Predictably, my coverage of Sam Bankman-Fried’s self-described “f–k up” elicited several irritated e-mails from incorrigible crypto proponents, who, much like Bankman-Fried himself, are having a difficult time coming to terms with the scope of what’s just happened.

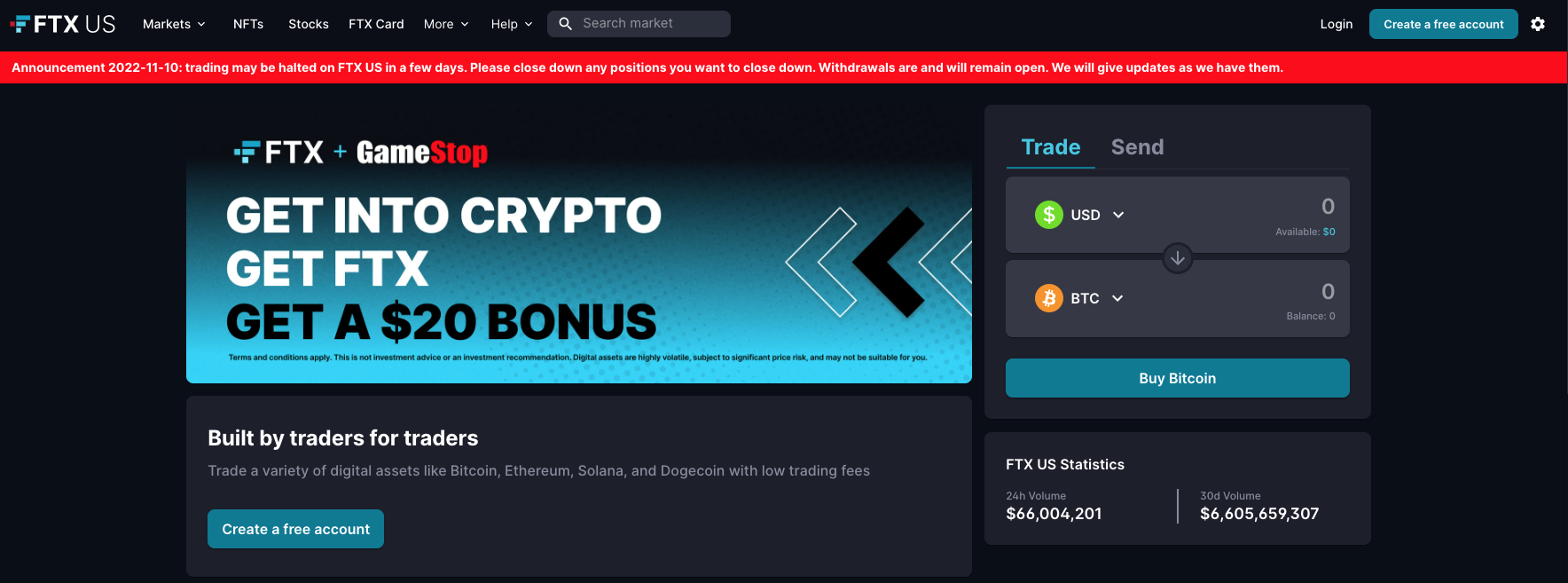

According to Bankman-Fried, FTX’s US business was “100% liquid” as of Thursday morning. Just hours later, a red banner appeared atop the platform’s website. “Announcement 2022-11-10: Trading may be halted on FTX US in a few days,” it read. “Please close down any positions you want to close down. Withdrawals are and will remain open. We will give updates as we have them.”

Directly below that message sat an oversized ad touting a partnership with GameStop. “Get into crypto,” it exhorted visitors. “Get FTX. Get a $20 bonus.”

Bankman-Fried might consider availing himself of that generous offer. Given what’s alleged about how self-referential his “empire” was, it’d be entirely consistent with his modus operandi if he plugged FTX International’s $8 billion hole by tapping FTX US for 500,000,000 promotional “bonuses.” I’m just joking. Sort of.

CoinDesk later reported that “FTX US temporarily ceased processing withdrawals around midday Friday before inexplicably restarting hours later.”

The potential trading halt at FTX US prompted Bloomberg to assume the business, like Bankman-Fried’s other businesses, is probably worthless. His stake in Robinhood was likewise removed from Bloomberg’s net worth calculation given that it was apparently held in Alameda, and might’ve been pledged as collateral.

“This May and June, Alameda suffered a series of losses from deals, includ[ing] a $500-million loan agreement with failed crypto lender Voyager Digital [which] filed for bankruptcy protection the following month,” Reuters reported, in a behind-the-scenes look at FTX’s unraveling. “Seeking to prop up Alameda, which held almost $15 billion in assets, Bankman-Fried transferred at least $4 billion in FTX funds, secured by assets including FTT and shares in Robinhood,” the same linked article said, citing sources.

With the US operation valued at $1 and the Robinhood stake tied up in the defunct Alameda, Bankman-Fried’s fortune was written down by Bloomberg to zero (figure below).

He is, for all intents and purposes, broke. Certainly not in the sense that a homeless person is broke, but as far as (former) billionaires go, Bankman-Fried has “no” money. He lost $16 billion (substantially all of it) in less than a week.

Worse, he’s under investigation by the SEC, according to Bloomberg, which cited someone familiar with the situation. That’s on top of investigations (plural) into FTX, FTX US and Alameda. The Justice Department is interested, apparently.

I’ve endeavored to be as polite as possible about this over the last several days, but that’s no longer a tenable predisposition. Bankman-Fried was, as of Thursday anyway, engaged in an effort to secure a $9.4 billion rescue package from an investor group which, according to Reuters, included Tron founder Justin Sun as well as Dan Loeb. Loeb is a serious person, so I certainly imagine he takes the risks associated with this situation seriously. But a lot of other serious people fell for the Bankman-Fried narrative, a decision they surely regret on some level, even if they won’t say so publicly. Efforts to cobble together a rescue met with little success, Reuters went on to say.

Assuming reports around US regulatory investigations are accurate, it’d be, in my opinion, exceptionally ill-advised to participate in any deal that hands him, or FTX, a significant sum of money in or out of bankruptcy. That, to me, sounds like a gross dereliction of fiduciary responsibility, assuming there are still parties interested after Friday and assuming any such parties have such a responsibility.

The Bahamas froze FTX’s assets and appointed a liquidator on Thursday. “The Commission is aware of public statements suggesting that clients’ assets were mishandled, mismanaged and/or transferred to Alameda Research,” the regulator said. “Based on the Commission’s information, any such actions would have been contrary to normal governance, without client consent and potentially unlawful.”

I’m done mincing words when it comes to crypto, and also with being polite about this situation in particular. On some days, I run fresh out of patience with a world that systematically, as a matter of course, treats possible white collar malfeasance allegedly committed by the already rich and privileged differently than blue collar crime allegedly committed by people who weren’t rich until they broke the law and were never privileged.

Like everybody else, Bankman-Fried is innocent (of everything) until proven otherwise. That goes without saying. So, spare me any protestations that I’m assuming he’s guilty of anything. I’m not. But a lot of other people seem to be. Similarly, I’m not the one investigating him. The media is, figuratively, and US regulators are, literally. Also, I didn’t freeze his assets. The Bahamas did.

All I’m suggesting is that if, instead of possibly mishandling enormous sums at a crypto exchange and trading house, Bankman-Fried allegedly ran a drug exchange and trading house, and if, instead of being Sam Bankman-Fried, born on Stanford’s campus (literally) to a pair of highly accomplished law school professors, he were a hypothetical Terrell “Big Dolla” Williams, born in a Chicago housing project to a poor single mother, or Williams’s hypothetical boss, Diego “El Jefe” González, born to nobody knows who in Sinaloa, and currently living in the Chicago suburbs in a $4 million home purchased by his wife, would he still have an active Twitter account? (Maybe, under Elon Musk, but that’s a separate discussion.) Would his organizations still be functioning at all? Would he be in discussions with an investor group to inject $9 billion into his crumbling empire? Would Bloomberg and Reuters still be reaching out for quotes? If not, why not? After all, the scenario I’ve just posited assumes that no guilt has been established for Bankman-Fried, Big Dolla or El Jefe. They’re all innocent until proven otherwise. Or at least that’s the way the legal system is supposed to work.

You might (easily) argue the comparison doesn’t hold up. The crypto trade isn’t illegal, after all, and the (hard) drug trade is. But in this case, I’d argue that’s an exercise in question begging. It’s not obvious that the crypto trade is entirely legal in all its various manifestations. Indeed, US regulators, including the SEC, are engaged in a sweeping effort to determine what’s legal and what isn’t in the space, and it’s entirely fair to say that Bankman-Fried was, directly or indirectly, engaged in every meaningful aspect of the crypto market. So, if anything is illegal in the space, he might’ve done something illegal at some point. That’s not an accusation, it’s just working backwards using simple logic.

How do we distinguish between someone who ruins lives by way of alleged financial chicanery and someone who allegedly ruins lives via the sale of illicit, addictive substances? Is a life ruined by purported white collar fraud somehow a more tolerable life than one ruined by drug addiction? Maybe, or maybe not. You can come back from financial ruin, but you can also come back from drug addiction. Or, you can not come back from either.

While the Big Dollas and El Jefes of the world may de jure enjoy the same assumption of innocence accorded to the Bankman-Frieds of the world, they certainly don’t de facto enjoy the same assumption.

Finally, let me pose an even more uncomfortable question to readers: Who’s smarter, more capable and deserving of our collective adoration: The Stanford-born, all-lanes-open whiz kid who made $16 billion by way of legal goods and services which some believe should be illegal, or the child born to nothing, with nothing and with no lanes open, who made $16 million trading illicit goods and services which many people believe should be legal?

On Friday, FTX.com, FTX US and Alameda Research filed for Chapter 11 bankruptcy in Delaware. Bankman-Fried stepped down as CEO. “I’m really sorry, again, that we ended up here,” he said.

One way or another, my guess is he gets some manner of bail out, if not literally, in a financial sense, then figuratively, in some other sense. In my opinion, he won’t deserve it.

{kind=link}

Great post. Law and order is the new slavery in sheep’s clothes.

IMHO, crypto should be illegal and drugs should be legal 🙂

There is a reality TV concept in here somewhere

Chappelle already did it.

One might argue that Big Dollas will actually spend more of his booty into the general economy.. vs the average ‘gifted high net worth on paper’ holder.

Big Dolla is a pillar of his community. On weekends.

H-Man, my youngest (age 35) told me this was a crypto buying opportunity. I just shook my head, wished him the best, and told him we he could talk about it when he can explain how it works and how it is priced.

I’d rather buy Bitcoin at $50,000 had this not happened than buy it at $15,000 knowing it did happen. This was very bad for the space.

Really good post here. Hit on a lot of strong notes.

Walt – The comparison of SBF the crypto dealer to Chicago drug dealers reminded me of W. Adler’s book “Land of Opportunity” about the Chamber’s brothers Detroit crack operation in the 1980s. They took the opportunity they had and built a business empire. Unfortunately, selling actual crack cocaine is illegal and landed the Chambers brothers in jail.

I guess Milken spent some time in jail too ???

I see renewed calls for crypto to be regulated and made safer. My question is, why encourage broader participation in crypto by ostensibly making it safer?

Depending on who got burnt Sam might actually be going to jail. I suspect he managed to trap a few well connected clients.

I did find it curious that he bailed out Voyager; any diligence in that deal would have uncovered its impending bankruptcy. After seeing this implosion, I suspect Sam bailed so many firms out because he had no option, given how intertwined all these businesses were.

Alameda started off as an arbitrageur, and at some point became the casino where FTX Customers’ funds were gambled. Maybe Alameda’s funds were lost by some of the bailed-out firms and it isn’t until now that the situation became unmanageable and impossible to hide.

My hope is that this grants the excuse politicians were looking for to regulate crypto to the point coins become just like gift cards redeemable in video games.

Excellent read as usual and your uncomfortable question to readers is one we should consider as a society more often. Even as a crypto proponent and believer, which I still am, watching this drama unfold has been surprising. I’ll be the first to admit there are a lot os smoke and mirrors as well as rampant speculation in cryptosphere, but there are also opportunities and promises for innovation that might bring societal good, we’ll see. This will certainly set back adoption and may cause over reaction from regulators, but my loses from the debacle have been deminimis so far from funds I forgot I had at BlockFi (now seemingly defunct also), I realize that had I lost real money I might feel differently. Avarice, greed and human incompetence will cause growing pains like this in any new industry, the history of banking and finance is littered with equivalent episodes, not even great human minds like Issac Newton could escape the FTX of his time, anybody can read how at the time citizens clamored for outlawing stock trading after the South Sea fiasco. Humans tend to learn the hard way, I feel for those who will not recover or lost meaningful funds on this debacle, some are close friends. I still believe there are ways to be in crypto and be safe, I’ve done it and so have others, hopefully this leads to progress and to some folks landing in prison, something we did not see when it was bankers negligence and greed collapsing the financial system in 2008.

Yeah, I mean, with apologies to anyone who might’ve been offended by my comparison here, the fact is, “Here are some dangerous drugs that you, me and everyone in the world knows are dangerous” is not the same sales pitch as “Here are cryptocurrencies, if you’re unfamiliar, they’re great and wonderful, and many people believe they represent a quantum leap in economic liberty.”

Addiction is addiction, and it’s bad. But it’s impossible to argue that anyone over the age of 18 doesn’t understand that picking up hard drugs poses considerable risks. Sure, people do it anyway, but people also drive 75 mph down curvy roads knowing full well that it’s dangerous. In both cases, they’ve weighed the danger versus the fun and decided the latter outweighs the former.

By contrast, it’s entirely possible to argue that many (most, even) people who get into cryptocurrencies have no idea that it poses considerable risks, of if they do, they don’t have any conception whatsoever about the nature and character of those risks. It goes well beyond the risk associated with traditional assets. It’s much more dangerous than betting on meme stocks, for example.

So, people can’t do the “math,” so to speak. “I like to drive fast. I know driving fast is dangerous. But, rightly or wrongly, I judge the odds of me dying on this curvy road at 75 mph to be low enough that the experience is worth taking the risk.” People can’t do that “math” with crypto. Because they don’t have enough information.

H and others, a question.

What sort of regulations, auditing, enforcement, and expense, either US or global, would be required to make crypto “safe” enough?

Aside from the challenges of regulation and enforcement of something that exists online, with only a small and easily moved physical presence, how do you audit an asset that has no intrinsic value at all?

I fear that regulators will just get sucked into a hopeless financial version of the War On Drugs, chasing slippery URLs and shape-shifting balance sheets around the world while being undercut in Congress by crypto lobbying and influence-buying.

I worry that the imprimatur of government regulation and approval will encourage participation by more can’t-do-math ordinary people. Losses will grow, from twenty-somethings losing thousands to families losing everything, risks will become systemic, and government bailouts unavoidable.

I question why we (society, govt, US, etc) should devote all this effort and start down this slippery slope, to make better and “safer” a thing with no societal value.

A couple of points here. As a professional techie, I’ve always felt the comparison to the war on drugs is apt. Trying to regulate crypto is a silly battle against a shapeshifting specter, probably being designed by people who have a better grip on justifying their budgets and mollifying their constituents than on anything about the crypto space. Technologically, I don’t see how regulation can be accomplished on a practical level. I mean, yeah, last week they finally caught that guy who bilked the Silk Road for bitcoin in 2012… after 10 years and how many man-hours of work just to catch a single guy?

Where I disagree with you is on the “no societal value”. The potential value of decentralized computing, if they overcome the current technological hurdles, is huge, and there needs to be an incentive mechanism to get people to contribute CPU cycles to running the network. That’s where crypto’s actual use case will eventually arise.

At that time, regulation will make more sense, too, because then you’ll have an Uber or an Ebay running serverlessly, code executing on the monetary network itself, but it will intersect with the real world in terms of delivering services or products and that’s a handle governments can use to regulate it. “You swindle grandma on your crypto token, we don’t let you run your cars on our streets.” But right now, without a “handle” to apply real-world leverage, attempts at regulation are tilting at windmills.

I wonder if “decentralized” can really be applied to cryptocurrency? Coins like Luna, Terra, FTT, Tether, etc seem very centralized, their viability depends on a single issuing/backing entity. Even coins like BTC, Ether seem highly exposed to a few large exchanges.

I’m of a time and a place. In the fall of 1982, I took a new job. As a result, I began to read Grant’s Interest Rate Review, the Bank Credit Analyst, the Economist and the FT. So I ask Moral Hazard? Who pays for Heads I win, tails you lose with a fallback position of heads I win, tails I break even? Add to this the lie that can’t learn from other countries’ experience, and the prevalence of Everybody’s always liked my work amongst the elites….I say let this asset class go to zero-I’d rather have the learning experience create that type of risk aversion as opposed to an unhealthy fear of stocks, bonds etc….The tide rolled out and there are many naked swimmers…

“I’m done mincing words when it comes to crypto, and also with being polite about this situation in particular. On some days, I run fresh out of patience with a world that systematically, as a matter of course, treats possible white collar malfeasance allegedly committed by the already rich and privileged differently than blue collar crime allegedly committed by people who weren’t rich until they broke the law and were never privileged.”

100% with you on that one.