Headed into the November FOMC meeting, many worried Jerome Powell would come across as unduly conciliatory while editorializing around a policy statement that was widely expected to telegraph the Committee’s intentions to decrease the pace of rate hikes following a fourth consecutive three-quarter point move.

As it turns out, Fed watchers needn’t have been concerned. Powell managed a hawkish spin on what might’ve otherwise been traded as dovish statement language. The Committee did, in fact, suggest rate hikes will be smaller going forward, but Powell succeeded in convincing the market to focus on a higher expected terminal rate, which policymakers plan to hold for longer.

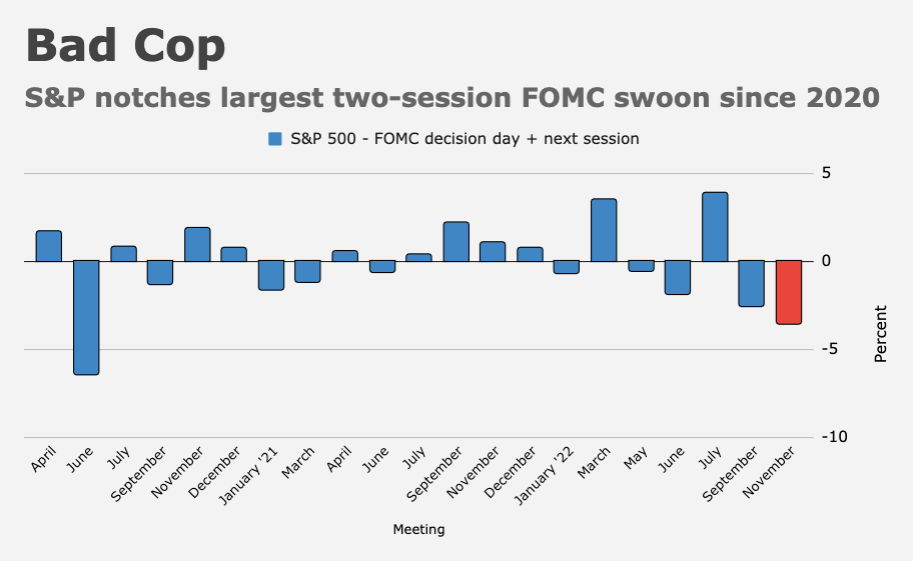

That was no small feat for Powell who, whatever else he is, isn’t the best communicator. US equities logged their largest two-session FOMC decline in two years, helpful for a Fed that desperately needs to tighten financial conditions. Higher stock prices, lower yields and dollar weakness all work to ease financial conditions at cross purposes with the Committee’s inflation-fighting efforts.

Seen through that lens, Thursday’s outlandish rally on Wall Street, as well as the attendant drop in US yields and accompanying dollar weakness, were a veritable disaster. That’s not hyperbole. Well, it is hyperbole, but not in the narrow context of markets as a transmission mechanism for monetary policy.

If you haven’t seen some version of the figure (below) by now, then financial media outlets, mainstream and otherwise, aren’t doing their jobs.

The easing impulse as measured by Goldman’s US financial conditions index was among the largest on record, eclipsed only by that seen in and around crises (which beget volatility and, of course, massive stimulus).

Thursday’s easing on Goldman’s gauge was on par with that seen the day after the CARES Act passed, and just shy of the easing impulse unleashed by the Fed’s announcement of open-ended QE, corporate bond buying and credit ETF purchases two days previous.

To call that counterproductive would be to materially understate the case. The Fed will want to walk it back. In addition to being entirely contrary to the Committee’s efforts to curb inflation, it’s also indicative of broken, illiquid markets.

Although it was tempting to celebrate what, for anyone with even a few hundred thousand dollars invested long, was a very lucrative six hours, in reality, Thursday should probably live in some kind of infamy.

Oh, and if you’re wondering whether the Fed noticed, Nick Timiraos tweeted about the monumental drop in Goldman’s index. “[The] intra-day estimate of US financial conditions from [the bank’s] index eased by over 50bps [Thursday] following the rally triggered by the October CPI print,” he said, noting that the drop constituted the “third-largest single-day decline on record.”

{kind=link}

So is it that there’s so much money sitting on the sidelines that institutional and retail investors are looking for any reason to jump back in? Such an odd dynamic; good is bad and bad is good. Reminds me of “Bizarro World” from the comic books of my childhood.

Well, there were 3 fed speakers on the CPI day that could have walked back the market jump, but either they don’t want to or they failed in their attempt. From what I read, their statement likely gave more fuel to the rocket ship.

On second thought, their statements are consistent with the FOMC official statement. Now I wonder whether the dovish FOMC statement were in fact from the voting members, and Powell is the lone hawk in the FOMC meeting. He then gave a hawkish press release just to show everyone who’s the boss. Powell did the same thing at Jackson hole and tighten financial conditions with hawkish (or Volckish?) speech.

Not a disaster. Both recent events and most economic releases lately argue for lower rates and the market obliged. Pretty soon inflation fighting will likely look like fighting the last war. But we will have plenty more data between now and January to see if this is correct. The stock market may get blindsided by a rapid fall in corporate profits….

From a practical perspective, what action is the Fed going to take that will meaningfully influence this trajectory? Most of the more aggressive actions they could take (surprise rate hikes, for example) won’t happen. The market seems to assume that the fed will wilt on rates at the first whispers of any sort of financial distress in the market. Seems like a self-reinforcing cycle: raise rates – market sees some change in the rate of change of rates – market financial conditions loosen – fed tries to react.

Could you expand on this, please? Was volume lower than you think it should have been? Or was this just more general commentary? Do you know who was driving the rally?

Also, is it actually bad for the Fed, or just the appearance of bad? I mean i (think i) understand how higher equities translate to a broadly easier time raising cash and thus increased demand, but isn’t that easing impulse mostly confined to businesses? Any increased demand on the part of guys like me would be at the end of a long lag.

Also, i wonder if much of yesterdays rally was exacerbated by the harried flight out of crypto.

H-Man, so what does the market do with a soft print on CPI in December?