For weeks, 4,200 on the S&P was bandied about by some top-down strategists as a “sell-the-rip” level — a kind of bridge too far for a star-crossed bear market rally condemned to collapse under the weight of negative earnings revisions.

The benchmark of all benchmarks is testing that level and there’s a case to be made that US equities could breach the threshold — and then keep going.

“We are in the midst of an angst-ridden pain trade higher in stocks which is pushing us back into increasingly unstable FOMO-type behavior,” Nomura’s Charlie McElligott said Thursday.

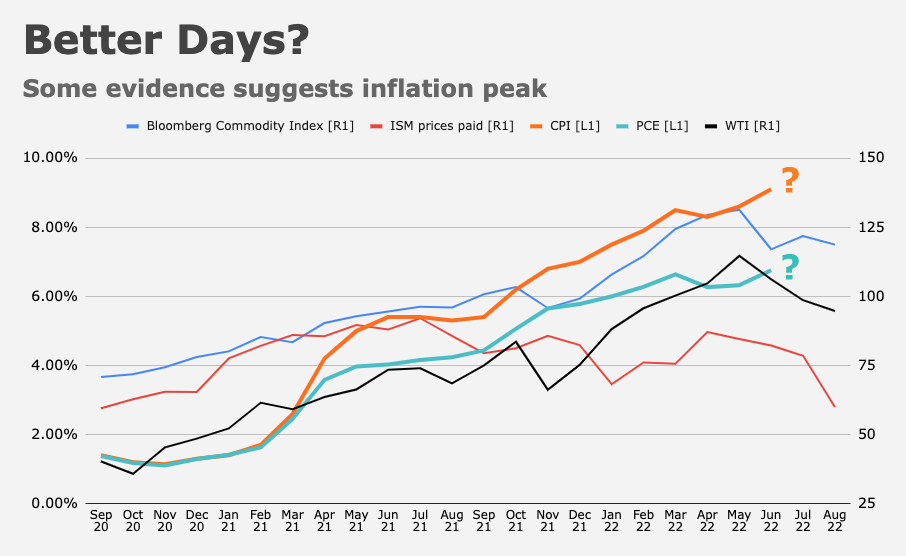

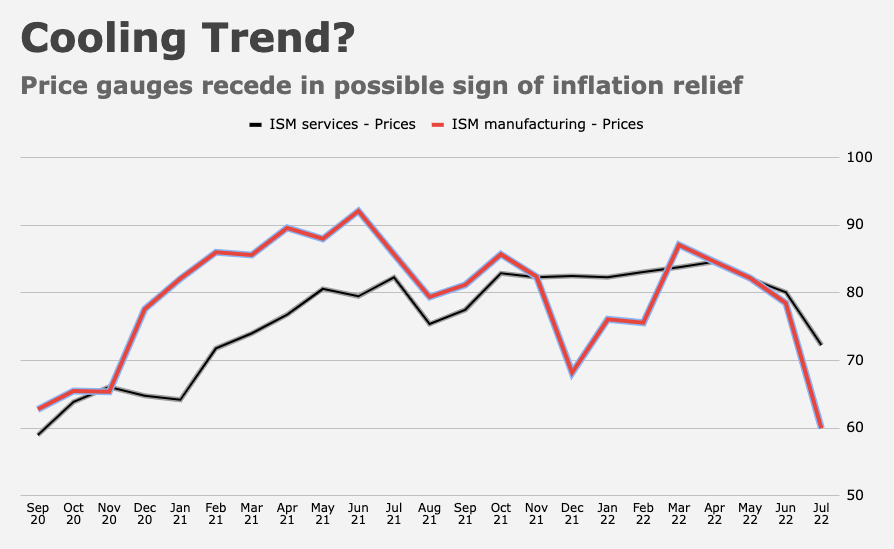

In addition to signs of peak inflation (e.g., receding commodity prices and declines on key PMI price indexes) and the (highly contentious) notion that earnings season was “better” than expected, there are two key factors.

First, CTA covering and options dynamics are contributing quite a bit from a flows perspective, and the latent vol control bid is poised to “realize” over the next few weeks. Second, light positioning made July’s rally very painful for a lot of folks, and that’s fuel on the fire to the extent it suggests underperformance is prompting a panic grab for exposure.

Both the L/S crowd and macro funds just “don’t have it,” so to speak. The former’s beta to the S&P sits in just the 9%ile going back almost two decades, for example. And the latter’s correlation to equities is likewise indicative of a “missing the boat” conjuncture (figure below).

The bottom line, McElligott said, is that “people are hurting for performance, and the equities tape has gotten away from them.”

It’s thus not surprising (even as the sheer scope is conducive to raised eyebrows) to observe what looks like an increasingly desperate grab for upside.

McElligott again flagged “enormous ‘positive $Delta’ flows in Index / ETF Options” (figure below), alongside some “lumpy Put selling,” particularly in mega-cap tech. Legacy right-tail (i.e., upside) hedges are, naturally, enjoying the move.

“Stunningly, we now see SPX / SPY $Delta back up to 90.6%ile since 2013, and even more wildly, we see QQQ $Delta rank back to 99.5%ile,” Charlie exclaimed.

So, how could it get “worse,” where that means more frantic, from here? Well, as McElligott went on to note, 4,200 SPX could be “interesting,” as that’s the short strike for some recent call spread buyers. “Hence, we could see a ‘Short Gamma’-type move on an upside break through that level,” he wrote.

Beyond that, there’s the latent vol control bid, which Nomura’s estimates project could be around $22 billion as three-month trailing realized mathematically catches down, and assuming a relatively tame (i.e., +/- 1%) daily outcome distribution for spot. If the market managed to defy seasonals and trade in what, for 2022 anyway, would count as a very narrow daily range, the re-allocation impulse from vol control could be considerably larger.

Meanwhile, McElligott reminded market participants that so far, the lion’s share of the CTA “buying” in equities was actually covering. Even after $60 billion of notional exposure adds, the net position across global equities is flat (figure below).

With equity-only net exposure sitting in just the 18%ile, there’s considerable room to get long. For example, SPX 4,307 would trigger a “100% Long” signal on Nomura’s model.

Of course, not much of this is “real,” as it were. It’s just flows chasing flows. But it’s all too real for a fundamental/discretionary crowd which wasn’t positioned for it. Underperformance is underperformance. They have to chase it.

“This continues to be ‘un-economical’ and/or ‘mechanical’ behavior, which is creating a potential ‘false optic’ for increasingly desperate investors who don’t have performance or positioning,” McElligott wrote.

It’s chasing ghosts in an illiquid summer tape. As Charlie put it Thursday, it’s “the market that wasn’t there.”

{kind=link}

{kind=link}

Perhaps a naive question, but is there a strong and direct correlation between: (i) the big $’s being swung around by the “un-economical” CTA and Vol Control players, and (ii) the new $’s that were created via QE (…which, by and large, are still out there “circulating around”, even as new creation has ceased) ?

I personally don’t see a correlation, QE is basically an asset swap resulting in the creation of bank reserves with the Fed, so not sure how that would connect to CTA/systematic funding, there is a massive pile of institutional money floating around independent of QE even if QE might inflate financial asset pricing.