A week ago, I (somewhat begrudgingly) expressed guarded optimism about earnings season in the US.

At the time, just 21% of companies had reported. “A lot hangs on mega-cap tech,” I wrote, in “Just Don’t Call It Optimism.”

In the end, mega-cap tech was fine with the exception of Facebook, which logged its first revenue decline on record. Apple and Amazon beat, and investors found plenty to like in Microsoft’s guidance and Google’s ad numbers.

With 56% of companies having now reported results, more than half beat consensus by at least a standard deviation (figure below). That’s considerably better than the long-term average, albeit nowhere near post-pandemic levels.

35% of reports were in line, not materially different from Q1 or Q4 2021. 21% missed, roughly the same as the prior two quarters and although the percentage missing by at least a standard deviation of estimates is considerably higher (12% versus 9% last quarter) it’s hardly indicative of disaster.

Last weekend, I wrote that although it was still early, there was no evidence to suggest Q2 reporting season would go down as singularly catastrophic. Now, with more than 70% of S&P 500 market cap on the books, the catastrophe is next quarter’s story — if it’s a story at all.

Retail earnings (set to roll in over the next four weeks) will doubtlessly be lackluster, but at this point, it’s probably fair to suggest that’s mostly “priced” in, where the scare quotes denote that the market is cognizant of retailer woes. It’s at least priced into investor psychology.

The bottom line (figuratively and literally) is that it just wasn’t there, where “it” means the tidal wave of guide downs and margin mishaps that some bearish strategists anticipated. Next week will invariably bring more revisions breadth charts using various leads and lags to show how close we are to something bad. At the risk of lapsing into colloquialisms, I’d just reiterate that it’s either there or it ain’t. Right now, it ain’t there.

Since the start of earnings season, consensus estimates for 2023 S&P profits have been cut by 2%, with the biggest downward revisions (by far) seen in Comms Services (figure below).

Obviously, energy is the outlier. Exxon and Chevron reported record quarterly profits on Friday.

“The ‘negative earnings revision’ and equities broad bear case took a soul punch this past week [as] perversely, margins have largely held-in and even expanded due to (inflation) pricing power overwhelming slowing (macro) volumes,” Nomura’s Charlie McElligott said, calling earnings “generally ‘okay enough’ into really low expectations” and noting that the market found “massive relief in the high-profile index heavyweight Amazon and Apple prints and guides.”

All of this suggests it was simply too early for the profit recession story. I’d also note that the FX headwind could abate going forward if expectations for a less aggressive (albeit still assertive) Fed are borne out.

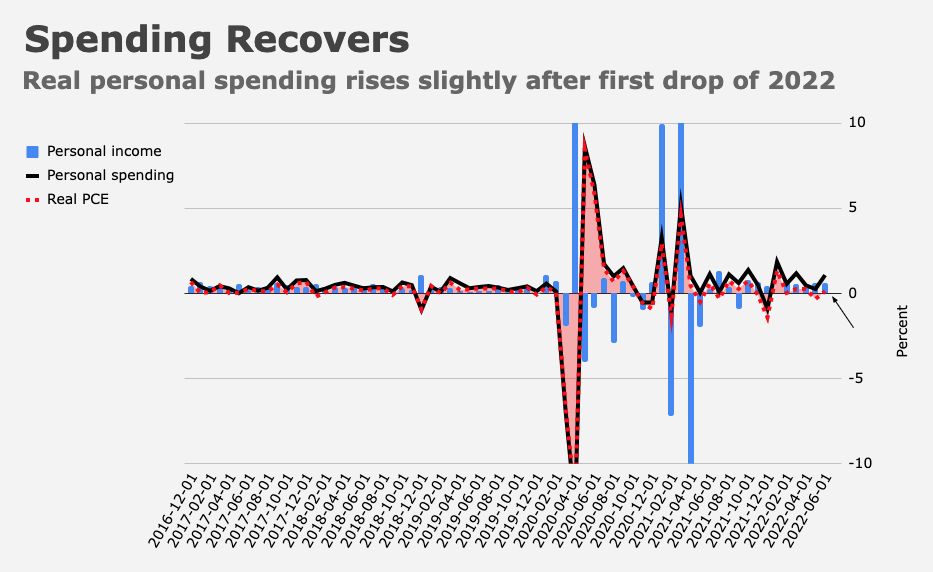

Of course, there’s talk of a recession. That should impact the consumer, who, according to Q2’s advance read on US GDP, is faltering, notwithstanding June’s barely positive real personal spending print.

But even there, commentary from Visa and Mastercard suggested consumers aren’t really retrenching. Both companies benefited handsomely from cross-border travel during the second quarter, but it was the unequivocal nature of the management color that struck me.

“We’re seeing no evidence of a pullback in consumer spending,” Visa CFO Vasant Prabhu said. Mastercard chief Michael Miebach flagged “some shift” to gas and groceries from discretionary categories like home furnishings, but said US spending “remains healthy.”

“I was told there’d be drama.”

{kind=link}

U.S. consumer to pundits: “Rumors of my death have been greatly exaggerated.”

Not sure, but never discount the wisdom of that great ’60s Western: “Have credit card, will travel.”

It’s a mixed bag for sure now

And now there is Manchin coming to the rescue with a big spending bill as well asthe infrastructure bill kicking in sometime and the chips bill. Get some lower inflation #’s and the pundits will need a new narrative.

It is kind of like everyone expected the demolition derby, with every car made showing up and only a couple Plymouths did.

On a relative basis, America and Americans are navigating all of the current global economic issues (too long to list) better than anywhere else.

The investment money seems to be following.

I just got some doors on Monday that I ordered back in March. Still don’t have the screens I ordered February. The hospital where I work is still 8 cars short in their homecare motor pool.

It’s going to take some time yet to work through the backlog. Is it realistic to see earnings fall in any significant way for another Q or 2 ?