It’s fine unless you need new financing.

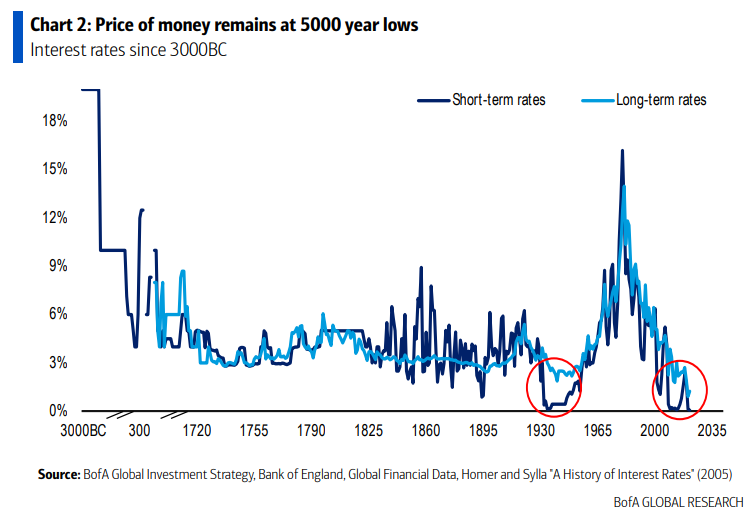

That applies in a lot of contexts right now, sitting as we are with the highest rates of the post-Lehman era barely a year removed from the lowest rates in several millennia.

The most popular refi apocalypse narrative centers around CRE, but outside of doomsday prophesying, the stark juxtaposition between where we were with rates 12 months ago and where we are now is also a contributing factor to the dearth of housing inventory in the US.

Would-be sellers who might otherwise be looking to upsize (either literally with more square footage, or just figuratively in terms of neighborhood or “niceness”), won’t sell because the much higher cost of financing complicates what would otherwise be a no-brainer “trade.” Crucially (and Americans take this for granted), you don’t typically have to obtain new financing as a homeowner in the US. The refi either works in your favor (when rates go lower) or you just don’t do it.

That latter bit is important when it comes to monetary policy transmission. The Fed can leverage the housing market to stimulate the economy (e.g., through the wealth effect or by incentivizing demand and thereby residential investment), but the only way to slow the economy through housing (now that we don’t have waitresses with two homes and a condo all on ARMs) is to constrain new buyers’ capacity to participate. That might work through the residential investment channel, but it’s not going to be especially efficient when it comes to curtailing consumer spending, which is where you really need to apply the brakes if you’re trying to curb inflation in a services-based economy.

Now think about it from the corporate side. It’s the same thing. When you drop rates to the lower bound, smart borrowers with ready market access will take advantage by issuing long-term, fixed-rate debt (getting a mortgage on the consumer side), thereby insulating and inoculating themselves from future policy tightening.

While you could argue this is all a good thing for financial stability, it’s suboptimal for technocrats trying to micromanage demand. Interest costs for corporations are the lowest ever despite the most aggressive policy tightening in four decades (see the chart below). And assuming you didn’t overextend, anyone who bought a home during the pandemic is still sitting on a tidy gain, with a very low monthly payment.

“The transmission of tighter monetary policy has yet to kick into gear,” SocGen’s Jitesh Kumar and Vincent Cassot wrote, in a note published Friday. “Corporations were able to issue newer debt at lower costs following the pandemic, termed out debt to longer maturities and as a result, sensitivity to changes in interest rates is likely to have been dampened in the near-term.”

Again: For affluent Americans without revolving debt or other variable rate obligations, the same is generally true. Monetary policy isn’t going to be very efficient. Your mortgage payment isn’t going to change, and if you have no credit card debt and don’t need a new car, all you need to worry about is keeping your job.

So, rate hikes could take a very long time to materially impact corporates and wealthy households. That suggests (almost inescapably) that the burden for cooling the economy will fall to consumers who need new financing or who rely on variable rate debt to make ends meet.

“Fortunately” (note the scare quotes) those are the economic actors with the highest marginal propensity to consume. Lower- and middle-income households tend to spend a larger share of every dollar by virtue of the fact that they don’t have many — dollars, that is. As the figure below suggests, those households (the ones who rely on credit cards and installment loans) are about to feel it.

“There is some economic weakness in the pipeline,” Kumar and Cassot went on to say. “Most importantly, credit availability is going to be a problem at some point [and] balance sheets are in focus as the marginal reduction in credit is likely to affect companies with weaker balance sheets first.”

The weaker you are, whether you’re a household or a corporate, the harder you’re likely to be hit.

Of course, on the household side anyway, there are far more “weak” links than strong ones. So, to the extent we’re relying on throttling those consumers to bring down inflation, this is a kind of reverse utilitarianism. Which is appropriate for America. Socialism for the rich, capitalism for the poor.

{kind=link}

Haven’t thought about it that way, thanks for the piece.

That last sentence about socialism for the rich and capitalism for the poor, that didn’t happen by accident. It’s built into the system, perhaps not by design but because that’s what human nature strives for.