policymaking and certainly from the perspective of an electorate which is increasingly insistent on more progressive social policies) as many traditional “textbook” models and frameworks might be, they do still have some explanatory power.

The problem with, for example, the Phillips curve or monetarism, isn’t that they’re fatally flawed or imperfect. I hate to be the bearer of bad news, but “fatally flawed and imperfect” describes every human being who’s ever existed, so we should expect the same from the models humans create in the service of advancing a soft science. The problem with such frameworks, rather, is that we insisted on calling them “rules” and “axioms” or, worse, treating them as immutable and reliable in the course of making policy, as opposed to simply consulting them as part of a more comprehensive, common sense, subjective, non-scientific process. When they “failed” to perform as well as the rules and laws of hard (i.e., real) sciences, we jettisoned them, or began the process of demoting them for political expediency.

Now, we’re learning that was a mistake. Expanding the money supply with no regard whatever for the relative scope of that expansion and without taking account of what cutting out the QE middleman (banks) might mean when the supply side of the economy is severely constrained, helped stoke inflation. Just as monetarism might’ve predicted.

Unlike monetarism, the Phillips Curve wasn’t relegated to the dustbin of history by economists. On the contrary, it was accorded so much respect that when it allegedly stopped working, politicians with an interest in seeing it scrapped couldn’t help but notice. The relationship between the labor market and inflation had become but a “faint heartbeat” by 2019, as Jerome Powell put it, in a famous exchange with Alexandria Ocasio-Cortez. That motivated a push to deemphasize it.

But, as it turns out, the relationship does still exist through the wage channel, which is what the model was concerned with in the first place. There’s still a tradeoff. If demand for labor exceeds the supply of it, the price of labor will generally go up, and while the transmission mechanisms (plural) from that simple relationship to consumer prices operate with varying degrees of efficiency and on sometimes unpredictable time tables, they do operate.

Like all things, what happened over the past three years is easy to explain in hindsight. We pushed the envelope without giving due consideration to prevailing supply-side constraints for, initially, goods, and then later, for services, the provision of which was hampered by an insufficient supply of labor.

The theories and models exacted their revenge not because they were more “true” than we gave them credit for, but rather because the sheer magnitude of the macro distortions in the 2020s meant that if they had any explanatory power at all, it’d be amplified in direct proportion to the scope of the mismatch between supply and demand.

With that in mind, it’s not unreasonable to suggest that maybe — just maybe — pausing rate hikes with core inflation miles above target, unemployment at rock-bottom levels and real policy rates still negative, will indeed serve to “lock in” inflation for the foreseeable future.

{kind=link}

I think it’s important to acknowledge that we were staring down the barrel of another great depression due to the impact of the pandemic, and that erring on the side of too much helicopter money was a better move than risking the alternative. To your point, it’s easy in hindsight to see stimulus, both monetary and fiscal, might have been too much, especially given the supply constraints, but all things considered, the inflation we’ve experienced was likely worth ensuring that the economy didn’t completely fall apart (assuming that doesn’t still happen).

Agreed. A major problem with decision/policy making is that once a decision or policy has been made, time starts to pass and things change, never to be the same again. “This time” is always different. So once we decide something we can’t go back and see what would have happened if we had done something different that what we actually did. Second guessing is always futile. We can record what we did and what we think happened, but in a world as complex as the one we have, we won’t ever know all that really happened so using past information in the next decision will create new errors we can’t foresee. Just ask any pro golfer whose lost their swing or a baseball player whose gone 0 for his last 44 ABs.

If you think in terms of population biology, it is not unreasonable to think that inflation will be sticky. The resources that people need to live and thrive are becoming scarcer, in the face of an increasing population of humans. Relative scarcity of resources means those resources are more valuable. With increasing competition for resources, people will work harder to secure those resources, which results in greater conflict, in turn resulting in the need to spend a greater proportion of resources on defense (or aggression).