Rates aren’t high enough yet.

If you like tautologies, that’s the best way to explain why the Fed may feel compelled to hike rates significantly higher than market participants currently expect in 2023.

So far, there’s scant evidence to suggest the Fed has crossed any red lines in the context of the real economy. Sure, markets suffered mightily in 2022, and as I never tire of reminding folks, there is a point beyond which what happens on Wall Street spills over and floods Main Street. But we haven’t reached that point yet:

- For one thing, dangerous spillover to Main Street typically requires stress in funding markets — problems with the proverbial plumbing.

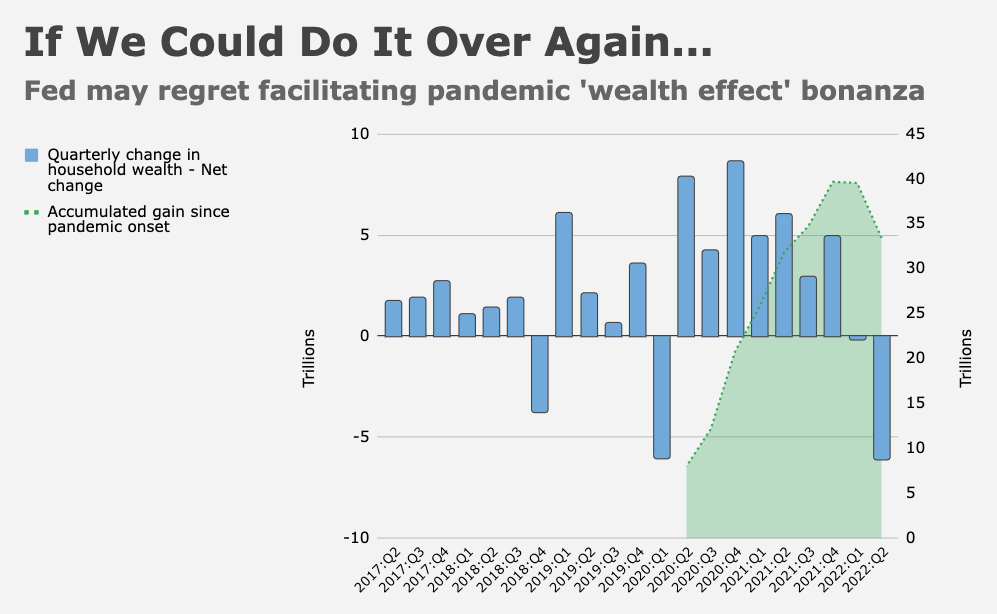

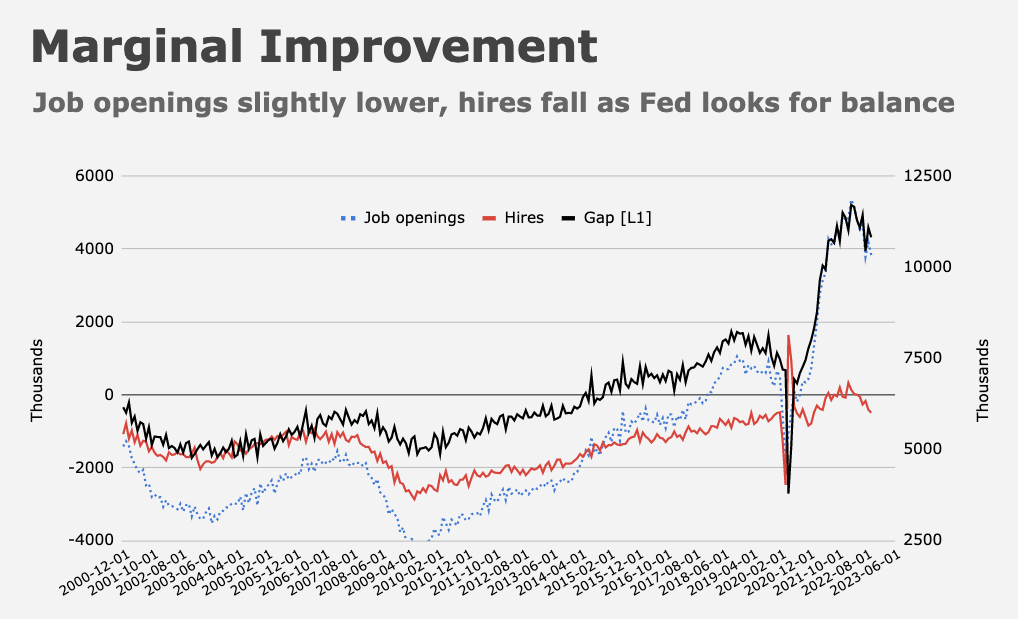

- From a macro perspective, the accumulated wealth effect from the pandemic bonanza in stock and property prices is nowhere near reversed despite recent steep declines in household wealth, demand for labor still far outstrips supply, only the least well-off income cohorts have less liquid savings than they did pre-pandemic and spending remains resilient in the US.

To be sure, the Fed did some damage in 2022. Just ask the yen, the euro, the yuan, Treasurys, IG credit, Cathie Wood, and so on. But if the goal is to slow the real economy in the service of smothering inflation, you could argue the Fed has made almost no progress at all.

There are two caveats. First, the surge in mortgage rates succeeded in slamming the brakes on the US housing market. Pending home sales fell almost 40% in October. But even there, the situation is more deep freeze than deep downturn. Second, monetary policy acts on a lag, so it’s possible the Fed has embedded a latent recession through the tightening already delivered.

But consider that when it comes to debt and credit servicing, affordability hasn’t deteriorated much yet. The figure on the left (below) from JPMorgan shows coupon payments on the Bloomberg Global Agg and high yield indexes as a share of global GDP. The annotations speak for themselves, but the bank spelled it out: “The lower diamond shows a projection for how coupon rates are set to increase in the next three years as bonds mature and are assumed to be refinanced at current yields and the higher diamond shows a proxy for where interest costs as a share of GDP would rise over the next decade or so” assuming refinancing on the same terms.

The read-through is straightforward: Rates would need to stay high for a very long time in order for affordability to deteriorate dangerously.

The figure on the right (above) is JPMorgan’s attempt to proxy the broad cost of credit. They use BIS estimates of total credit to the non-financial sector, and assume that “two-thirds of credit to households is fixed rate with the remaining third floating rate, that credit to non-financial corporates is split roughly equally between fixed and floating rate, and that government debt is predominantly fixed rate.”

The bottom line: Yields have surged to levels not seen in almost a decade and half, but as a share of global GDP, interest costs are merely back to 2014 levels. It’d take a decade to get back to levels seen prior to the financial crisis.

At the same time, the pace of loan creation across the US, UK, Europe and Japan is double that seen from 2015 through 2019, US household cash balances are still very elevated, as are corporate margins.

All of those factors, JPMorgan’s Nikolaos Panigirtzoglou said, “have thus far allowed economic agents such as households and corporates to take on more debt and sustain their spending even in the face of Fed funds rates being raised to 4% and likely further to 5% by March.”

That’s suboptimal for Jerome Powell under the circumstances. “There is a risk that unless credit creation begins to slow, this ongoing demand could eventually force the Fed to push interest rates to above 6%,” Panigirtzoglou cautioned.

Coming full circle: Rates aren’t high enough yet.

{kind=link}

{kind=link}

The beatings will continue until morale improves.

Thanks for those two charts.