This time last year, the Fed was busy disavowing “transitory” as a description of the inflation percolating in the US economy.

Headline CPI, which loitered harmlessly just above 1% in December of 2020, was up to almost 7% and calls for the Fed to do something (anything, really) were becoming more urgent virtually by the day.

Two weeks after telling US lawmakers that the “T word” was, like so many former members of the labor force, headed for early retirement, the Fed dropped “transitory” from the policy statement. Three weeks later, on January 5, 2022, the release of minutes from the prior month’s FOMC meeting triggered a selloff on Wall Street. Five-year real yields rose 30bps that week. The rest, as they say, is history.

375bps of rate hikes and (literally) no progress on inflation later, the Fed will close out an extremely difficult year with 50bps in additional tightening. In a testament to what kind of year it’s been, 50bps now counts as a dovish increment. 12 months ago, the idea of half-point moves was still considered overkill, although unless you count recency bias as an excuse, it’s not clear why.

The figure (below) shows different measures of the underlying trend in inflation. Again: There’s scant evidence of progress.

Although October’s CPI report was celebrated as a potential turning point, producer price data for November suggested it’s far too early for such calls. The Fed will get consumer price data for last month the day before this week’s decision.

The official rationale for slowing the pace of rate hikes was outlined by Jerome Powell after last month’s FOMC meeting. Having expeditiously hiked rates into restrictive territory (albeit just barely), the more important questions now are “How high?” and “How long?”, not “How fast?”

There are two additional rationales for slowing down. First, monetary policy acts on unpredictable lags. Driving using the rearview mirror hasn’t generally served policymakers well over the years, so rather than fight “yesterday’s” battle, the Committee will now downshift and hope that the tightening already delivered, combined with an additional 75-100bps expected over the first half of 2023, will eventually curb inflation. And hopefully without torpedoing the economy. Second, financial stability will become an issue at some point, it’s just not clear where the threshold is. The Fed would plainly rather not cross it. Reducing the pace of hikes ostensibly lowers the odds of an accident in markets.

It’s possible that a scorching-hot November CPI report could tip the scales in favor of a fifth straight 75bps hike this week, but that seems doubtful. It’d be a hawkish surprise for markets, which have all but priced out another three-quarter point move.

You could argue that the very hot read on wage growth that accompanied November’s jobs report was itself cause for the Fed to delay a downshift, but if you think the Journal‘s Nick Timiraos has an inside line on the Fed’s thinking, the Committee’s consternation around wages is more likely to show up in nods to a higher terminal rate (and a longer stay in restrictive territory) than it is to manifest in another 75bps hike.

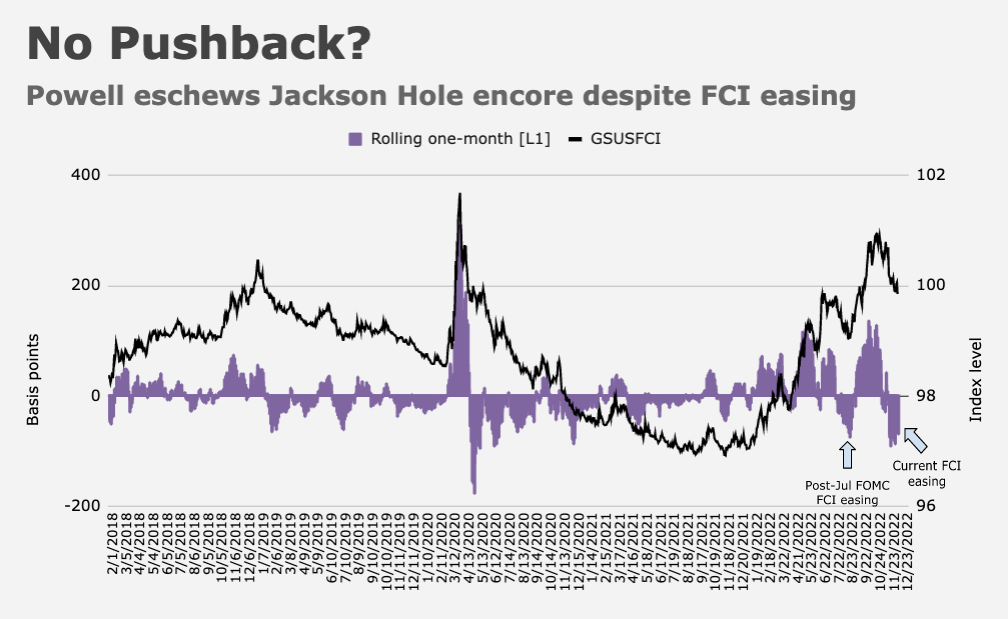

Do note: Powell was criticized in some corners for delivering an insufficiently stern message during a key speech for a Brookings event late last month. His decision to editorialize around the labor market less than 48 hours ahead of a jobs report he hadn’t seen was a poor one, in my judgment. Markets seized on his speech to push the issue on various manifestations of the financial conditions easing trade, only to learn that wage growth rose at double the expected monthly rate in November, when participation ticked lower, outcomes which plainly argued for a more aggressive Fed, and thereby tighter financial conditions. In all likelihood, Powell will be compelled to address that ostensible misstep this week, either directly or indirectly. He’ll almost surely devote some of his remarks in the press conference to the wage-setting environment.

“The November labor market report does not bode well for the Fed’s effort to bring inflation back to target,” TD analysts including Jan Groen and Oscar Munoz wrote. “With labor supply being constrained as it is, excess demand for labor remains elevated and is pushing up underlying inflationary pressures in the economy… strongly indicat[ing] that wages are catching up to and, at least partially, locking in higher near-term inflation expectations.”

In TD’s view, that dynamic is likely to keep “core services inflation sticky at elevated levels going into 2023.” Real wage growth is still negative in aggregate, but that could change next year as goods prices fall. That’d be a positive development (figuratively and literally) unless it results in an unwelcome uptick in consumption that prolongs services sector inflation.

In the same note, which featured contributions from Priya Misra and Gennadiy Goldberg, TD suggested the recent easing in financial conditions is “unlikely to be well received by the Fed, and Powell may use the December press conference to push back against market perceptions of a dovish Fed reaction function.”

“We also think the Fed will attempt to push back against excessive easing in financial conditions,” Goldman’s Praveen Korapaty said. “This is admittedly hard for the Fed to do, given rising market perceptions that tightening is close to being ‘done,'” he added, before suggesting how the Committee might go about compelling the market to curb its enthusiasm. “Possibilities include showing higher 2023 rates in the dot plot, Powell suggesting there could be more than one 50bps hike in his post-FOMC conference, or a material upward revision of the long run rate,” Goldman wrote.

The new dots are certain to reflect a higher terminal rate. Officials have uniformly stated that rates need to go higher than indicated in the September SEP, although the November minutes cast some doubt on how much higher. 5% is a foregone conclusion. It’s just a matter of whether the Fed wants to signal that “sufficiently restrictive” is likely to be materially higher than that, and also how long they imagine they’ll be able to cling to terminal.

As for the updated economic projections, the juxtaposition between a stubbornly resilient economy and the most intense rate hikes in three decades means the growth projections are even more of a blindfolded darts game than usual.

Obviously, the Fed isn’t going to forecast a deep recession and probably not any other sort of recession either, even as private sector forecasters, bank CEOs and the yield curve (figure above) all believe a downturn is a virtual guarantee.

On unemployment, it’s the same story: Critics think the Fed is far too optimistic. Powell is still convinced (or pretends to be, anyway) that millions of “extra” job openings suggest the labor market can balance without mass layoffs. Skeptics abound. The new forecasts will probably include small upward revisions to the unemployment projections — the key word being “small.”

“In the coming quarters, we have confidence in the Fed’s ability to bring the UNR from 3.5% to 4.4%, but not in its ability to prevent unemployment from moving above 5% more quickly than the Committee anticipates,” BMO’s Ian Lyngen and Ben Jeffery said, in their year-ahead US rates outlook. “It’s this reality that will eventually necessitate the Fed transition back to the dual mandate as it was originally conceived — i.e. containing the fallout in the employment sector.”

As for the updated inflation projections, the new forecasts will surely suggest that price growth will decelerate to more palatable levels in 2023, before returning to target (or somewhere close to target) in 2024. Write your own jokes.

{kind=link}

Short of calling them liars, I personally believe there are things that Fed chair can and cannot say even if he sees it as a likely outcome. Everything is sugar coated for safe consumptions.

i.e. Windows for soft landing is narrowing (hard); Some pain (lots of it); Keeping at it (Volcker hike)

The number of legal immigrants into the US is projected to be just over 1M in 2022- which is slightly higher than annual immigration rate pre-covid. If there truly are 10M job openings and only 6M job seekers in the US, it is going to take a few years for immigration to fill the job openings gap- but if immigration continues on a similar track, there should be significant progress made in 2023 and every year thereafter.

It seems unlikely that the labor participation rate will recover back to the pre-covid level of 63% from the current level of 62%- which roughly translates to a loss of 2.0-2.5M workers.

I remain hopeful for an updated immigration policy – however, 1M/year is better than I realized. Most legal immigrants are from Mexico (24%) followed by India (6%). Typically, immigrants are more willing to take the jobs that existing US workers do not want to do (eg- service industry).

I can’t help but roll my eyes at the notion that the Fed thinks it’s bad when labor is finally getting its long overdue pay increases and that it must use its power to fight that. But when corporate profits are through the roof, that’s fine? You want to know where the bias towards making the rich richer lies, look no further.

I suffer from the same affliction… even though my own income is now, in retirement, more tied to corporate profits than to improvements for labor.